Federal student loan servicers, Maximus, and the U.S. Treasury are paid under three completely different contracts. Only one of them is structured around the borrower repaying, and that one pays the same whether the borrower thrives or barely hangs on. The July 1, 2026 overhaul cements all three for a decade.

The 60-second version

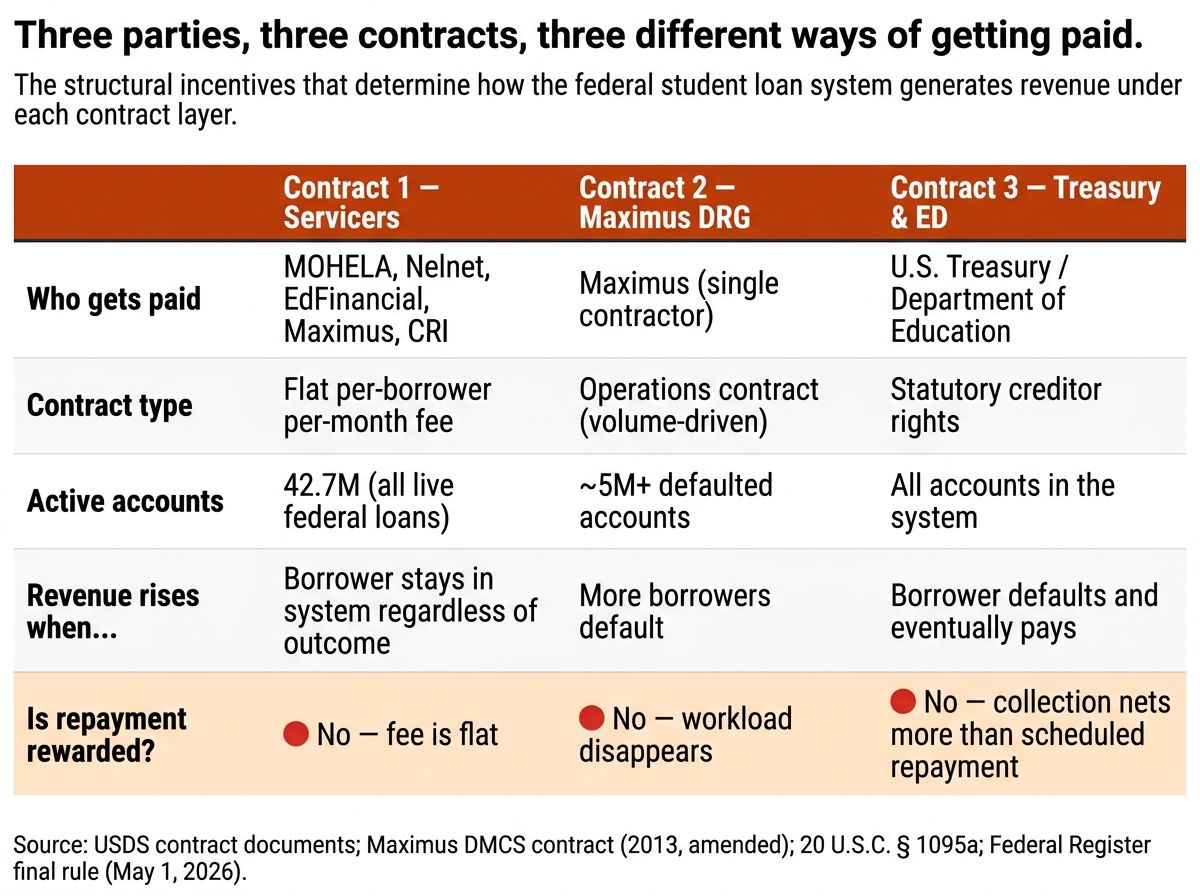

The federal student loan system pays three different parties under three different contract structures. Regular servicers like MOHELA and Nelnet are paid a flat per-borrower fee through the Unified Servicing and Data Solution (USDS) contract — same dollar amount whether the borrower repays smoothly or limps along delinquent. Maximus, the single contractor running the Default Resolution Group, is paid under an operations contract whose workload scales with the number of defaulted accounts. The Department of Education and Treasury, as creditor and enforcer, collect more total dollars over the life of a defaulted loan than over a loan repaid on schedule, through interest capitalization, collection fees, and 15% wage garnishment.

The contrarian point: only the servicer contract is even nominally structured around repayment, and it’s structured to pay the same regardless of borrower outcome. The other two contracts only generate revenue when the system breaks.

What to watch:

The legacy plan lockout: any new loan disbursed on or after July 1, 2026 forces all of a borrower’s loans onto RAP or the new Standard plan

July 1, 2026: Repayment Assistance Plan (RAP) goes live; $10 minimum monthly payment kills the $0 IDR option that protected zero-income borrowers

