The Wall Street thesis that Ozempic would empty gyms collapsed in plain sight. Here is what the 2025 filings actually show.

The 60-second version

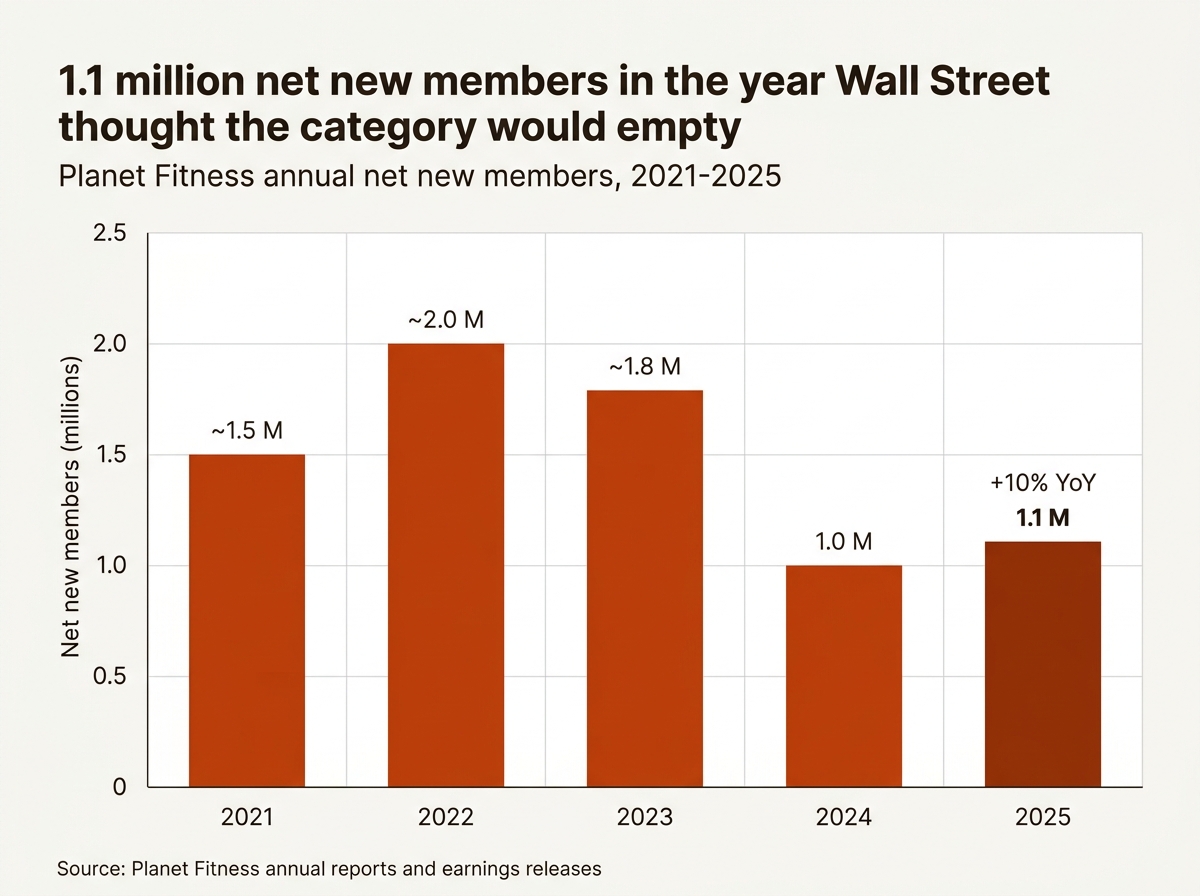

In late 2023, gym stocks dropped on a Wall Street thesis that GLP-1 weight-loss drugs like Ozempic, Wegovy, and Mounjaro would empty fitness facilities. The thesis was that thin people do not need to work out. Three years of operating data have demolished that view. Planet Fitness added 1.1 million net new members in 2025 and grew revenue 12.1% to $1.3 billion. Life Time grew revenue 14.3% to $2.995 billion and tripled the footprint of its in-club Miora longevity clinics, which now prescribe GLP-1s alongside personal training. Equinox raised $1.8 billion in capital after launching a GLP-1 protocol. The contrarian point is that the GLP-1 patient is not a lost gym customer but the most pre-qualified one in the industry, because the drug strips muscle along with fat and the only way to keep that muscle is strength training. The gym category did not survive GLP-1s. It absorbed them. What investors should watch for next is how the operators who built clinical infrastructure during the panic, Planet’s Ro partnership, Life Time’s Miora, Xponential’s Lindora, defend their economics against low-price competitors who did not.

