The reacquisition isn’t a supply chain fix — it’s the most expensive financial-engineering reversal in modern aerospace, and the integration is already over budget.

The 60-second version

In June 2005, Boeing sold its Wichita and Tulsa fabrication operations, including the entire fuselage of every 737, to private equity firm Onex for $900M cash. On December 8, 2025, Boeing closed on buying it back for $4.7B in stock, $8.3B including assumed debt. Between those two transactions, Onex turned a $375M equity investment into $3.2B, Spirit AeroSystems lost roughly $3B in 2023-2024 alone, two 737 MAXes crashed, and a door plug detached from an Alaska Airlines flight at altitude. The reacquisition isn’t Boeing fixing its supply chain. It’s a forced unwinding of a financialization bet from a different management era, and the company’s own filings show the unwind itself is being managed by the same incentive structure that produced the original mistake. CFO Jay Malave admitted on March 17, 2026 that “you don’t get access to all the information until you actually close,” which is to say, shareholders learned about the integration cost overrun a quarter after they paid for it.

Skip to the section that interests you most

The 2005 deal Boeing now wishes it could undo

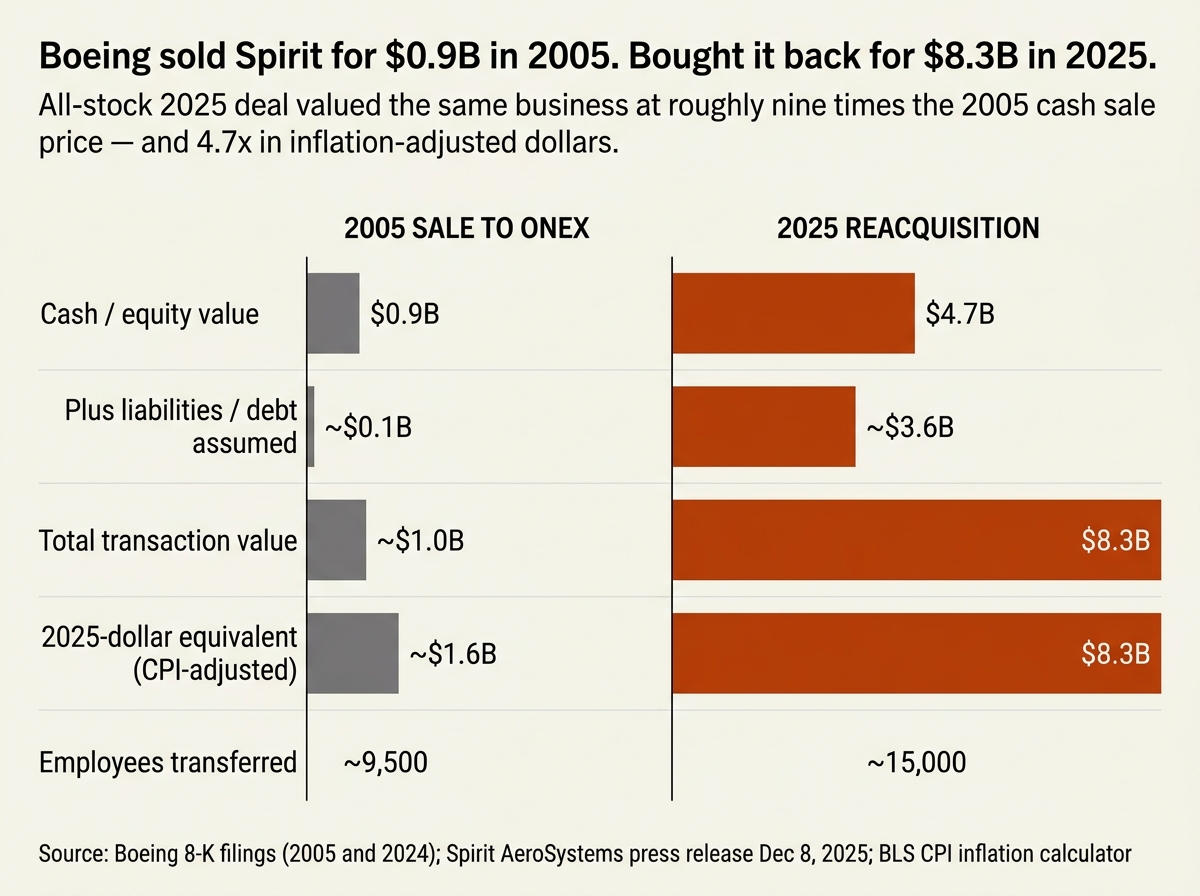

In June 2005, Boeing sold its Commercial Airplanes operations in Wichita, Kansas, plus facilities in Tulsa and McAlester, Oklahoma, to Canadian private equity firm Onex Corporation. The deal terms, per Boeing’s own 8-K filing: approximately $900M in cash, plus the transfer of about $100M in liabilities. The combined operations had generated roughly $2.2B in annual costs in 2004 and produced fuselage and structural components for the 737, 747, 767, and 777 programs.