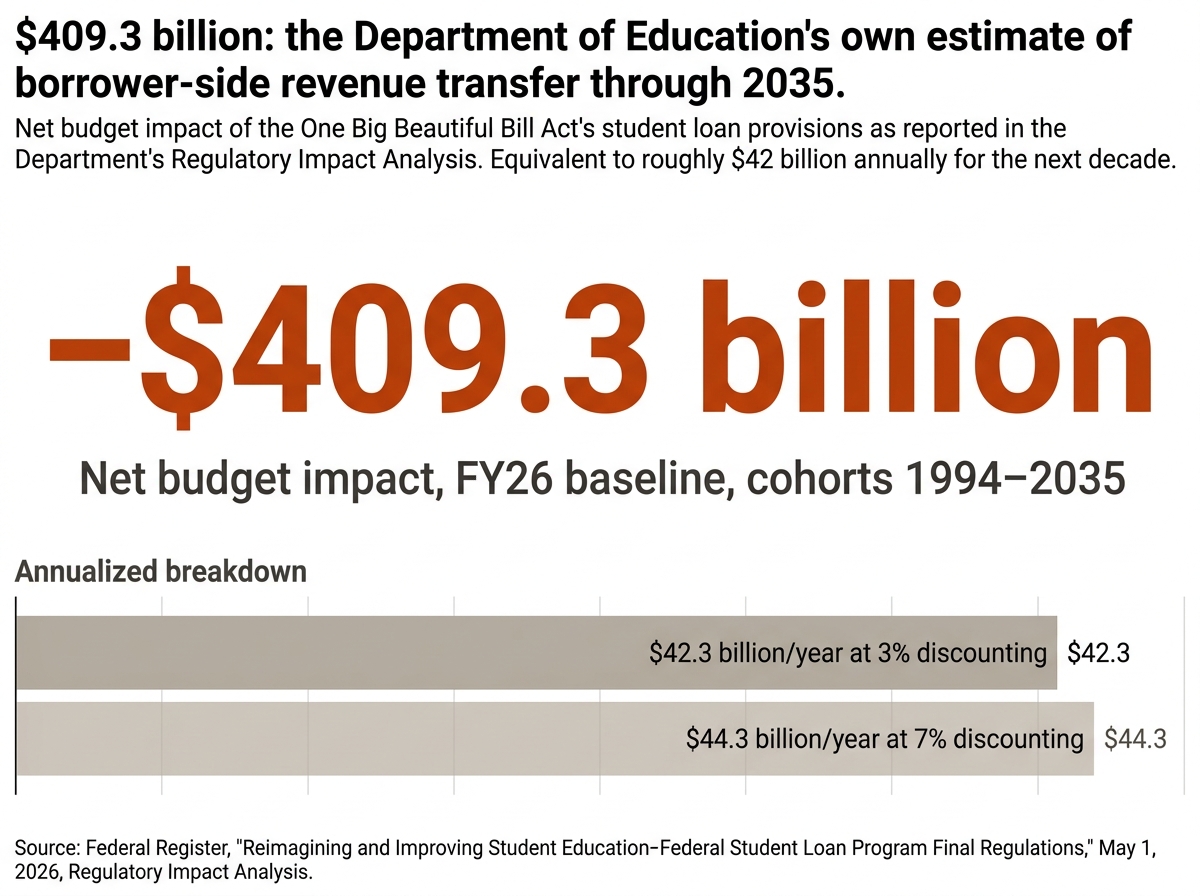

The $409.3 billion in “taxpayer savings” identified in ED’s own Regulatory Impact Analysis is a transfer from borrowers to the federal balance sheet, not an efficiency gain