Skip to the section that interests you most

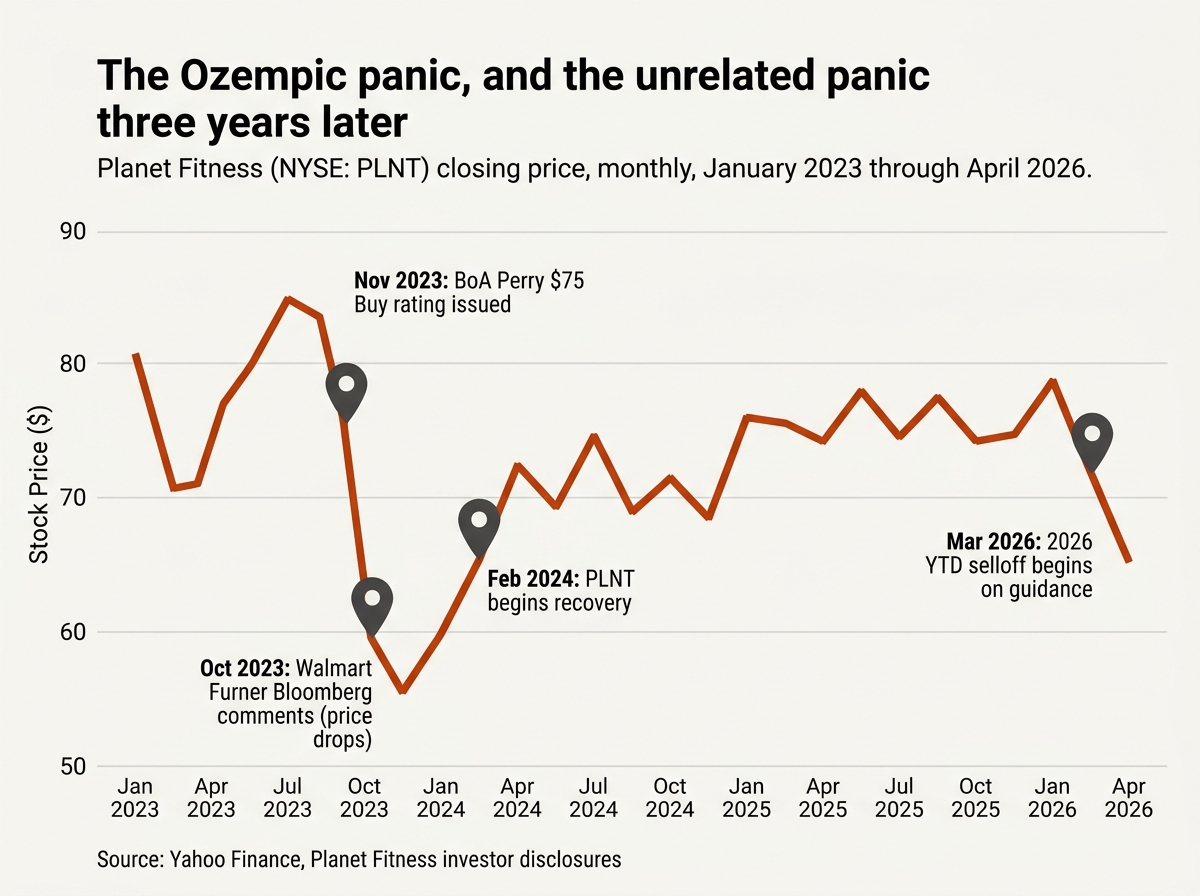

The 2023 panic that emptied gym stocks

The story starts at Walmart, of all places. On October 4, 2023, U.S. CEO John Furner told Bloomberg that customers picking up Ozempic and Wegovy at the company’s pharmacies were buying meaningfully less food. “We definitely do see a slight change compared to the total population, we do see a slight pullback in overall basket. Just less units, slightly less calories.” Walmart was running anonymized comparisons between shoppers filling GLP-1 scripts and their statistical peers, and the appetite-suppressing drugs appeared to be visibly affecting basket size.

That offhand interview detonated a sector-wide repricing.

Within weeks, the GLP-1 contagion thesis had spread far beyond food. Snack and beverage stocks dropped. Restaurant stocks dropped. Then, for reasons that look strange in hindsight, fitness stocks dropped too. Planet Fitness slid more than 30% across the months that followed. Piper Sandler analyst Korinne Wolfmeyer captured the prevailing sentiment to CNBC in November 2023: gyms, she said, were getting “looped into the group of sectors that could get hurt by GLP-1s.”

The implicit reasoning was simple, and simple reasoning is often what powers a market panic. People who lose weight on a drug do not need to go to the gym. People who do not want to lose weight the hard way do not go to the gym either. So a drug that makes weight loss easy is a drug that empties the gym.

It was not a unanimous view. Bank of America’s Alexander Perry held a Buy rating on Planet Fitness with a $75 price target as early as November 7, 2023, citing “early signs of benefits to fitness industry from increased usage of GLP-1 drugs.” BMO’s Simeon Siegel was telling reporters that “in a world where GLP-1s become widely accessible, gyms from Planet Fitness all the way up to the highest-end brands are likely going to pull out marketing campaigns looking to boost their membership bases.” But the bullish notes were swimming against the tape.

Three years and a stack of 10-Ks later, the bears have lost the argument cleanly.

What Planet Fitness’s 2025 numbers actually showed

Planet Fitness reported full-year 2025 results on February 24, 2026. The headline figures are not subtle.