Boeing’s then-CEO Harry Stonecipher was running an aggressive asset-disposal program designed to make the company “asset-light.” The conventional Wall Street wisdom of that era held that capital-intensive, unionized, low-margin manufacturing was a drag on multiple expansion. Sell the metalwork, keep the engineering and final assembly, watch the stock re-rate. GE was running a version of this playbook. Sears was running a version of this playbook. Most US industrial conglomerates between 1995 and 2010 were running variants.

Boeing’s 2005 SEC filings reveal what the deal cost the company in one-time charges. Across Q2, Q3, and Q4 of 2005, Boeing recognized roughly $538M in pre-tax non-cash charges tied to the sale. The largest single charge, $238M booked in Q3, was specifically attributed to “the curtailment and settlement of pension plans and the transfer of pension liabilities.” Another $190M followed in Q4 for post-retirement obligations. About 9,500 Boeing employees moved from the Boeing payroll to the new entity, initially named Mid-Western Aircraft Systems, later renamed Spirit AeroSystems, and the long-tail pension and healthcare obligations attached to them moved with them.

In exchange, Boeing received cash, a long-term supply agreement that locked in cost savings on the structures and parts the new company would supply, and continued partnership on the 787 Dreamliner program. On paper, it looked like a brilliantly executed financial engineering trade.

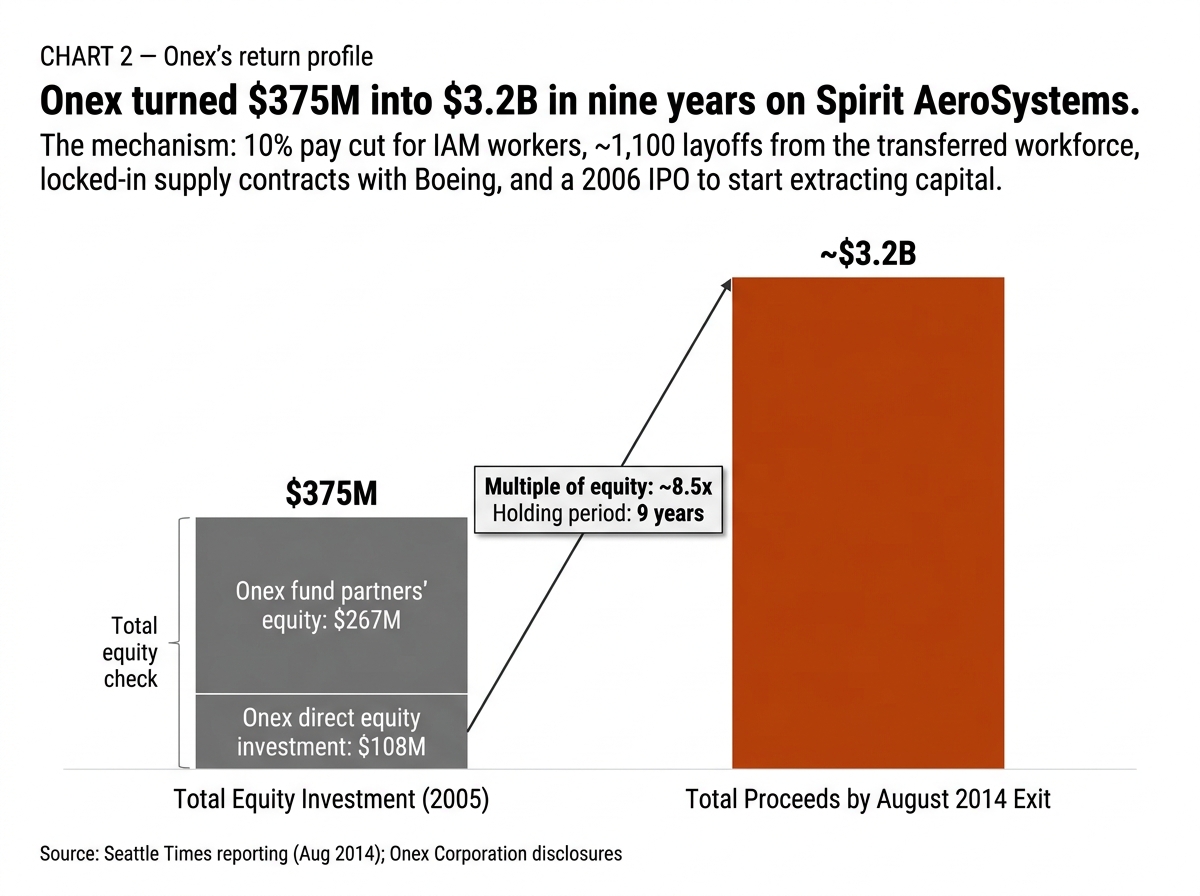

What Onex actually extracted between 2005 and 2014

The PE math on Spirit was the kind of return that gets PowerPoint slides built around it for fundraising decks.