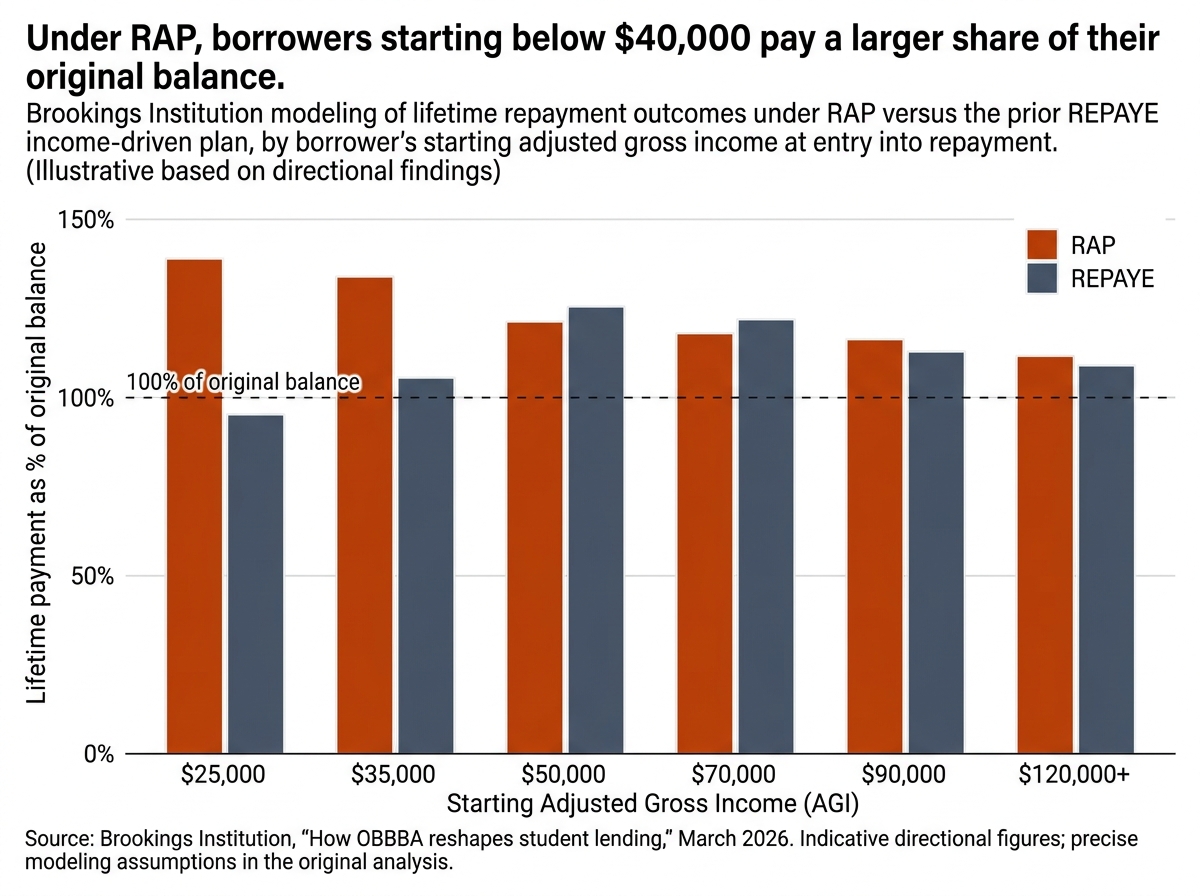

Borrowers earning less than $40,000 AGI repay a larger share of their balance under RAP than under prior plans, per Brookings modeling

The scale of the federal student loan portfolio

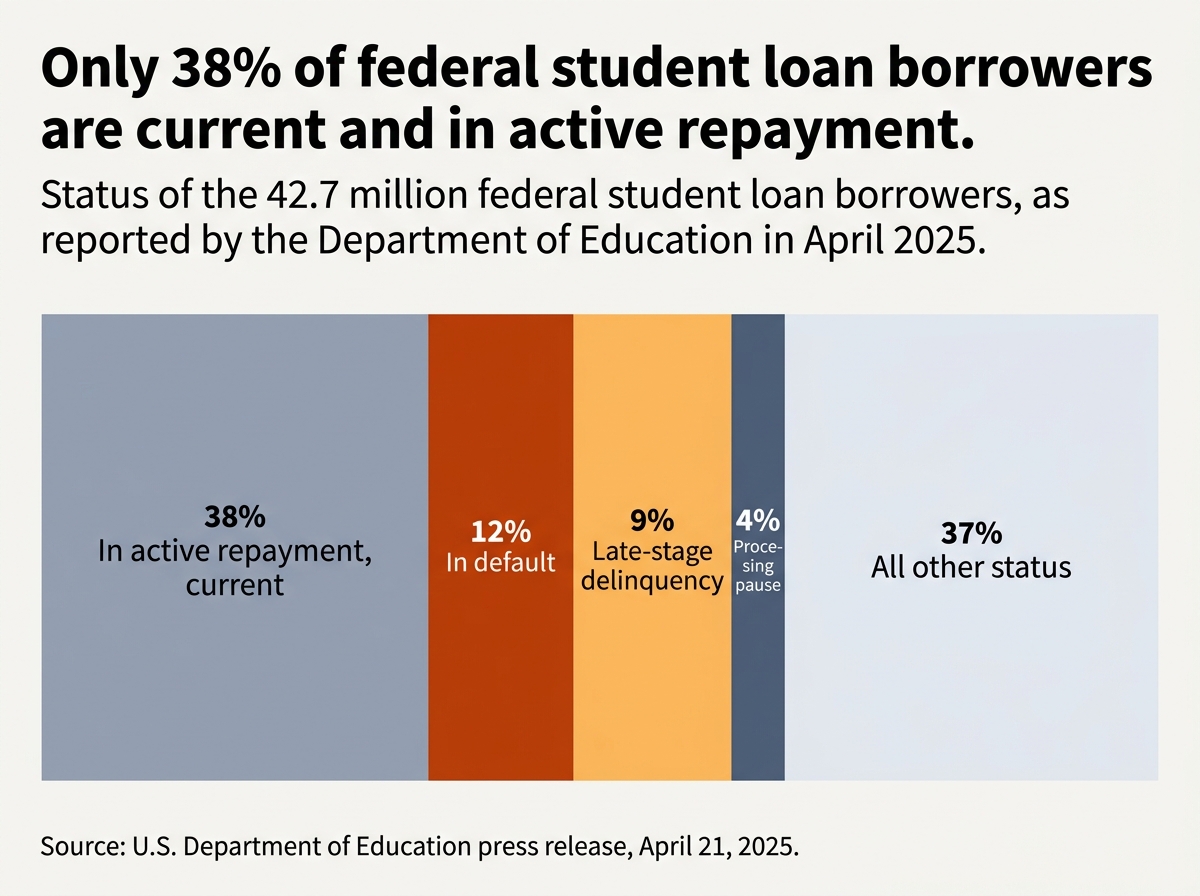

Before the contract analysis, the rough scale of what’s being administered: 42.7 million federal student loan borrowers owe more than $1.6 trillion. That’s the Department of Education’s own figure as of April 2025.