Revenue came in at $1.3 billion for the year, up 12.1% over 2024. The company added 1.1 million net new members, a 10% increase over the prior year. Total membership reached 20.8 million across nearly 2,900 clubs. Adjusted EBITDA grew to $551.6 million from $487.7 million the year before. System-wide same-club sales increased 6.7% on the year, with Q4 same-club sales up 5.7%. The company opened 181 new clubs, a record. Black Card penetration reached an all-time high of 66.5%.

The company executed a price increase on its Classic Card membership through the year and still added more members than it had in any of the prior several years. That is the kind of pricing power that does not happen in a category being disrupted by a substitute product. It happens in a category that is gaining share.

Planet Fitness CEO Colleen Keating, on the Q4 earnings call, told investors that a franchisee survey indicated roughly half of people who take a GLP-1 medication also consider a gym membership. The data point was not buried. It was the strategic frame for the entire 2026 outlook. Keating’s argument was straightforward: as GLP-1s become more accessible, through lower pricing and the rollout of pill formats like orforglipron, the addressable population for entry-level fitness expands rather than contracts.

Read the call transcript carefully and you find a company whose CFO is explaining why same-club sales should decelerate to 4-5% in 2026 (an extended equipment replacement cycle plus the sale of eight California corporate clubs to franchisees), and whose CEO is using nearly all of her airtime to talk about positioning the chain at the center of a metabolic-health movement. The disconnect tells you what management actually thinks the long-term story is.

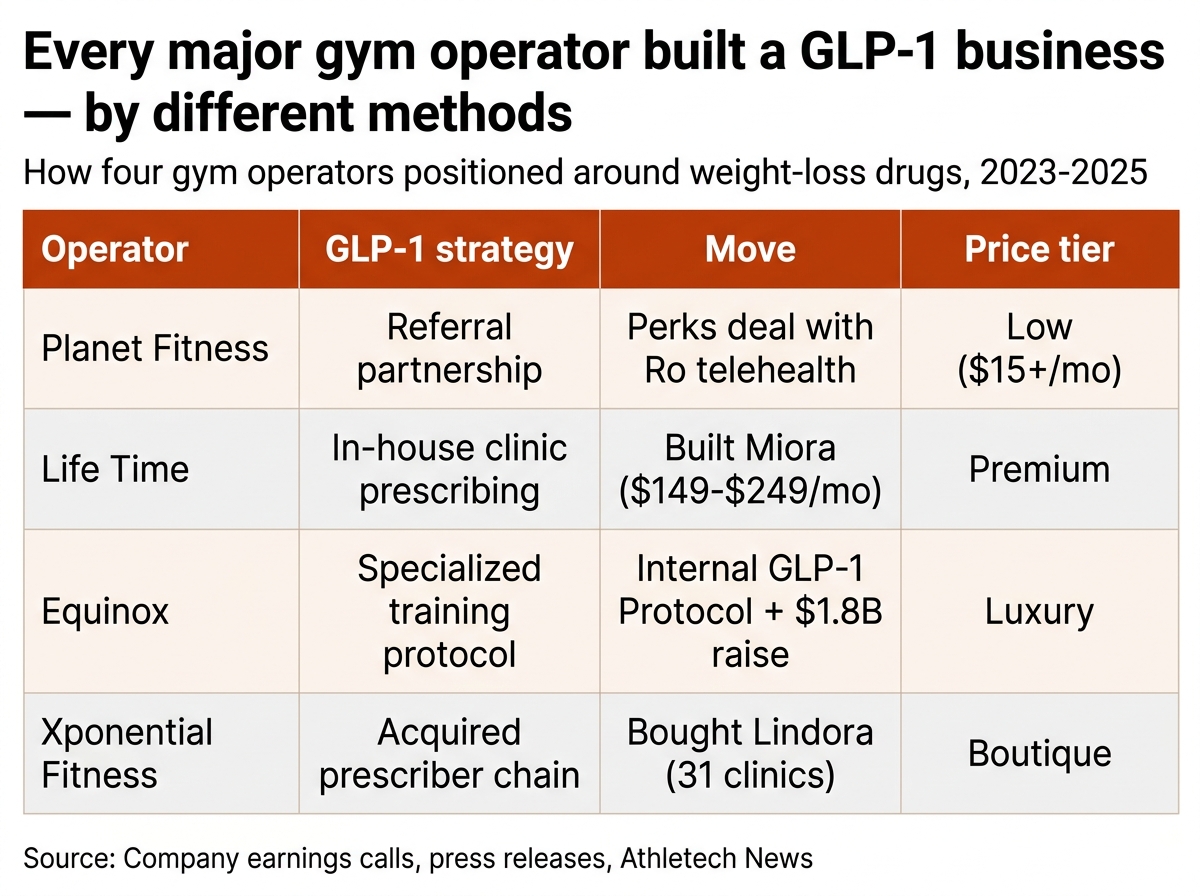

Why the Planet Fitness × Ro partnership matters

The most strategically interesting move Planet Fitness made in 2025 was not opening 181 new clubs. It was a marketing partnership.