Onex’s total equity check was $375M, $108M from Onex itself, $267M from its limited partners. The rest of the purchase price was financed with debt loaded onto the new entity. By the time Onex sold its final shares in August 2014, total proceeds had reached approximately $3.2B. That works out to 8.5x return on the equity investment over nine years.

The mechanism for that return is worth understanding because it explains a lot of what came after. Within months of the spinoff, the new owners renegotiated the IAM union contract: the workers who had transferred from Boeing took a roughly 10% pay cut, and about 1,100 of the 9,500 transferred employees were cut entirely. The new company also took Spirit public on the NYSE in 2006, allowing Onex to begin extracting capital years before its eventual full exit.

But the real margin came from operational discipline against the long-term supply agreements with Boeing. Spirit had locked-in revenue from being the sole-source supplier of major structures on Boeing’s commercial fleet. Squeeze labor costs, push capital expenditure to the margins, run the production line as hard as the supply agreements allowed, and the cash flow Onex extracted compounded. By 2014, Spirit employed about 13,500 people in Kansas and Oklahoma, meaning the workforce had grown again, but not at the pace of revenue, and not at Boeing-comparable wages.

This is the part of the playbook that doesn’t show up cleanly in either company’s 10-K, because the cost wasn’t being borne in 2005-2014. It was being deferred.

The quality decay that built up over 19 years

The bill came due slowly, then all at once.

From 2018 onward, Spirit ramped 737 fuselage production from the mid-30s per month to over 50 per month, supporting Boeing’s pre-pandemic MAX delivery ramp. Whistleblower depositions in a shareholder lawsuit filed in May 2023, and broadly reported by CBS News, NPR, and Jacobin in 2024, described a culture in which inspectors who flagged defects were pressured to underreport them. One inspector at the Wichita plant said his managers nicknamed him “Showstopper” for slowing deliveries by writing up problems that needed repair.

The first publicly visible signal came in April 2023, when Boeing reported a defect related to the tail fin fittings on some 737 aircraft. In August 2023, Boeing discovered Spirit had delivered MAX fuselages with mis-drilled rivet holes in the aft pressure bulkhead, the heavy structural dome that holds cabin pressure. By October 2023, Spirit fired CEO Tom Gentile and replaced him with Pat Shanahan, a former Boeing manufacturing executive.

