The auto-parts bankruptcy that wiped out billions wasn’t really a fraud story. It was a story about how a $3 trillion private debt market grew up without a 10-K.

Skip to the section that interests you most

The 60-second version

First Brands Group, a Cleveland-based auto-parts roll-up doing $5 billion a year in sales, filed for Chapter 11 in September 2025. By January 2026, founder Patrick James and his brother Edward had been indicted on nine federal felony counts including a “continuing financial crimes enterprise” charge. At the time of the filing, the company had $12 million in cash and over $9 billion in liabilities. Lenders are looking at billions in losses, and a federal indictment alleges hundreds of millions flowed personally to Patrick James between 2018 and 2025.

The fraud is the headline. The disclosure failure that let the fraud scale to $11 billion is the actual story.

First Brands ran four parallel debt programs — on-balance-sheet term loans, receivables factoring, off-balance-sheet inventory finance through founder-controlled SPVs, and supply-chain finance — each rated by different agencies, each disclosed to different lenders, none of them required to be cross-referenced. The factoring lenders didn’t know about the SPV inventory finance. The term-loan lenders were told there was “no off-balance sheet financing” while $2 billion of it already existed. The whole structure was rated investment-grade or near it across multiple tiers by a private letter ratings market increasingly dominated by smaller agencies with looser methodologies than Moody’s, S&P, and Fitch.

Contrarian point: This isn’t a Patrick James story. It’s a story about what disclosure looks like in a $3 trillion private credit market that has no equivalent of the 10-K, no SEC reviewer comparing year-over-year footnotes, and no rule against the same pile of inventory being pledged to three different lenders.

What to watch: NAIC capital treatment of privately rated insurance assets, SEC threshold disclosure rules for private debt, and which tier-2 rating agencies start losing institutional mandates.

Who is First Brands Group?

First Brands Group is — was — a Cleveland-based aftermarket auto parts company assembled through debt-financed acquisitions over roughly a decade. Patrick James founded what was then called Crowne Group in 2013. The Crowne name was retired around 2020 and became First Brands. By the bankruptcy filing in September 2025, the company employed roughly 26,000 people across more than 100 entities globally, with around 17,000 of those employees in North America.

The portfolio is the kind of brand list anyone who has changed a wiper blade has seen in an AutoZone aisle. FRAM filters. Autolite spark plugs. Anco wipers. Raybestos brakes. Champion. Cardone. Brake Parts. The strategy was straightforward and not unusual in private equity: buy small to mid-sized aftermarket brands, integrate the operations, fund the next acquisition with new debt. Roll-ups in this category have been one of the most common LBO templates of the last fifteen years.

The numbers were big enough to be a credible borrower in the broadly syndicated loan market. The company reported approximately $5 billion in net annual sales in 2024 and roughly $1.1 billion of EBITDA — leverage of more than 5x on the on-balance-sheet debt of $6.1 billion. Aggressive but not unusual for this corner of the credit market.

What was unusual, only in retrospect, was the structure underneath the headline numbers.