Of those borrowers, by the Department’s count:

- Only 38% are current and in active repayment

- 5 million borrowers are in default (more than 360 days past due) — many for seven years or longer

- 4 million additional borrowers are in late-stage delinquency (91 to 180 days past due)

- 1.9 million borrowers are stuck in a processing pause put in place by the prior administration that prevented enrollment in IDR plans

- The remaining borrowers are in deferment, forbearance, the in-school grace period, or paused under SAVE-plan litigation

If the late-stage delinquency cohort transitions to default, almost 25% of the federal student loan portfolio will be in default within months. That’s the “default cliff” Congressional Research Service flagged in September 2025.

The Trump administration’s framing of this picture is straightforward: borrowers borrowed, borrowers must repay, and the prior administration’s repayment policies were unsustainable. The new framing for collections is enforcement.

What gets less attention is the contract architecture that determines who gets paid for that enforcement.

Contract 1: How regular student loan servicers get paid

The five companies that act as primary federal student loan servicers — MOHELA, Nelnet, EdFinancial, Maximus Federal Services, and Central Research, Inc. (CRI) — are paid under the Unified Servicing and Data Solution (USDS) contract that went live April 1, 2024. The USDS contract replaced the legacy Title IV Additional Servicer (TIVAS) and not-for-profit servicer contracts that had governed the system since 2009 and 2011.

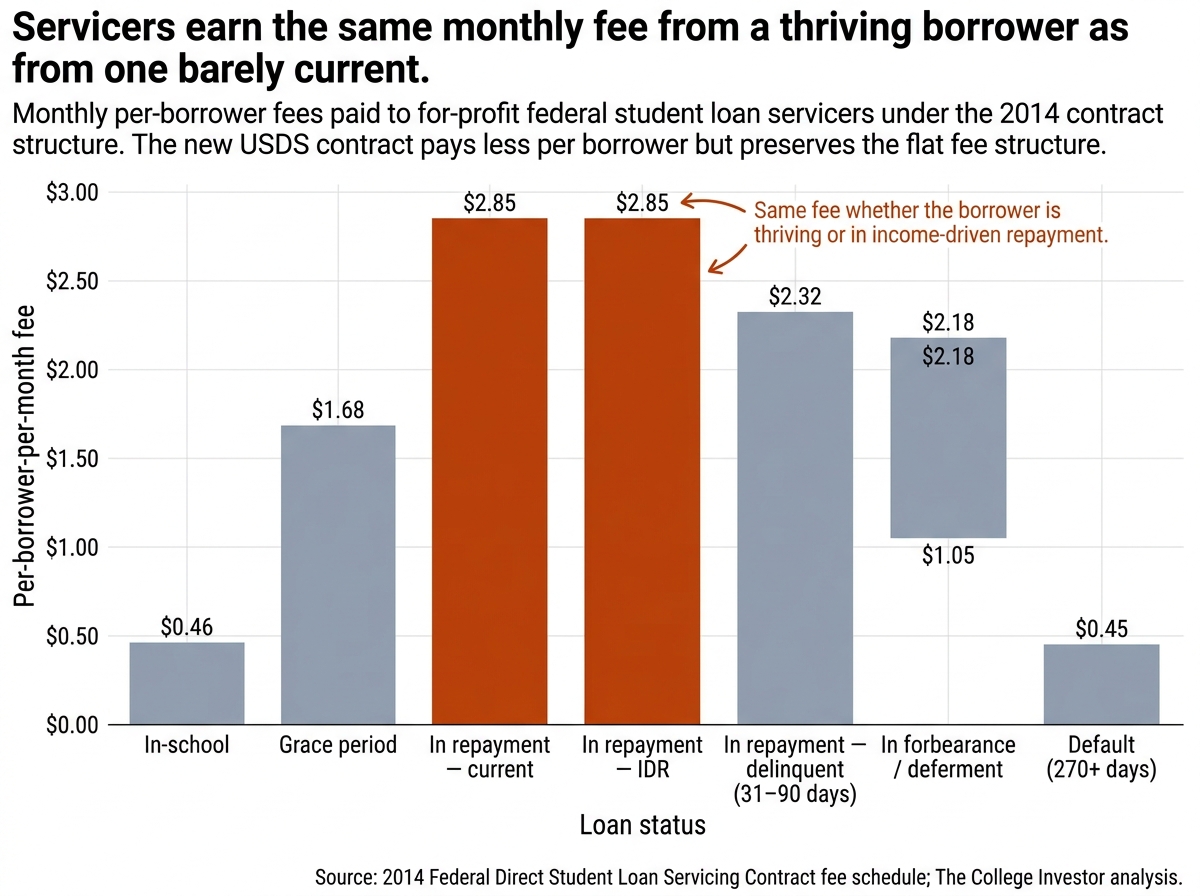

Under the legacy contract structure, the fee was a flat per-borrower-per-month rate that varied by loan status. For a borrower in active repayment, a for-profit servicer received roughly $2.85 a month. For a borrower in the in-school period, the servicer received roughly $0.46 per month, totaling $47.25 over the full pre-repayment period. For a borrower in the six-month grace period after graduation, the servicer received about $1.68 per month, totaling $10.08 across the grace window.

Stacked across a standard 10-year repayment plan, a borrower who stayed current generated about $399 in lifetime servicer revenue under the legacy contract: $47.25 from the in-school period, $10.08 from grace, and $342 from 10 years of in-repayment fees at $2.85 per month.