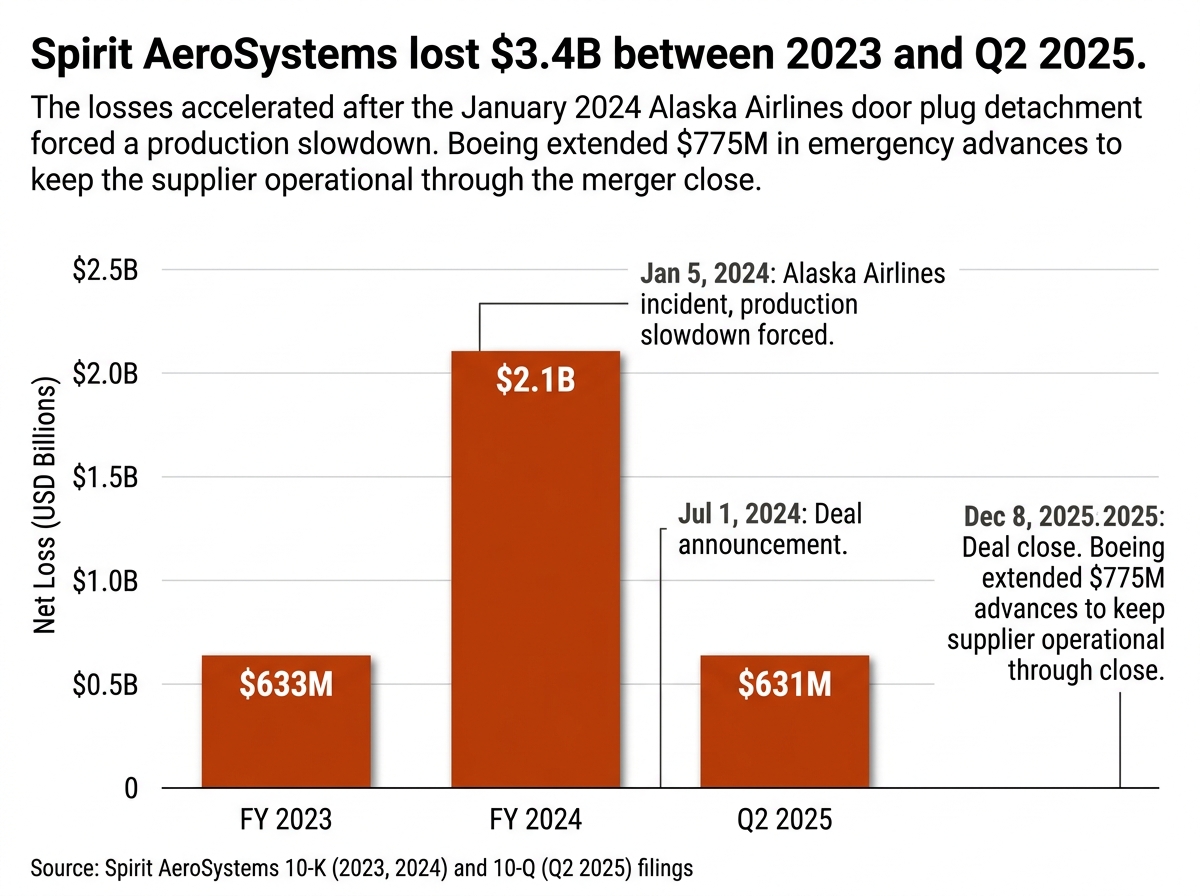

Then, on January 5, 2024, a door plug on an Alaska Airlines 737 MAX 9 detached at 16,000 feet over Portland, Oregon. The FAA grounded all 737 MAX 9s, then ran a six-week audit of both Boeing and Spirit. The audit findings, surfaced by the New York Times in March 2024, included Spirit mechanics using a hotel key card to check a door seal and Dawn dish soap as a “lubricant” in the fit-up process. Of 13 product audits at Spirit, seven failed. Of 89 audits at Boeing, 33 failed, with 97 documented instances of non-compliance.

By the time Boeing announced the reacquisition agreement on July 1, 2024, the picture was settled: the supplier whose value Onex had extracted was no longer capable of supplying the quality Boeing needed at the volumes Boeing needed. The 19-year experiment in supply chain financialization had broken its core asset.

The deal terms: what shareholders actually approved

The reacquisition was structured as an all-stock transaction. Spirit shareholders received Boeing common stock at a fixed ratio of $37.25 in Boeing stock per Spirit share, subject to a collar mechanism: 0.18 Boeing shares per Spirit share if Boeing’s 15-day VWAP was at or above $206.94, 0.25 Boeing shares per Spirit share if VWAP was at or below $149.00.

The headline numbers:

- Equity value: Approximately $4.7B

- Enterprise value (including assumed net debt): Approximately $8.3B

- Premium: $37.25 per share represented a 30% premium to Spirit’s $28.60 closing price on February 29, 2024, the last trading day before deal talks went public

Boeing also acquired all of Spirit’s Boeing-related commercial operations, including 737 fuselages and major structures for the 767, 777, and 787 programs. Spirit’s defense work was carved into a separate non-integrated subsidiary, Spirit Defense, that continues operating as an independent supplier to other defense customers. Spirit’s Belfast operations became Short Brothers, a Boeing subsidiary. Spirit’s Airbus-related work was divested to Airbus directly, and the Malaysia facility was divested to Composites Technology Research Malaysia, both as conditions imposed by the EU Commission and the FTC.

The deal closed on December 8, 2025, about six months later than originally planned, with regulatory clearances dragging into October (EU) and December (FTC) of 2025. Roughly 15,000 Spirit employees joined Boeing.

What’s notable about the all-stock structure: Boeing’s equity holders effectively absorbed the deal cost via dilution rather than balance-sheet cash deployment, which preserved Boeing’s stretched liquidity (it ended Q1 2026 with $9.4B in cash against $47B in debt). It also meant Spirit shareholders got Boeing equity at the moment Boeing’s own commercial division was still posting losses; they’re now exposed to whatever happens to the BCA margin recovery, which is the next chapter.