In 2025, Planet Fitness announced a Perks program tie-up with Ro, the direct-to-consumer telehealth company that prescribes GLP-1 medications through an app and fills them through a vertically integrated pharmacy network. Ro’s most visible patient ambassadors are Serena Williams, who lost 31 pounds on Zepbound through Ro’s program and joined as a multi-year ambassador in August 2025, and Charles Barkley, who lost 65 pounds and joined in April 2025. Williams’s husband, Alexis Ohanian, is an investor in Ro and sits on the company’s board.

Planet Fitness’s Perks deal gives the chain’s 20.8 million members discounts on Ro’s services in exchange for funneling Planet’s customer base toward Ro’s prescribers. Keating, on the Q4 call, called it “our most successful Perks program yet”, a meaningful comparison given that Planet has been running Perks for years across categories from apparel to food. The partnership is, in functional terms, the integration of a gym chain into the GLP-1 distribution stack.

What makes this strategically clean is the symmetry. Ro gets exposure to 20 million-plus fitness-minded members; Planet gets discounts that strengthen retention and a referral pipeline of new GLP-1 patients who, per Keating’s own data, are roughly 50% likely to consider a gym membership. The gym chain that was supposed to be the canary in the GLP-1 coal mine is now a downstream channel for the company that prescribes the drug.

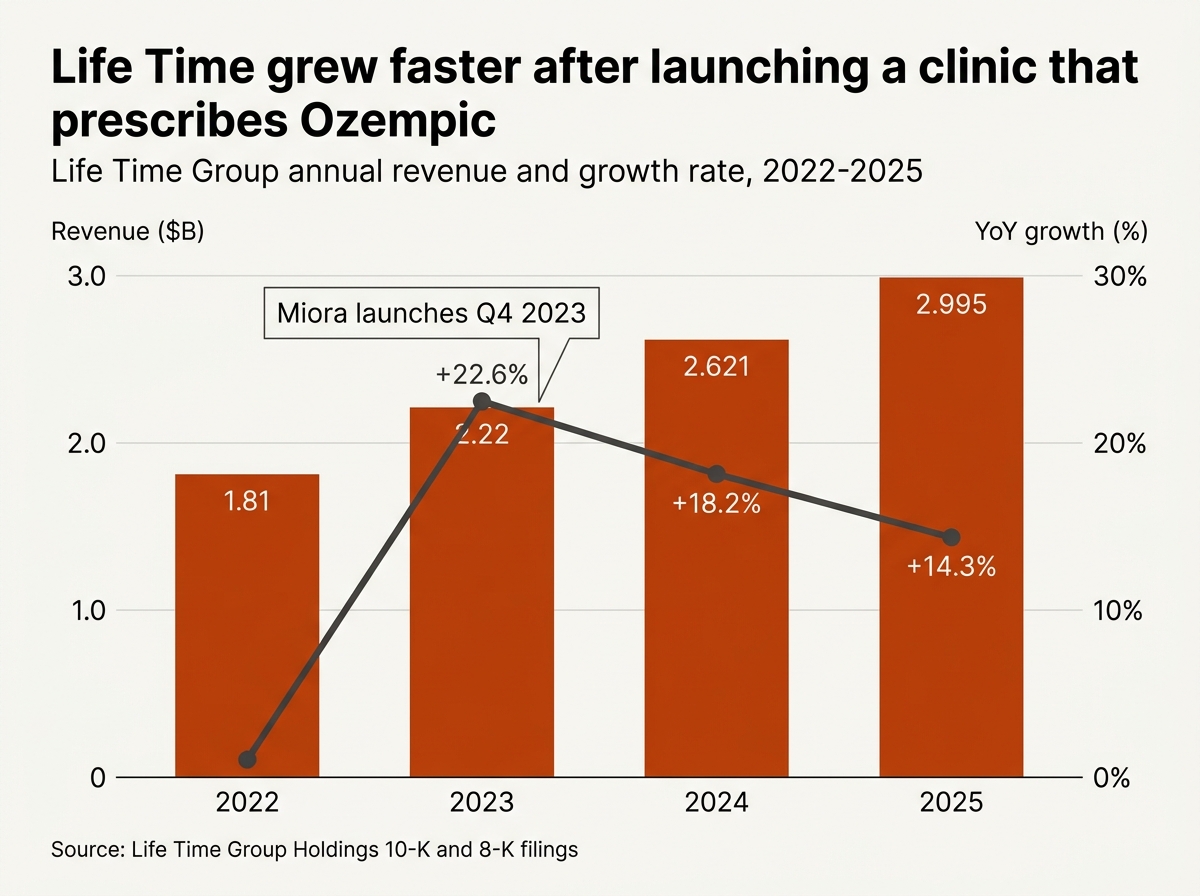

Life Time built a pharmacy. Then it built six more.

If Planet Fitness is the low-end of the gym industry’s GLP-1 absorption strategy, Life Time is the high end, and Life Time has been more aggressive.

Life Time launched Miora, an in-club longevity and performance clinic, in November 2023 at its Target Center flagship in Minneapolis. The clinic was a pilot. Over the next 24 months, the model ramped through Evanston, Illinois, and across what management now describes as 7 or 8 locations spanning multiple states.