The USDS contract does not publish its per-borrower rate. Nelnet, the only USDS servicer that’s a publicly traded company, has disclosed on multiple earnings calls — including its 10-K for fiscal year 2024 and again in its Q4 2025 earnings release — that revenue under USDS on a per-borrower blended basis is lower than under the legacy contract. Segment-level math: Nelnet’s Loan Servicing and Systems revenue dropped from $138.0 million in Q4 2024 to $116.6 million in Q4 2025, a 15% decline. Some of that is volume — Nelnet’s Discover acquisition added 400,000 borrowers — but the structural per-borrower compression is the public part.

The crucial detail in this contract is not the absolute number. It’s the flatness. Servicers receive the same fee whether the borrower is thriving or barely current. There is no payment bonus for moving a delinquent borrower back into good standing. There is no payment penalty for letting a borrower drift into default. The contract is structured to compensate operational presence, not borrower outcome.

The USDS contract and the per-borrower revenue squeeze

When the Department of Education designed USDS, the stated goals were centralization, accountability, and customer experience. The Department wanted to move borrower-facing branding and account management away from individual servicer websites toward StudentAid.gov. It wanted to be able to redistribute borrower accounts across multiple servicers as needed. And it wanted the ability to enforce performance standards through financial penalties.

The contract was awarded to five vendors in 2022 and went live April 1, 2024. Four of the five are continuing federal servicers with prior experience. The outlier is CRI — Central Research, Inc. — which had previously worked as a private collection agency on defaulted accounts but had not served current loans before USDS.

The per-borrower compression that Nelnet flagged in its 10-K is the predictable outcome of multi-vendor competitive procurement at federal scale. The Department got more accountability for less money per borrower. The servicers got reduced revenue.

What hasn’t changed is the underlying flatness of the per-borrower fee structure. The Department of Education didn’t restructure servicer compensation toward outcomes. It restructured it toward lower unit cost.

When servicer accuracy stopped being measured

The accountability that was supposed to come with USDS — the part that would have justified the per-borrower fee compression — has not materialized.

According to a March 2026 Government Accountability Office report (GAO-26-108534), the Department of Education’s Office of Federal Student Aid set performance standards for USDS servicers on six metrics, including the accuracy of borrower records and the quality of borrower phone calls. Financial penalties applied when servicers missed standards.

Four of the five servicers missed the accuracy standard in 2024 and incurred penalties.

In February 2025, FSA stopped assessing servicers on accuracy and call quality entirely. Agency officials cited a reduction in staff capacity. As of December 2025, no replacement assessment method was in place. The Department’s own response to the GAO recommendation to resume the assessments was to disagree.

The GAO’s framing of the consequence was unsparing: “Without [these assessments], the office can’t be sure that borrower records are correct and servicers are giving borrowers quality information.” Inaccurate records can result in borrowers being billed for incorrect amounts or placed in the wrong repayment status. Borrowers who call for help may be given wrong information.

The contract that was meant to reward keeping borrowers current pays the same regardless of outcome. The performance penalties that were supposed to catch failure stopped being measured fourteen months ago.

Contract 2: Maximus and the Default Resolution Group

When a borrower hits 360 days delinquent, the loan transfers from the servicer to a different system entirely. The Default Resolution Group — operationally, the Default Management and Collections System (DMCS) — is the federal government’s collection arm for defaulted education debt. The DMCS is operated under contract by Maximus Federal Services, a subsidiary of Maximus, Inc.

The Maximus DMCS contract was originally signed September 30, 2013, valued at $143.3 million for a base period of two years and three months, with eight one-year options. Total contract value over its full option-renewal life: approximately $848.4 million. The contract has been renewed and extended through subsequent periods; Maximus is currently the single contractor managing the DMCS.

Maximus did not always own this work alone. For decades, the Department of Education contracted with a network of private collection agencies (PCAs) — at peak, 11 simultaneous contracts — that collected on defaulted accounts under a percentage-of-recovery commission model. PCAs received commission on each dollar they collected from borrowers, plus per-account fees for processing rehabilitation agreements and consolidations.

In December 2021, the Department of Education terminated all 11 PCA contracts and recalled approximately 5.1 million borrower accounts. The work transitioned to Maximus under the existing DMCS infrastructure. The official rationale was efficiency and improved borrower experience.

Maximus’s DMCS contract is structured as an operations contract, not commission-based. The company is paid for running the system: call centers, correspondence processing, financial transaction handling, and credit-bureau reporting. The contract’s value is tied to operational volume, which is tied directly to the number of defaulted accounts in the system. The more borrowers default, the more accounts Maximus processes.

This is a different incentive than the PCA model — but it is not an incentive aligned with reducing defaults. It is an incentive aligned with handling defaults efficiently. A world with zero defaults would have a contract with nothing to do.

For context on what the PCA model produced when commission-based incentives ran free: in December 2024, the Consumer Financial Protection Bureau banned Performant Recovery, one of the terminated PCAs, from servicing or collecting on any student loan debt. The CFPB found that between 2015 and 2020, Performant deliberately delayed borrowers’ loan rehabilitation processing past the 65-day window during which rehabilitation fees were waived. The delay caused borrowers to incur collection costs equivalent to 16% of their loan balances plus additional interest. Performant’s revenue increased because of the delays.