The September 2025 collapse

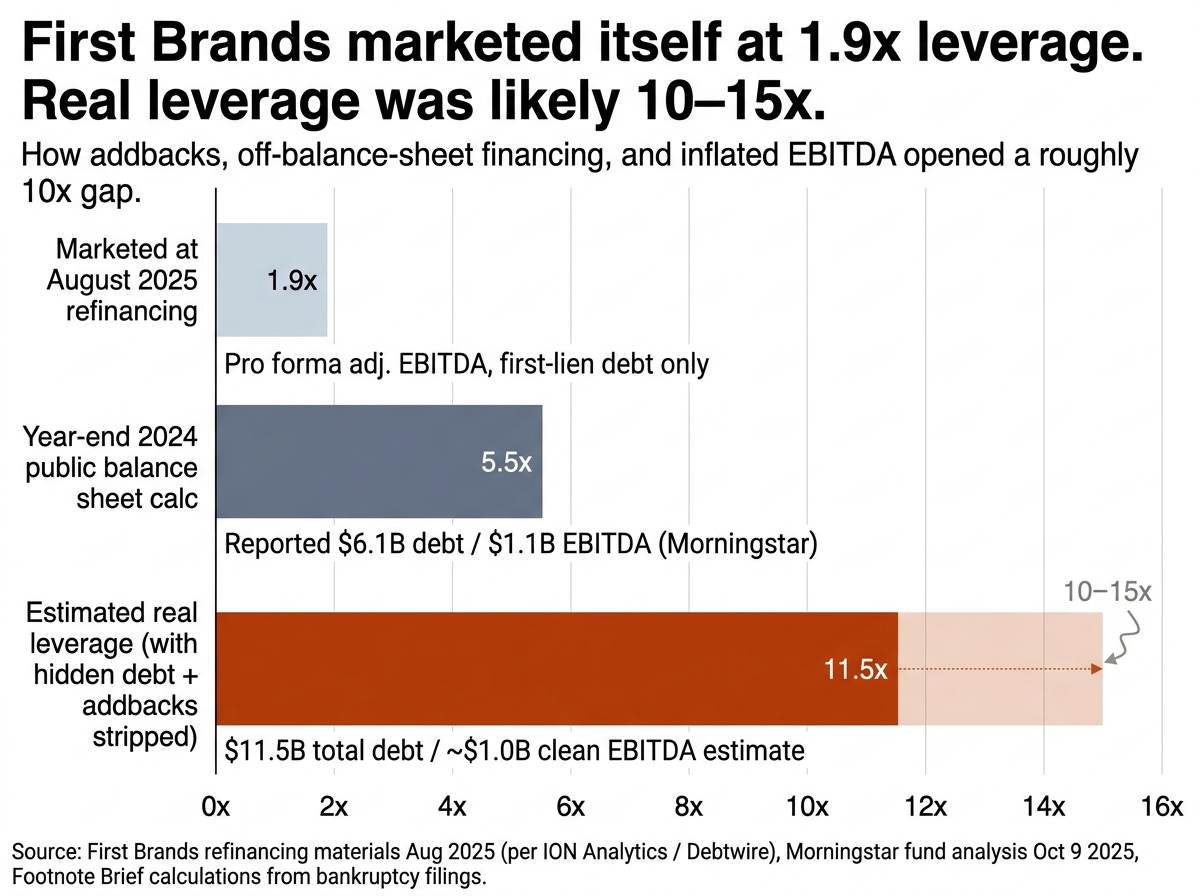

The unraveling started visibly in summer 2025, when First Brands tried to refinance approximately $6 billion of its capital structure. The company marketed the deal at 1.9x net first-lien leverage on $1.9 billion of LTM pro forma adjusted EBITDA. Even by the standards of leveraged finance, where addbacks are normal, the gap between the refinancing pitch (1.9x) and Morningstar’s calculation off the public balance sheet (>5x) was wide. A buy-side source quoted by ION Analytics estimated as much as 60% of the marketed EBITDA was addbacks tied to acquisitions.

The refinancing didn’t close. By early September, term loan prices were holding around 90 cents on the dollar. On September 12, the Financial Times reported that Apollo had taken a position betting against First Brands credit months earlier. Term loans started moving lower, fast. Within two weeks, the company and its top creditors had hired restructuring advisors. A senior steering-committee creditor exited via a so-called big-boy letter alerting buyers that the seller held material non-public information. Term loan quotes plunged from the high 90s into the high 30s.

First Brands filed for Chapter 11 protection in the U.S. Bankruptcy Court for the Southern District of Texas in late September 2025. Charles Moore of Alvarez & Marsal was named Chief Restructuring Officer in September and elevated to interim Chief Executive in October after Patrick James resigned. Edward James left as Senior Vice President shortly after. The company’s former CFO, Stephen Graham, resigned at the end of October.

The bankruptcy petition listed liabilities in the $10 billion to $50 billion range against assets of $1 billion to $10 billion. The Department of Justice’s later indictment specified roughly $9 billion in liabilities against just $12 million in corporate cash.

Then the forensic accountants from Alvarez & Marsal started filing affidavits in bankruptcy court — and the story that had looked like a debt-fueled roll-up gone wrong started to look like something else entirely.