What does Miora actually do? It is not a gym. It is a clinic that operates inside a Life Time facility, runs a 70-plus biomarker blood panel for $400 to $800, and prescribes a personalized protocol that can include GLP-1 medications, peptides, hormone replacement therapy, IV therapy, red-light therapy, and supplementation, at a recurring monthly cost of $149 to $249. The Miora medical team includes MDs, physician assistants, nurses, and registered dietitians. Prescriptions are filled through licensed U.S. compounding and specialty pharmacies. The bloodwork is interpreted using Life Time’s proprietary Metabolic Code system, developed by chief science officer Jim LaValle.

Life Time’s full-year 2025 results, reported February 24, 2026, gave the strategic context for Miora’s rollout. Total revenue grew 14.3% to $2.995 billion. Net income grew 139.2% to $373.7 million. Q4 net income alone was up 230.6% year-over-year. Comparable center revenue grew 9.9% in Q4, and revenue per center membership reached $882, up 10.8% year-over-year. Average monthly dues hit $223. Net debt leverage improved from 2.3x to 1.6x. The company announced a $500 million share repurchase program the same day.

CFO Erik Weaver told analysts that Miora moved from 2 locations a year ago to 7 or 8 today, and that “fully opened” Miora locations are ramping faster than the original financial models projected. CEO Bahram Akradi went further, telling the call that future club designs are being built with Miora space included by default, “this is the one program that we have tested, and I believe it’s gonna work extremely well.” Miora is not a side project. It is being designed into the company’s real estate.

The economics of stacking a clinic inside a gym are unusually attractive. The clinic monetizes a customer the gym already acquired and retained. The gym’s facility, brand, and personal training infrastructure pre-qualify the clinic’s customers. There is no second customer-acquisition cost. There is no second real-estate cost. The protein-and-strength program the patient needs is already on premise. And, quietly, the clinic gives Life Time a recurring high-margin revenue stream priced 5-10x higher than the underlying gym membership.

Equinox raised $1.8 billion. Xponential bought a clinic chain.

Two operators in the broader middle of the gym market made similar moves with different financing structures.

Equinox, the privately held luxury chain, debuted its “GLP-1 Protocol” in early 2024, a personal training and nutrition system designed specifically for clients on weight-loss medications. The protocol, developed in partnership with Equinox’s new Health Advisory Board of doctors and fitness professionals, focuses on muscle preservation through resistance training, structured nutrition, and recovery work. By March 2024, Equinox parent Equinox Group had raised $1.8 billion in new capital and credit for refinancing and expansion. The company has since announced more than 25 new gyms in major markets, with E by Equinox flagship locations leading the strategy. The Hudson Yards location’s Michael Crandall, who developed and piloted the protocol, has become one of the public faces of the strategy.

Equinox’s choice was deliberate. The chain has not become a prescriber. It is not a clinic. It positioned itself as the elite training partner for the GLP-1 patient, a positioning that is consistent with Equinox’s pre-existing brand and that lets it charge $160-plus per personal-training session to a customer with an immediate medical need to preserve muscle.

Xponential Fitness, parent of Club Pilates, Pure Barre, Rumble, RowHouse, and other boutique fitness franchises, went the other direction. In December 2023, the company acquired Lindora, a chain of 31 weight-loss medical clinics in Southern California and Washington state staffed with physicians who prescribe GLP-1s, hormone replacement therapy, and IV hydration. The acquisition gave Xponential something neither Planet Fitness nor Equinox had: vertical integration into prescription-writing infrastructure. The boutique operator did not partner with a clinic. It bought one.

Then there is the WeightWatchers data point, which is worth noting precisely because it cuts against the gym-industry pattern. WeightWatchers acquired Sequence, a GLP-1 telehealth business, for over $100 million in 2023, but the company’s stock has been crushed across the same period as it has struggled to convert pre-Ozempic dieters into GLP-1 customers. The contrast matters. The acquisition path that worked was for operators who already owned an in-person facility and a captive audience. WeightWatchers, which had neither in scale, has not made the model work.

Why GLP-1 patients are the highest-quality gym customers in the industry

The Wall Street thesis that animated the 2023 selloff assumed gyms sold weight loss. That is the wrong model.

Gyms sell muscle. They sell strength training, group fitness, recovery, community, accountability, and, at the high end, personal training and longevity care. Weight loss is a customer goal, not a product. The drug is now better than the gym at delivering weight loss. But the drug is worse than the gym at delivering everything else, and several things the gym delivers are now medically required for the GLP-1 patient.