The Maximus operations contract eliminates that specific pathology. It does not eliminate the broader truth that the entire Contract 2 layer of the federal student loan system only exists because defaults exist.

Contract 3: How the Treasury collects on default

The Department of Education and the U.S. Treasury are not contractors. They are the federal government — the creditor on every Direct Loan and the enforcement authority for every defaulted account. Their “contract” is statutory rather than negotiated, and the Higher Education Act and the Debt Collection Improvement Act of 1996 set its terms.

The terms are unilateral by design. When a borrower defaults, the entire balance of principal and interest is accelerated — the full unpaid amount becomes immediately due. Unpaid interest capitalizes onto principal, increasing the base on which future interest accrues. The Department reports the default to all four major consumer credit reporting agencies (Equifax, Experian, Innovis, TransUnion), where it remains visible for seven years.

Then the involuntary collection mechanisms activate.

Administrative wage garnishment. Under the Debt Collection Improvement Act of 1996, the Department of Education can order a non-federal employer to withhold up to 15% of a borrower’s disposable income to repay defaulted student loans. No court order is required. The borrower receives a 30-day notice and a right to a hearing. Garnishment continues until the default is resolved through rehabilitation, consolidation, or full repayment.

Administrative wage garnishment was paused during the COVID-19 pandemic. It formally restarted in the week of January 7, 2026, with the first 1,000 notices. The Department has stated that garnishment notices will scale up monthly throughout 2026.

Treasury Offset Program. Under the Debt Collection Improvement Act, the Treasury can seize federal payments owed to defaulted borrowers, including federal tax refunds, Social Security retirement and disability benefits, and certain federal salaries. Tax refund offset is unlimited in amount. Social Security offset is capped at 15% of benefits, leaving a minimum of $750 per month protected for the borrower.

Treasury Offset Program seizures resumed on May 5, 2025, after a five-year pandemic pause.

Collection charges. Historically, the Department added collection charges to defaulted balances at a rate of up to 24.34% of outstanding principal and interest at the time of default, or 19.58% of every payment before the payment touched principal or interest. These rates are set by federal regulation and are intended to recover the actual cost of debt collection. Collection charges were waived during the COVID-19 pandemic and through the Fresh Start initiative; as of May 2026, charges remain paused for borrowers who entered default during the pause window. The statutory authority for them remains intact.

The structural point about Contract 3 is this: the federal government collects more total dollars over the life of a defaulted loan than it collects over the life of a loan repaid on schedule. The collection mechanisms — capitalized interest on a larger base, collection charges, garnishment, offset — are by design more lucrative than scheduled repayment. There is no statute of limitations on federal student debt. A defaulted loan from 1995 is still collectible in 2026 against a borrower’s Social Security benefits.

What the One Big Beautiful Bill Act locks in on July 1, 2026

The One Big Beautiful Bill Act (formally renamed in the Department’s final rule as the Working Families Tax Cuts Act) was signed July 4, 2025. The Department published its final implementing regulations on May 1, 2026 in the Federal Register.

Most provisions take effect July 1, 2026. Some take effect July 1, 2027 (rehabilitation, deferment, forbearance). The legacy IDR plans sunset by July 1, 2028.

For new borrowers — anyone whose first federal student loan is disbursed on or after July 1, 2026 — the entire IDR menu collapses to one plan. The choices are the new Repayment Assistance Plan (RAP) and a new tiered Standard Repayment Plan with 10/15/20/25-year fixed terms based on balance.

For existing borrowers, the legacy IDR plans (SAVE, PAYE, Income-Contingent Repayment) all sunset on July 1, 2028. Income-Based Repayment (IBR) survives indefinitely. Borrowers in SAVE administrative forbearance — currently several million — will be defaulted into RAP if they do not select an alternative by July 2028.

Parent PLUS loans originated after July 1, 2026 are ineligible for RAP at all. The only repayment option for new Parent PLUS borrowers is the new Standard plan.

The Department’s own Regulatory Impact Analysis estimates the rule’s net budget impact at −$409.3 billion for cohorts 1994 through 2035. That’s $42.3 billion a year in reduced transfers from the federal balance sheet, across loans originated over a 40-year window.

The Department frames this number as $409 billion in taxpayer savings, plus an additional $224 billion in reduced loan volume from the new borrowing caps on Graduate PLUS and Parent PLUS loans.

Why low-income borrowers pay more under RAP

RAP’s payment formula on paper looks gentle. Monthly payments are scaled from 1% of adjusted gross income at the low end to 10% of AGI at the high end, in $10,000 income brackets. Each dependent reduces the payment by $50. Unpaid interest is waived if the borrower makes their on-time payment. A $50 principal subsidy ensures the loan balance declines each month even if the borrower’s payment doesn’t cover interest.

The mechanics are an improvement over SAVE in two specific ways: balance growth is structurally prevented through the interest-waiver mechanism, and the $50 principal subsidy guarantees ongoing principal reduction.

The mechanics are a regression in three specific ways.

There is no $0 payment. Under prior IDR plans — SAVE, PAYE, REPAYE — a borrower with income below approximately 225% of the federal poverty level paid zero per month. Under RAP, every borrower pays at least $10 per month regardless of income. About seven in ten borrowers in income-driven plans have qualified for a $0 bill at some point in their repayment history. Under RAP, that safety valve disappears.