The $179.84 invoice

In a court filing on November 3, 2025, Charles Moore detailed what he and the company’s restructuring advisors had found after weeks of forensic work. The most cited example, which would later be reproduced in court coverage from Bloomberg, Fortune, and the ABF Journal, was a single sales invoice from May 9, 2024.

The original invoice was for $179.84 — a small bill for a small package of brake parts. The version sold by First Brands to a financing counterparty showed $9,271.25. The same invoice. Fifty times the original amount.

That altered invoice was packaged with thousands of others and sold to Katsumi Global, a financing joint venture between Norinchukin Bank of Japan and Mitsui & Co. According to the Moore declaration, other invoices in the same package were inflated by twelve or fifteen thousand dollars apiece. Across the package, Katsumi paid roughly $11 million for invoices that were actually worth about $2.3 million.

The pattern was systematic, not isolated. The federal indictment unsealed January 29, 2026 detailed another example: in June 2025, First Brands invoiced a customer for $8,976.24. The same invoice was sold to one factor at $17,826.26 and three days later sold again to a different factor at $463,734.92. Same parts. Same customer. Three different inflated values, two different factors, no one knowing about the other.

By the bankruptcy filing, factoring counterparties were collectively sitting on $2.7 billion of fake or duplicated First Brands receivables. The DOJ later described the operation as a Ponzi scheme — proceeds from new fake invoices being used to pay obligations on older fake invoices.