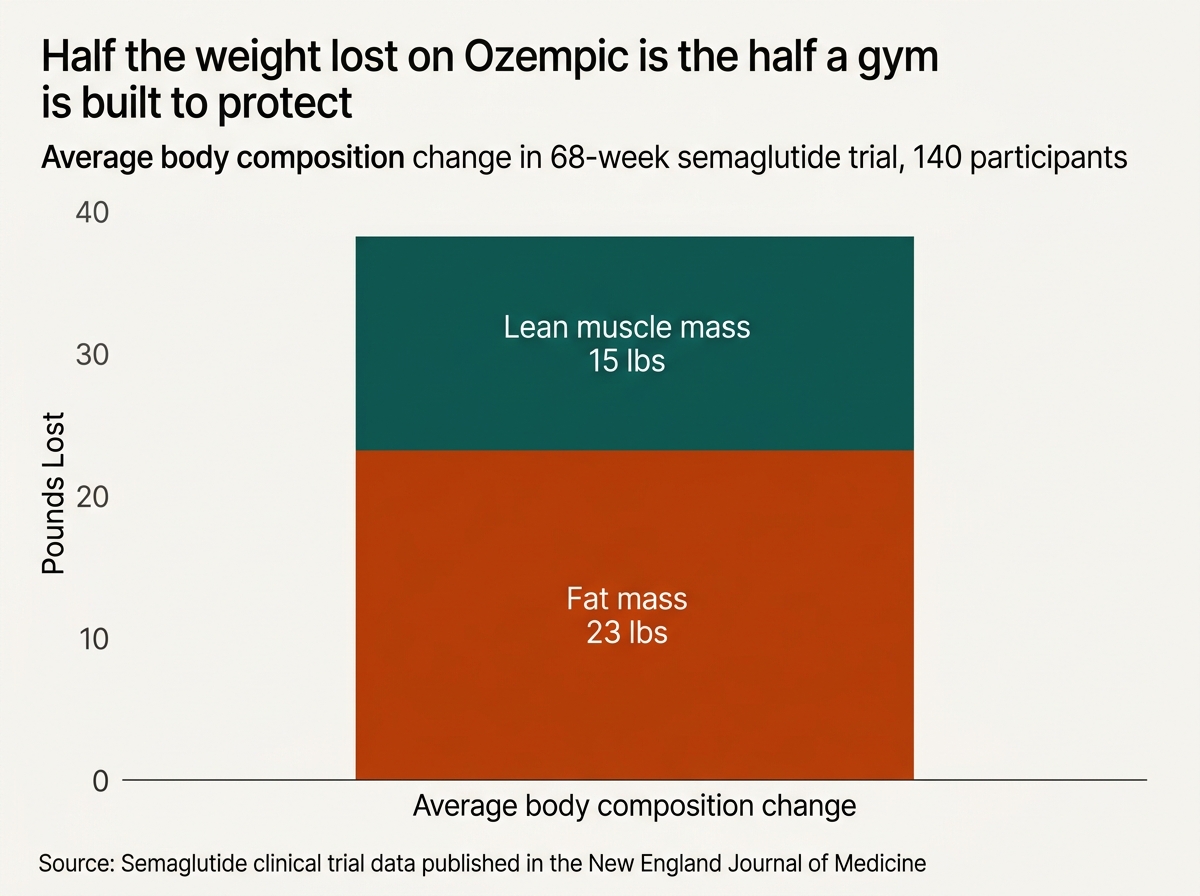

The clinical evidence is unambiguous. Semaglutide trials show 14% to 20% body weight loss on average over a year of treatment. But that loss is not pure fat. A widely-cited 68-week clinical trial of 140 participants on semaglutide found that participants lost approximately 15 pounds of lean muscle mass alongside 23 pounds of fat. The lean muscle loss is the medical problem inside the GLP-1 success story. Muscle drives basal metabolic rate, glucose disposal, mobility, and, over a longer horizon, independent function in older patients. Lose enough of it and you create a long-term metabolic disaster that any well-trained endocrinologist will warn against.

Every GLP-1 prescriber in the country now tells the patient the same thing: lift weights, eat protein, get to a gym. That is the conversation Planet Fitness, Life Time, Equinox, and Xponential are walking into.

The compounding effect is what makes the GLP-1 patient an unusually high-quality gym customer. They have a medical reason to be there, not a vanity reason that gets dropped after January. They are losing weight visibly and feeling more capable, which (per Morgan Stanley’s February 2024 survey of ~300 GLP-1 users) tracks with weekly workout rates jumping from 35% to 77% after starting the drug. The same survey found 50% of GLP-1 users were gym members, with 70% having joined in the last 12 months, the same window in which most started a GLP-1.

This is the empirical core of why gyms are growing. The drug is producing a strength-training customer.

The gym is no longer a fitness business. It is metabolic-health infrastructure.

The category implication of all this is bigger than any individual operator’s earnings beat.

The clinic and the gym used to be different categories. Different P&Ls, different real estate, different regulatory environments, different customer-acquisition channels. They are not different categories anymore. Life Time runs a clinic. Xponential owns a clinic chain. Planet Fitness has a referral relationship with the largest direct-to-consumer GLP-1 prescriber in the country. Equinox runs a coaching protocol designed by an internal medical advisory board. Even Costco, through its partnership with Sesame, now offers GLP-1 access alongside its membership.

The frame that explains all of this is metabolic-health infrastructure. The gym chain is becoming the physical layer in a stack that includes telehealth, prescribing infrastructure, lab work, pharmacy fulfillment, and personal coaching. The drug is one node in that stack. The gym is another. The two reinforce each other rather than compete.

That is a bigger and more durable category than fitness. Fitness was a category that depended on consumer New Year’s resolutions and discretionary spending. Metabolic health is a category that depends on chronic disease management, longevity care, and a population that the CDC says is 42% obese and rising. The total addressable market is structurally larger.