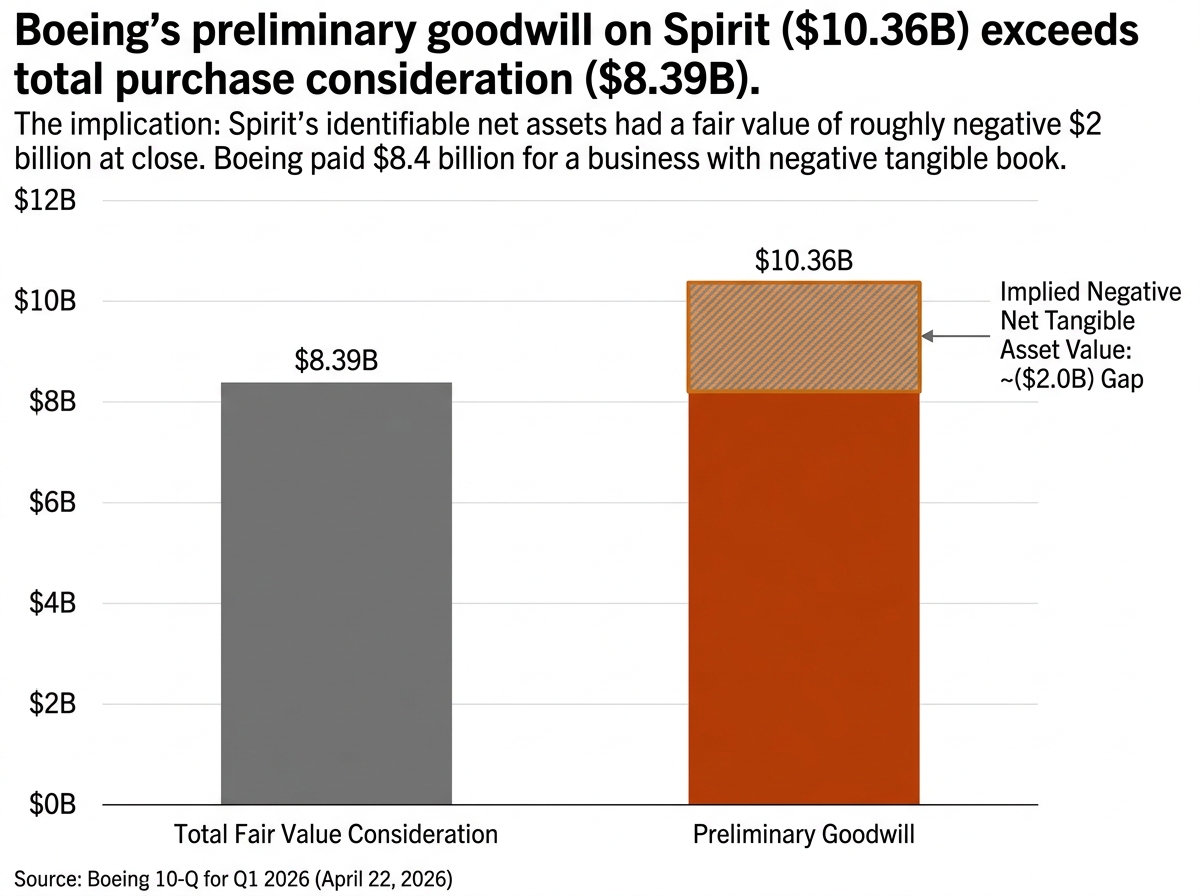

The single number that tells the financialization story: $10.36B in goodwill

Boeing’s Q1 2026 10-Q filing contains a number that almost no mainstream coverage has highlighted but that compresses the entire financialization-reversal thesis into one line item.

Total fair value consideration for the Spirit acquisition: $8.39B. Preliminary goodwill recognized: $10.36B.

Goodwill exceeds the purchase price by roughly $2B.

That math only works in one scenario: the identifiable net assets Boeing acquired had a negative fair value of approximately $2B at close. In other words, when Boeing’s accountants added up everything tangible and identifiable they were getting, property, plant, equipment, inventory, intellectual property, customer relationships, and subtracted everything they were assuming, debt, pension liabilities, deferred losses on unprofitable customer contracts, the answer was negative $2B.

Boeing paid $8.4B for a business whose net tangible assets had a fair value of negative $2B.

The accounting convention for that kind of acquisition is to push the difference into goodwill, where it sits on the balance sheet until management decides to test it for impairment. If the integration goes well and the synergies materialize, the goodwill stays on the books. If it doesn’t, expect a multi-billion-dollar non-cash impairment charge in some future quarter. Boeing has done this before — the company sank $6.5B into halted 787 deliveries between 2020 and 2022 due to fuselage join issues at Spirit, partly recoverable, partly not.

The number tells you everything about what 19 years of supplier financialization produces. Spirit’s identifiable net assets, the actual factories, machinery, and ongoing contracts, were worth less than zero by the time the parent had to take it back.

The integration cost ran over budget, and the timing should make shareholders nervous

Boeing’s communication around the Spirit integration cost is a case study in how the disclosure framework allows bad news to be parceled out in ways that lag the moment shareholders actually pay for the deal.

July 1, 2024: Boeing and Spirit announce the merger agreement. Boeing’s deal materials disclose ~$1B in expected annual revenue addition from the deal but no specific integration cost figure. The S-4 registration statement and proxy materials filed in subsequent months reference “anticipated benefits” and “integration costs” in the standard forward-looking risk-factor language but don’t put a dollar figure on the integration cost expected.

December 8, 2025: Deal closes. Boeing receives full access to Spirit’s books, contracts, and operations.