The four layers of debt

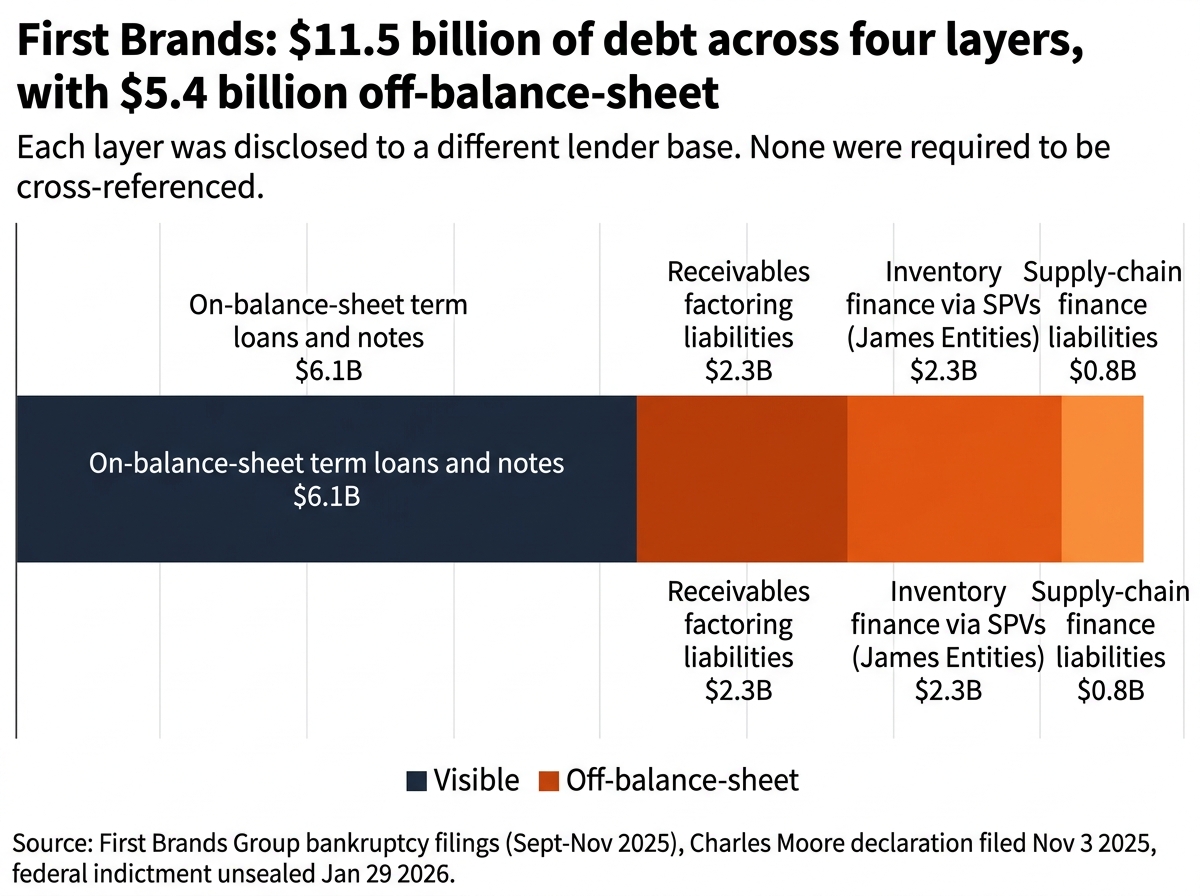

To understand why the fraud could scale to billions before any single lender noticed, you have to understand that First Brands was running four debt programs in parallel, each with a different lender base and a different disclosure regime.

The on-balance-sheet stack — roughly $6.1 billion at filing — was the visible part. Term loans, second lien, senior notes. This is the corner of the capital structure that gets a Fitch or Moody’s rating, that trades in the broadly syndicated loan market, and that ends up sitting in collateralized loan obligations.

The factoring program — $2.3 billion of liabilities at filing — was treated as off-balance-sheet under accounting rules. When a company sells a receivable to a factor and the transaction qualifies for “derecognition” under IFRS or US GAAP, the receivable disappears from the balance sheet entirely. The cash is recorded as an operating inflow. The implied liability — the obligation to pass through customer payments to the factor when they arrive — sits on the financing counterparty’s balance sheet, not the seller’s. This is normal, legal, and widely used. It is also, by design, invisible if you only look at the seller’s reported leverage.

The third layer — another $2.3 billion of off-balance-sheet financing — was the one that would later become the criminal core of the indictment. Patrick James personally controlled a set of holding companies that the indictment refers to as “the James Entities.” Three lenders advanced money to these entities. The James Entities used the cash to buy inventory from First Brands. They then sold or leased that inventory to First Brands’ off-balance-sheet inventory finance providers, with the cash routing back to First Brands itself. Functionally, First Brands was borrowing against inventory that was already pledged to its term-loan lenders, but the structure ran the borrowing through entities that — on paper — had no relationship to First Brands. When term-loan lenders sent diligence requests asking about off-balance-sheet financing, they were told there wasn’t any.

The fourth layer was supply-chain finance — roughly $800 million in unsecured liabilities to suppliers and the financing institutions that paid those suppliers on First Brands’ behalf. SCF programs are a normal feature of corporate finance and are usually disclosed as trade payables. They become opaque debt when the volume gets large enough relative to operating cash flow that they functionally substitute for revolving credit.

Add the four layers together and you get approximately $11.4 billion of debt. Apply that against EBITDA stripped of the addbacks — call it $1.4 billion based on Q2 2025 actuals annualized, or possibly significantly less once forensic accountants finish restating revenue net of the round-trip transactions — and First Brands’ real leverage was somewhere between 10 and 15 times. Possibly higher. The 1.9x marketed in August 2025 was a fiction supported by selective disclosure. The 5x calculated by Morningstar from the public balance sheet was a fiction supported by accounting rules that derecognize debt that economically still exists.

Bowery Finance II

Inside the second-layer structure was an account called Bowery Finance II.

According to the November 3, 2025 affidavit from Charles Moore, Bowery Finance II was a “slush fund” controlled by Patrick James. From 2022 through 2025, approximately $12 billion flowed through the account, including transfers between Patrick James personally, the Patrick James Trust, his affiliated business entities, and First Brands’ operating units. Some of the flows looked like money laundering through a corporate vehicle: cash arriving from off-balance-sheet financing facilities and being routed out to entities including a luxury aviation company (Pegasus Aviation), a real estate holding company (Albion Realty), and the Patrick James Trust itself.

The civil complaint filed by the bankruptcy estate identified more than $700 million transferred to Patrick James and entities he controlled between 2018 and 2025, with the majority occurring between 2023 and 2025. The named beneficiaries of those transfers — per the same complaint — included over $3 million in rent for a New York City townhouse, $8 million to a wellness company owned by James’s son-in-law, $2 million to a family office, $500,000 to a personal chef, and $150,000 to a “celebrity” personal trainer. James’s personal assets included seven homes (in Malibu and the Hamptons among them) and at least seventeen exotic cars.