This is also why Planet Fitness’s stock-market story is so much more complicated than the operating story.

The risks to the metabolic-health-infrastructure thesis

The bull case is not airtight. Three honest challenges:

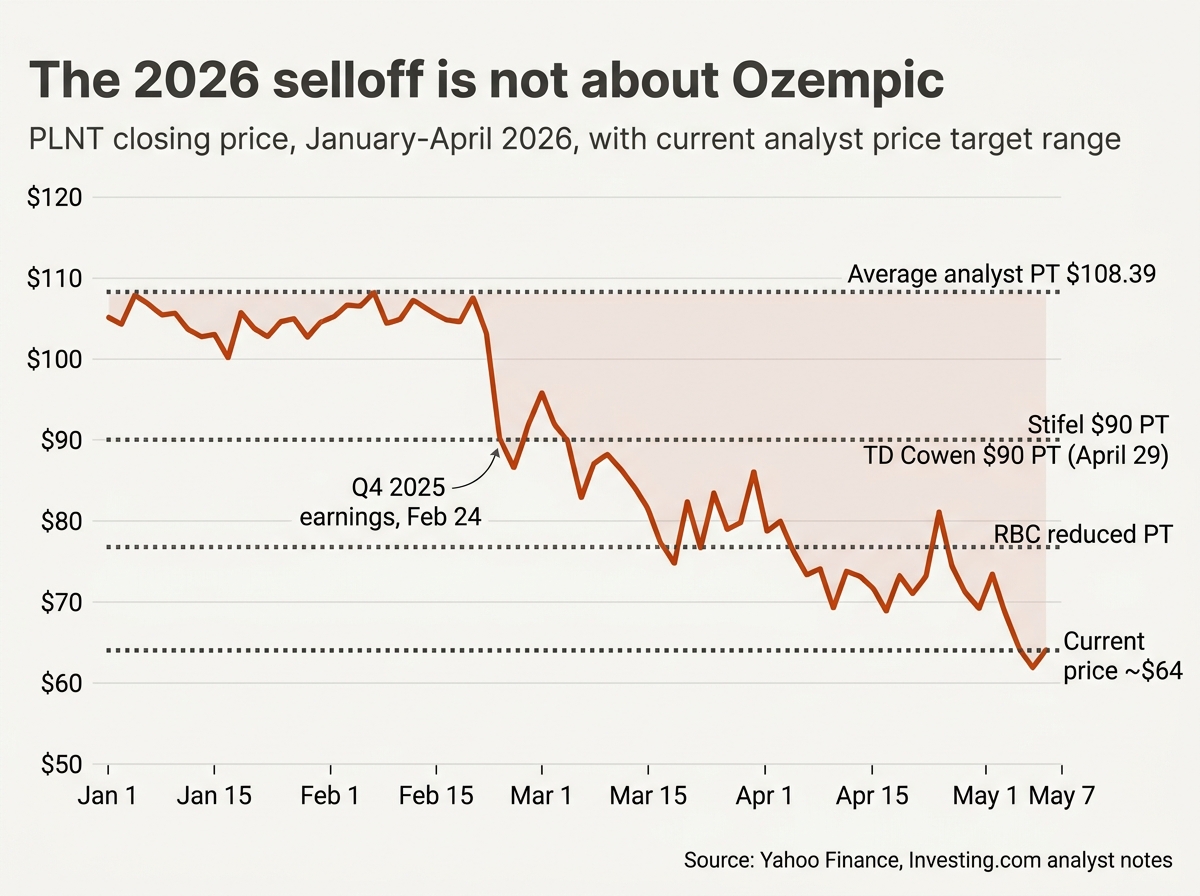

1. The stock market does not believe it yet. Planet Fitness shares are down approximately 40% year-to-date in 2026, trading near a 52-week low of $63.88 as of late April. TD Cowen lowered its price target to $90 from $100 on April 29, 2026. RBC Capital cited “elevated uncertainty” ahead of the company’s Q1 2026 report scheduled for May 7. The market’s concerns are not about GLP-1s, they are about decelerating same-club sales (guided to 4-5% in 2026, down from 6.7% in 2025), intensifying competition from Crunch Fitness and EoS Fitness in the high-value, low-price segment, and the mechanical revenue drag from selling eight California corporate clubs to franchisees. If those concerns persist, operating success and stock performance can stay disconnected for a long time.

2. The Miora model is unproven at scale. Life Time has 7 or 8 Miora locations against more than 180 clubs. Akradi’s commentary suggests “knick-knack” construction and permitting delays at several locations, and the model still needs to prove out the unit economics across a broader real estate footprint and across state-by-state medical regulations that vary considerably for telehealth and prescribing. The Miora opportunity is real; the execution is early.

3. Payor coverage and oral GLP-1s could change the cost curve. The economic story in metabolic-health infrastructure depends partly on GLP-1s remaining expensive enough that patients value the surrounding ecosystem. As insurance coverage expands and oral formulations like orforglipron come to market at lower price points, the surrounding services have to justify themselves on their own merits, not as the affordable component in an expensive bundle. The Miora $149-$249 monthly fee, the $500-plus bloodwork, the $160-per-session personal training: each has to win on its own value proposition, not on relative pricing against an injectable.