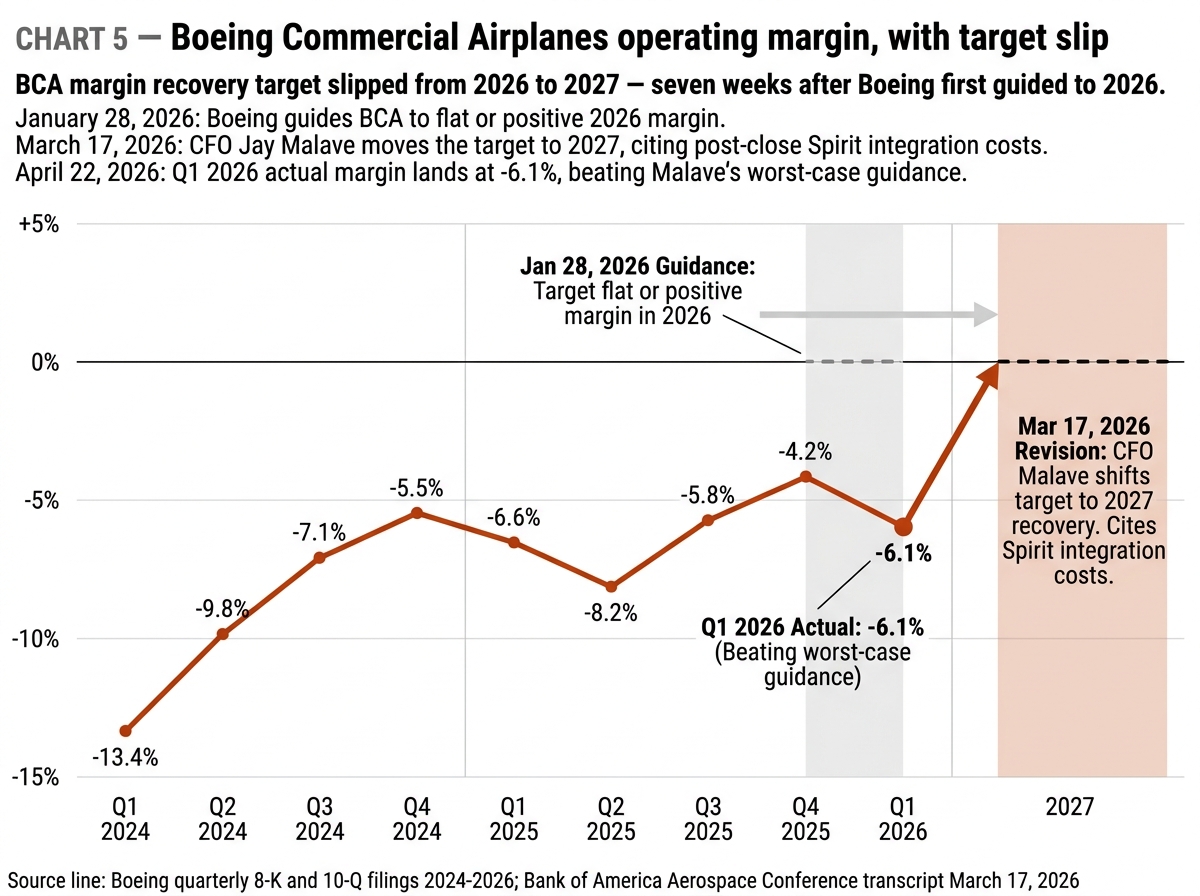

January 28, 2026 (Q4 2025 earnings): CFO Jay Malave discloses that Boeing expects to spend roughly $1B in 2026 specifically on the Spirit integration. Total 2026 spending is projected at about $4B, up from $1.9B in 2025. BCA is guided to flat or positive operating margin in 2026.

March 17, 2026 (Bank of America Aerospace Conference): Six weeks later, Malave walks back the BCA margin guidance. Recovery is now 2027, not 2026. Q1 2026 BCA margin is guided to between -7% and -8.5%. He explains: “We did have to fold in their accounting, which does cause a little bit of pressure on the BCA margins… You don’t get access to all the information until you actually close. And so there was cost.”

April 22, 2026 (Q1 2026 earnings): Actual BCA margin comes in at -6.1% on a $563M operating loss, better than the worst-case guidance from March, but still firmly negative and well below the flat-or-positive target Boeing held until Q1 2026 itself.

The pattern is clean. Until the deal closed, Boeing’s executives had limited visibility into Spirit’s actual operational and accounting state, or had visibility but no obligation to publicly disclose it. Within seven weeks of close, the integration cost picture had shifted enough to push the BCA margin recovery target out by a full year. The shareholders who voted to approve the issuance of $4.7B in Boeing stock to acquire Spirit didn’t have access to that information when they voted.

This is the disclosure structure working as designed. It’s also the same structural feature of the public markets that allowed the 2005 financialization trade to look brilliant for the first decade, the costs of supplier under-investment didn’t show up in either company’s quarterly results until they did, all at once.

Why the Malave quote is the most important sentence in the deal

“You don’t get access to all the information until you actually close. And so there was cost.”

That sentence is doing a lot of work, and it’s worth reading slowly.

It is, in one reading, simply factual. M&A due diligence has limits. Sellers control what data flows through the data room. Material adverse change clauses give the buyer some recourse but require litigation to invoke. Buyers really don’t have full operational visibility until close. This is true for every deal of every size.

But Boeing didn’t acquire a company it had a casual commercial relationship with. Boeing was Spirit’s largest customer, accounting for about 60-70% of Spirit’s revenue depending on the year. Boeing had personnel embedded in Spirit’s Wichita facility from at least March 2024 onward, doing fuselage inspection before shipment. Boeing was extending Spirit emergency financial advances starting in 2024, $425M under the April 2024 MOA, plus a separate $350M bridge term loan, which required Spirit to share extensive financial information with Boeing as a condition of receiving the cash.