The criminal indictment that followed in January referenced what First Brands employees internally called “round trips” or, euphemistically, “corporate initiatives” — transactions where financers wired money to a third-party bill processing company that the lenders thought was paying First Brands’ suppliers, but was actually routing the money back to First Brands itself.

The civil action seeks to claw back those funds. Patrick James, through his attorneys, has denied wrongdoing and characterized the bankruptcy estate’s allegations as “baseless and speculative.” He has separately blamed off-balance-sheet financing partners for what his lawyers have called “predatory” practices. The criminal case will be tried in Manhattan federal court.

How off-balance-sheet financing disappears

Here is where the structural answer lives. Receivables factoring and supply-chain finance, used as designed, are accounting-legitimate ways to move working-capital obligations off a company’s balance sheet. Under IFRS and US GAAP, a receivable can be derecognized — removed from the balance sheet entirely — if certain conditions are met around the transfer of risks and rewards.

This isn’t a loophole. It’s the entire point. The financing institution buying the receivable is taking the credit risk; treating the receivable as the seller’s asset would double-count it. The accounting rule reflects economic reality.

The problem is that “off-balance-sheet” doesn’t mean “doesn’t exist.” It means “not visible on this particular financial statement.” A company with $1 billion of receivables factoring is, in economic substance, a company with $1 billion more leverage than its balance sheet shows. If the factoring program covers a substantial portion of revenue, the company’s free cash flow is structurally dependent on continuously rolling new receivables into the program. If the program freezes — for any reason, including lender concerns about credit quality — the company faces an immediate working capital crisis that looks nothing like its reported leverage suggests.

For public companies, US GAAP and IFRS require footnote disclosure of factoring programs above certain thresholds, and SEC review of those footnotes provides a baseline of transparency. The disclosure isn’t always great, but a sophisticated reader can usually find the program and size it.

For private companies — and First Brands was private, owned 100% by Patrick James — there is no equivalent forcing function. A private company’s financial statements go to its lenders under the terms of its credit agreements. Each set of lenders gets the disclosure that their particular credit agreement requires. There is no central reviewer comparing what was disclosed to one set of lenders against what was disclosed to another. There is no SEC enforcement risk for selective disclosure.

When First Brands’ senior executives told term-loan lenders in July 2025 that there was “no off-balance sheet financing” while $2 billion of it already existed — and while operating accounts were routing cash through Bowery Finance II — they were lying to lenders about a representation in their credit agreement. They were not lying to the SEC. Because the SEC was not in the room.

The private letter ratings market

The disclosure gap doesn’t sit in a vacuum. It sits inside a ratings infrastructure that has been quietly shifting under everyone’s feet for the better part of a decade.

Moody’s, S&P, and Fitch — the so-called “Big Three” — still dominate public debt ratings. They rated First Brands’ senior loans (Fitch downgraded the company to CCC well before bankruptcy). What they don’t dominate, increasingly, is the private credit market.