There is also the standard regulatory risk: any meaningful FDA, state-level, or DEA action against compounded or telehealth-prescribed GLP-1s would tighten supply, raise prices, and disrupt the partnership models the gym industry has built around them.

What to watch in 2026 and 2027

A few signals worth tracking, in rough order of importance:

Planet Fitness Q1 2026 earnings, scheduled for May 7, 2026. Net member adds and Black Card penetration will tell you whether the deceleration is GLP-1-related (it shouldn’t be) or competition-related (it likely is). Watch for management commentary on the Ro partnership conversion rates.

Life Time’s Miora location count by Q4 2026. Akradi’s stated plan is to embed Miora into future club designs. If the count moves from 7-8 to 15-plus by year-end, the model is working at unit-economics scale. If it stalls below 12, execution risk is real.

The orforglipron launch and its pricing. Eli Lilly’s oral GLP-1 has shown 12.4% weight loss in trials. A pill formulation at a meaningfully lower price than injectable peers would expand the addressable population dramatically, and would test whether gym partnerships can monetize a wider, lower-spending patient cohort.

Xponential’s Lindora P&L disclosure. Xponential has not yet broken out the clinic chain’s contribution. If the company starts disclosing it, and the unit economics rival or exceed the boutique studio franchise model, the read-across for Life Time is significant.

Whether Crunch Fitness or EoS Fitness announce comparable GLP-1 partnerships. If they do, the moat narrows quickly and the thesis weakens. If they don’t, the operators with clinical infrastructure built during the panic continue to differentiate.

Gyms aren’t fitness businesses anymore. They’re metabolic-health infrastructure, and the drug that was supposed to kill the category just handed the smartest operators a second business model worth billions in incremental high-margin revenue.

Frequently asked questions

Will Ozempic and other GLP-1 drugs hurt the gym industry?

The 2025 operating data suggests the opposite. Planet Fitness added 1.1 million net new members and grew revenue 12.1% to $1.3 billion in 2025. Life Time grew revenue 14.3% to $2.995 billion. Equinox raised $1.8 billion in capital and is opening more than 25 new gyms. The clinical evidence that GLP-1 patients lose lean muscle and need to strength-train to preserve metabolic health makes them an attractive gym customer rather than a lost one.

Why did Planet Fitness stock drop in 2026 if its operations are doing well?

The 2026 stock drop is not about GLP-1s. It is about decelerating same-club sales (Planet Fitness guided 2026 growth to 4-5%, down from 6.7% in 2025), intensifying competition from chains like Crunch Fitness and EoS Fitness, and the mechanical revenue impact of selling eight California corporate clubs to franchisees. The 2023 GLP-1 panic was a misdirection. The 2026 selloff is responding to different, and more legitimate, operating risks.

What is Life Time’s Miora clinic and how does it work?

Miora is a longevity and performance clinic operated inside select Life Time fitness facilities. Members start with a comprehensive blood panel covering 70-plus biomarkers ($400-$800), then receive a personalized protocol from MDs, PAs, RNs, and registered dietitians that can include GLP-1 medications, peptides, hormone replacement therapy, and supplementation. Recurring monthly memberships run $149 to $249. As of February 2026, Life Time operates 7-8 Miora locations and is designing future Life Time clubs to include Miora space by default.

What is the Planet Fitness partnership with Ro?

Planet Fitness’s Perks program signed a partnership with Ro, the direct-to-consumer telehealth company that prescribes GLP-1 medications. Planet Fitness members receive discounts on Ro’s services; Ro receives exposure to Planet’s 20.8 million members. CEO Colleen Keating described it on the Q4 2025 earnings call as “our most successful Perks program yet.”

Are GLP-1 users actually going to the gym?

A Morgan Stanley survey of approximately 300 GLP-1 users in February 2024 found 50% were members of a gym, with 70% of those members having joined within the previous 12 months, the same window in which most started taking the drug. The survey also found that the proportion of GLP-1 users who reported working out weekly rose from 35% before starting the drug to 77% after.

Why do GLP-1 patients need to strength-train?

GLP-1 medications produce 14% to 20% weight loss on average over a year, but a portion of that loss is lean muscle mass. A 68-week semaglutide trial of 140 participants showed roughly 15 pounds of lean muscle loss alongside 23 pounds of fat loss. Muscle preservation requires resistance training and adequate protein intake, which is why endocrinologists almost universally recommend a strength-training program for patients on these drugs.

This analysis is based on Planet Fitness Q4 2025 earnings releases and call transcripts, Life Time Group Holdings 8-K filings and earnings call transcripts, the Ro press release announcing the Serena Williams partnership, Athletech News, CNBC, Bloomberg, NBC News, the New England Journal of Medicine, Morgan Stanley Research notes on GLP-1 consumer impact, and reporting from Quartz, Fast Company, and the Boring Business Nerd newsletter.

— Hamza, Footnote Brief