In other words: Boeing had vastly more visibility into Spirit’s books, operations, and accounting than any acquirer of any other company would have had. And Boeing’s CFO is on the record saying the post-close cost picture was still materially worse than the pre-close cost picture.

There are two readings. Either Boeing genuinely didn’t know, which says something about how thoroughly Spirit was running deferred-cost accounting that even its largest customer couldn’t see, or Boeing knew and the disclosure framework didn’t require it to say so until earnings released after close. Both readings are damaging to the case that the deal was fairly priced. Both readings indict the same incentive structure that produced the 2005 spinoff: management with quarterly performance pressure, asymmetric upside on stock-based compensation, and a disclosure regime that allows long-tail liabilities to be moved off the income statement until they can’t be.

The broader pattern: financialization templates that won’t survive contact with reality

The Spirit reacquisition is the largest visible reversal of a specific financialization template I’m aware of in current US industrial history. The template runs roughly like this:

- Identify a capital-intensive, unionized, low-margin business unit inside a larger industrial company

- Argue it’s “non-core” and a drag on multiple expansion

- Sell it to a private equity buyer in a leveraged transaction

- Negotiate long-term supply agreements that lock in revenue but transfer operational risk

- Watch the parent company’s stock re-rate on the asset-light story

- Watch the spun-off business squeeze labor and capex to extract returns to PE

- Years later, deal with the consequences

Boeing did this with Spirit in 2005. The company also bought back two of its 787 program suppliers, Global Aeronautica in 2008 and Vought’s South Carolina operations in 2009, when both proved unable to meet quality standards under the same kind of financial squeeze. GE pursued aggressive variants under Jack Welch and Jeff Immelt, which has been partially unwound by current management. Sears unwound its real estate and retail operations into separate entities, with disastrous results.

The Spirit unwind is the cleanest test case in living memory of whether the financialization trade is fully reversible. Everything that’s possible to know about whether the original model worked is now visible in the filings. The 2005 deal looked brilliant for nearly a decade. The structural costs were real but didn’t surface in quarterly results. By 2018, the cracks were visible. By 2024, the cracks were a door plug at 16,000 feet. By 2025, Boeing was paying nine times the original sale price to undo it.

What’s actually unresolved is whether Boeing can integrate Spirit cleanly enough to recover the goodwill the deal added to the balance sheet. That’s the question worth tracking through 2026 and 2027.

The risks to the financialization-reversal thesis

I’ve argued that the Spirit reacquisition is best understood as a forced unwinding of a 20-year financial engineering bet, and that the same incentives that produced the original deal are now slowing the unwind. That thesis has real risks worth naming.

Risk 1: It really was an operational fix, not a financialization reversal. Boeing executives could plausibly argue that the 2005 spinoff was reasonable at the time and that Spirit’s quality decay was the result of specific managerial failures at Spirit, not a structural feature of the spinoff itself. Reasonable people can hold this view. The counter is that Spirit’s quality issues started visibly emerging in 2018, the moment production rates climbed and the financial squeeze tightened, and that the structural incentive of a PE-controlled supplier to defer capex against locked-in supply agreements is hard to dispute.

Risk 2: Integration may go better than the March 2026 disclosure suggested. Q1 2026 BCA margin came in at -6.1%, beating Malave’s guidance. The 737 line is on track to ramp from 42 to 47 per month this summer. Spirit defects were already down 40% in early 2026. If 2027 BCA margin recovery actually lands on schedule, the goodwill will look more justified.

Risk 3: The acquisition multiple may be defensible if synergies land. $8.3B for a company with roughly $6.3B in revenue is not on its face an exotic multiple, even with negative net tangible assets. If integration unlocks $500M-$1B in annual run-rate cost savings via supply chain consolidation, the deal’s IRR could end up acceptable on a multi-year view. The bear case requires the synergies to underdeliver materially.

Risk 4: Reading too much into one Malave quote. The “you don’t get access to all the information” comment is being read here as the most important sentence in the deal, but executives say things at conferences. The substantive question is whether the integration cost overrun is material, and the public disclosures so far suggest it is, but not catastrophically so.

The thesis I’d defend most strongly is the narrow one: the Spirit reacquisition reversed a 20-year financialization trade that was running on deferred operational cost, and the disclosure structure is allowing Boeing to manage the unwind on the same quarterly cadence that produced the original mistake. Whether that’s an investable insight depends on what you do with it.

What to watch in 2026 and 2027

If you’re tracking this story for any reason, equity exposure to BA, supply chain or aerospace adjacency, financialization-reversal as a broader thesis, here are the specific data points worth watching across the next 18 months.