The repayment period is longer. Existing IDR plans forgive after 20 years (for undergraduate-only borrowers) or 25 years (for borrowers with graduate debt). RAP forgives after 30 years — a flat additional 5 to 10 years of payments.

Forgiveness is now federally taxable. The American Rescue Plan Act of 2021 temporarily excluded forgiven student loan balances from federal income tax. The exclusion expired December 31, 2025. Any IDR forgiveness discharged on or after January 1, 2026 is reportable as ordinary income for federal tax purposes, potentially producing a substantial tax bill in the year of forgiveness. Public Service Loan Forgiveness remains tax-free; PSLF was not changed by OBBBA. RAP payments do count toward PSLF.

The Brookings Institution’s March 2026 lifetime-repayment modeling captured the aggregate impact. Brookings found that “borrowers starting with annual incomes below about $40,000 repay a larger share of their original balances because they no longer qualify for $0 payments and must remain in repayment for up to 30 years rather than 20 or 25.” For these borrowers, total lifetime payments will be notably higher under RAP than under REPAYE, even after accounting for RAP’s interest and principal subsidies.

For middle-income borrowers ($40,000–$70,000), Brookings found RAP payments will be roughly comparable to REPAYE, with most fully repaying within 13–15 years. For high-income borrowers ($80,000+), RAP payments will be modestly higher because the 10% rate applies to full income rather than discretionary income above a threshold.

The distribution of RAP’s net effect is regressive: it produces the largest relative payment increases on the lowest-income borrowers.

The $409 billion that’s being called “savings.”

The Department of Education’s framing of the $409.3 billion figure is that it represents taxpayer savings. The Department’s press release from May 1, 2026 explicitly uses the word “saves” in the headline.

The Regulatory Impact Analysis is more precise. The figure is a net budget impact — a reduction in federal outlays — computed against the FY2026 President’s Budget baseline across loan cohorts 1994 through 2035.

The reduction comes from two main mechanisms. First, less forgiveness is paid out: longer repayment periods, smaller forgivable balances, and taxable forgiveness all reduce the federal cost of the IDR-forgiveness pathway. Second, more is collected: defaulted borrowers cycling through Maximus DRG and Treasury offset, plus higher monthly payments for low-income borrowers under RAP, increase the recovery rate on outstanding balances.

In one sense, “taxpayer savings” is accurate. Taxpayers in aggregate are net better off if the federal student loan portfolio recovers more dollars and writes off fewer dollars.

In another sense, “savings” is misleading framing for what is structurally a transfer from one set of Americans to another. The borrowers who would have qualified for $0 payments under SAVE will now pay $10 a month or more under RAP. Borrowers who would have seen forgiveness at 20 or 25 years will now see it at 30, if at all. Borrowers who default will face capitalized interest, restored collection charges, wage garnishment, and Treasury offset — collection mechanisms that the prior administration had largely paused.

Forty-two percent of the U.S. borrowing population is paying $42 billion a year more so that the federal balance sheet shows $42 billion a year less in outlays. That is not “savings” in the sense of reduced waste. It is reallocation.

The legacy plan lockout – and why one new loan triggers it for all your loans

Buried in OBBBA’s transition provisions is a feature that has received less attention than it deserves: the legacy plan lockout.

Existing borrowers who took out their last federal student loan before July 1, 2026 retain access to the legacy IDR plans (Standard, Graduated, Extended, IBR) and can opt into RAP voluntarily. They can switch among the surviving legacy IBR plan and RAP through July 1, 2028. After July 2028, anyone still in SAVE, PAYE, or ICR is automatically migrated to RAP or IBR.

But any borrower who takes out a single new federal student loan on or after July 1, 2026 loses access to the legacy plans across their entire portfolio. All of their existing loans plus the new loan must be repaid under either RAP or the new Standard plan. The legacy plans cannot be partially retained.

This is the structural trap. A graduate student finishing their last semester of a degree in fall 2026 — taking out one final $10,000 Direct Loan to finish — converts every legacy loan they hold into a RAP loan. Parent PLUS borrowers who take out one more Parent PLUS loan to cover their younger child’s freshman year lose IDR access on every Parent PLUS they’ve ever taken.

There is no clawback or unwinding. The lockout is one-directional.

For borrowers strategizing around this provision: completing federal borrowing before July 1, 2026 preserves legacy plan access. Switching to private loans for any post-July financing preserves legacy plan access on federal loans. Both options have costs.

The risks to the three-contracts thesis

Three honest challenges to the analysis above:

The servicer contract isn’t structurally hostile to borrowers — it’s structurally indifferent. A flat per-borrower fee doesn’t pay servicers more when borrowers fail; it just doesn’t pay them more when borrowers thrive. Indifference is not the same as adversarial incentive. The case for servicers is that flat fees produce predictable operational costs and avoid the worst pathologies of commission-based compensation. The historical record on commission-based compensation in student loan collection — the Performant Recovery story — supports that case.

The PCA-to-Maximus transition was a borrower-protective decision. The Department of Education terminated the 11 PCA contracts in December 2021 because the percentage-of-recovery commission model produced rampant abuse and customer-service failures. Maximus’s operations contract is genuinely less predatory than the PCA model. The argument that “Maximus only exists because defaults exist” is true but does not mean Maximus has an active incentive to cause defaults — just to manage them when they occur.