1. Quarterly BCA operating margin progression. The 2027 flat-or-positive target is the headline number. Each quarter’s print is a vote on whether Boeing is on track. A continued miss in Q2 or Q3 2026 would suggest the integration cost picture is worse than even Malave’s revised March 2026 framing.

2. Final purchase price allocation in Q2 2026 10-Q. The $10.36B preliminary goodwill is preliminary. The final allocation may shift the mix between goodwill, intangibles, and the negative net tangible asset line. Watch whether the goodwill figure goes up (worse) or down (better).

3. 737 MAX 7 and MAX 10 certification timing. Both certifications have slipped repeatedly. Boeing’s Q1 2026 disclosure now expects certification in 2026 and first delivery in 2027. Slippage past that window adds program-level losses Boeing has been deferring.

4. 737 production rate progression. From 42/month now to 47/month this summer to 52/month thereafter via the new Everett line. Each rate increase is a quality test of the integrated Spirit operations.

5. Goodwill impairment testing. Annual testing happens at year-end. A first impairment charge would be the clearest possible signal that the deal’s economics are not landing where management projected.

Boeing didn’t pay $4.7B to fix a supply chain problem. It paid $4.7B to unwind a 20-year financial-engineering bet, and the same incentive structure that created the bet is now slowing the unwind. The deal is best understood not as Boeing fixing its supply chain, but as Boeing being forced to absorb the 20-year cost of a financial engineering trade that mainstream coverage applauded in 2005 and is now still applauding as a “supply chain fix” in 2025.

FAQ

Why did Boeing sell Spirit AeroSystems in 2005?

Boeing’s then-CEO Harry Stonecipher was running an asset-disposal program designed to make the company “asset-light” by selling off capital-intensive, unionized manufacturing operations and focusing on design, engineering, and final assembly. The Wichita and Tulsa fabrication facilities, which made the entire 737 fuselage and major structures for other Boeing jets, were sold to Onex Corporation for $900M in cash plus the transfer of about $100M in liabilities. The deal was praised on Wall Street at the time as a textbook financial engineering trade.

How much did Boeing pay to buy back Spirit AeroSystems?

Boeing paid $4.7B in equity (all-stock at $37.25 per Spirit share) and $8.3B including assumed debt. The deal closed on December 8, 2025. Spirit shareholders received Boeing common stock at an exchange ratio between 0.18 and 0.25 Boeing shares per Spirit share, subject to a collar based on Boeing’s 15-day VWAP.

Did Boeing make money on the original Spirit spinoff?

In the short term, yes. Boeing received approximately $900M in cash, transferred about 9,500 employees and the long-tail pension liabilities attached to them, and recognized roughly $538M in pre-tax non-cash charges across 2005. The company’s stock multiple expanded as the asset-light story took hold. In the long term, Boeing paid roughly nine times the original sale price to buy the same business back 20 years later, having absorbed years of program disruption, two MAX crashes, and a door plug detachment in between. Net economic return on the 2005 trade is deeply negative when properly accounted for.

What did Spirit AeroSystems lose before Boeing reacquired it?

Spirit posted a $633M loss in 2023, a $2.1B loss in 2024, and continued losses into 2025 (including a $631M loss in Q2 2025 alone). The company’s cash reserves fell to $206M by mid-2024, a level that would have made independent operations impossible without external support. Boeing extended a $425M advance under the April 2024 Memorandum of Agreement, plus a $350M bridge term loan to keep Spirit operational through the merger close. Airbus also extended approximately $152M in support for its programs.

Will the Spirit acquisition fix Boeing’s quality problems?

It depends on execution. Boeing has owned Spirit’s primary commercial operations only since December 2025. Spirit defects were already down 40% in early 2026, per CFO Malave’s March 2026 disclosure, and the 737 production rate is increasing. Bringing fuselage manufacturing back in-house removes one layer of supplier-Boeing communication and accountability gaps. But the same management approach that produced the 2005 spinoff is now responsible for the integration, and the post-close disclosure that integration costs ran higher than expected is a warning sign about how cleanly the unwind will be managed.

When will Boeing’s commercial airplanes division return to profitability?

Boeing’s most recent guidance is 2027. CFO Jay Malave revised this from 2026 at the Bank of America Aerospace Conference on March 17, 2026, citing Spirit integration costs as the primary reason for the delay. Q1 2026 BCA operating margin came in at -6.1% on a $563M loss, better than Malave’s worst-case guidance of -7% to -8.5% but still firmly negative. Whether the 2027 target holds depends on integration cost progression, 737 production rate increases, and 737 MAX 7/10 certifications.

This analysis is based on Boeing and Spirit AeroSystems public SEC filings (8-K and 10-Q), Boeing investor communications, the July 2024 merger agreement and proxy materials, FAA audit reports as reported by the New York Times, whistleblower depositions reported by CBS News and NPR, the Bank of America Aerospace Conference of March 2026, and reporting from Reuters, Bloomberg, the Seattle Times, Manufacturing Dive, Flight Global, Simple Flying, and The Air Current.

— Hamza, Footnote Brief