RAP’s interest-waiver and principal-subsidy mechanics are genuine improvements over prior plans. Under SAVE and earlier IDR plans, low-income borrowers’ balances often grew despite making on-time payments — a phenomenon called negative amortization that left borrowers psychologically demoralized and financially stuck. RAP prevents balance growth structurally. For borrowers committed to repayment but facing temporary income shocks, RAP is more forgiving than its predecessors in some specific situations. The Brookings finding that <$40K AGI borrowers pay more under RAP is a population-level conclusion that does not apply to every individual circumstance.

The aggregate point of the article stands: the three contracts don’t reward repayment in a structurally meaningful way, and the July 2026 changes don’t fix that. The individual points above are real qualifications.

What to watch in 2026 and 2027

Five specific signals will indicate how the post-OBBBA system performs in practice:

- Whether FSA resumes servicer accuracy and call-quality assessments. The GAO recommended resumption; the Department disagreed. If the assessments do not resume by end of 2026, the USDS accountability layer is effectively eliminated.

- The trajectory of the default population. Department of Education data showed 5 million in default and 4 million in late-stage delinquency as of April 2025. The number to watch is whether late-stage delinquency converts to default or recovers to current. If the conversion rate is high, the Maximus DRG caseload will spike and stress single-contractor capacity that CRS has already flagged as a concern.

- The trajectory of wage garnishment. The first 1,000 garnishment notices went out the week of January 7, 2026. The Department stated notices will scale monthly through 2026. Total annual garnishment volume by Q4 2026 will indicate whether the Department is throttling enforcement politically or pursuing it at full statutory authority.

- Whether collection charges are reinstated. The 24.34% / 19.58% collection charges remain authorized in statute but waived in current practice. Reinstatement would substantially increase the recovery the Treasury extracts from defaulted borrowers.

- How many borrowers trigger the legacy plan lockout. Anyone who takes out a federal student loan after July 1, 2026 with prior federal loans outstanding will lose legacy IDR access. The number of borrowers affected — and whether the Department clarifies any reversal mechanism — will materially shape RAP enrollment numbers.

The student loan system isn’t broken. It’s working exactly as the contracts are written — and only one of those contracts pays more when you succeed.

FAQ

Do student loan servicers actually make money when borrowers default?

No, when a borrower defaults, the loan transfers from the servicer to the Default Resolution Group (Maximus), and the servicer stops being paid for that account. Servicers do not directly profit from default. The servicer fee structure is flat per borrower regardless of borrower outcome, which means servicers earn the same revenue from a thriving borrower as from a barely-current one, that is the actual incentive asymmetry, not direct profit on default.

How much does Maximus get paid to run the Default Resolution Group?

Maximus’s original DMCS contract was signed in 2013, valued at $143.3 million for the base period and approximately $848.4 million if all eight one-year option periods are exercised. Maximus has subsequently been the single contractor managing the system; current contract values are not publicly disclosed at the same granularity. The contract is structured as an operations contract, not a commission on recovery.

When does the Repayment Assistance Plan start?

RAP becomes available on July 1, 2026. For borrowers whose first federal student loan is disbursed on or after July 1, 2026, RAP and the new tiered Standard Repayment Plan are the only options. Existing borrowers can voluntarily enroll in RAP on July 1, 2026 or remain in legacy IDR plans until July 1, 2028.

What’s the minimum monthly payment under RAP?

$10 per month. Every borrower pays at least $10 regardless of income or family size. Under prior IDR plans, borrowers with very low income could qualify for $0 monthly payments. That $0 option is eliminated under RAP.

Is student loan forgiveness still tax-free?

Public Service Loan Forgiveness (PSLF) remains federally tax-free. IDR forgiveness — including RAP forgiveness at the 30-year mark — is federally taxable as ordinary income for any forgiveness discharged on or after January 1, 2026. The American Rescue Plan Act’s temporary tax exclusion expired December 31, 2025. State tax treatment varies by state.

Will my wages be garnished if I’m in default?

Wage garnishment for defaulted federal student loans formally restarted the week of January 7, 2026 after a five-year pandemic pause. The Department of Education can order non-federal employers to withhold up to 15% of disposable income without a court order. Borrowers receive a 30-day notice before garnishment begins. Garnishment stops when the default is resolved through rehabilitation, consolidation, or full repayment.

What happens if I take out a new student loan after July 1, 2026?

If you have existing federal student loans and take out a new federal loan disbursed on or after July 1, 2026, you lose access to all legacy IDR plans on every loan in your portfolio. All your loans must be repaid under either RAP or the new Standard plan. This is the “legacy plan lockout” provision of OBBBA.

This analysis is based on the Department of Education’s Regulatory Impact Analysis published in the Federal Register on May 1, 2026; Nelnet’s Q4 2024 and Q4 2025 earnings releases; the Government Accountability Office’s March 2026 report on FSA servicer oversight; the Consumer Financial Protection Bureau’s December 2024 enforcement action against Performant Recovery; the Brookings Institution’s March 2026 analysis of OBBBA’s repayment provisions; Congressional Research Service products on RAP and default trends; and U.S. Department of Education press releases and Dear Colleague Letters from 2024 through May 2026.

— Hamza