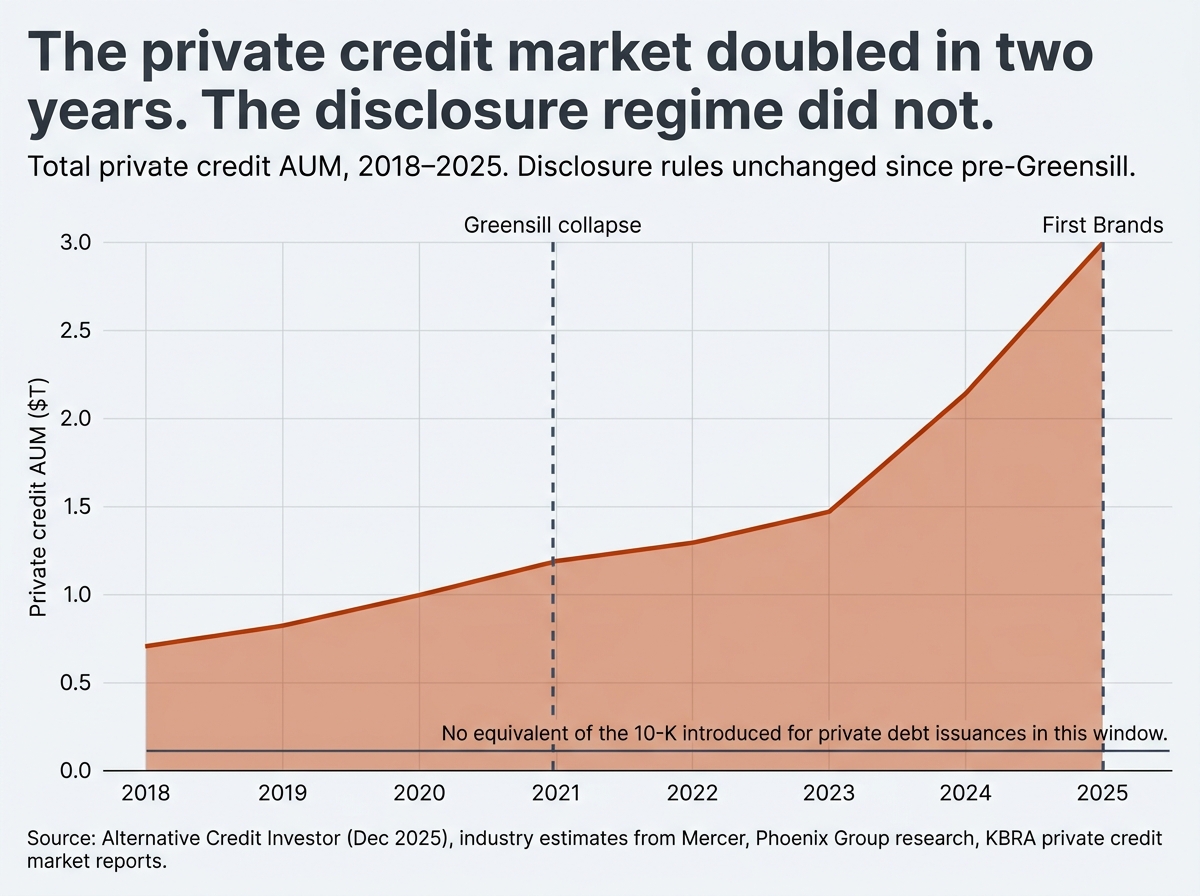

Private letter ratings are individually negotiated assessments issued for specific debt instruments to specific investors, typically not made public. Insurance companies use them to set capital charges under the National Association of Insurance Commissioners (NAIC) framework. Asset managers use them to satisfy fund-level mandates. The market has grown to fill the demand created by the broader explosion of private credit, which doubled from roughly $1.5 trillion in 2023 to $3 trillion by late 2025.

A clutch of smaller agencies has captured most of the growth: Egan-Jones, KBRA, Morningstar DBRS, AM Best, HR Ratings. Egan-Jones in particular has drawn scrutiny — a Bloomberg investigation reported the firm rated more than 3,000 investments in 2024 from a four-bedroom colonial outside Philadelphia. The NAIC’s Capital Markets Bureau has reported that ratings from smaller credit rating providers averaged about 3.01 notches more favorable than the regulator’s own Securities Valuation Office assessments, with 17 specific cases involving discrepancies wide enough to flip a security from speculative-grade to investment-grade for capital purposes.

That gap matters. An investment-grade designation lets an insurance company hold the asset against far less regulatory capital than a junk-grade designation. If the rating is wrong, the capital cushion is wrong, and the loss when something defaults is bigger than the capital model anticipated.

KBRA has publicly disputed criticism from Fitch and questioned the rigor of the underlying NAIC data. Egan-Jones has defended its private debt default record as below expected and pointed to consistency with major-agency public ratings. Both points are reasonable on their own terms. The structural issue is that the issuer pays for the rating, the market is opaque, and the agencies competing for share are competing on speed and favorability.

The First Brands SPV inventory financings and the supply-chain finance programs almost certainly received private letter ratings from somewhere in this market. The agency-by-agency mapping is not yet public — those mappings rarely are — but the structural reality is that the rated structures sat across a regulatory border where the Big Three weren’t and aren’t doing the work.

The lenders affected

The list of institutions exposed to First Brands reads like a who’s who of the credit markets.

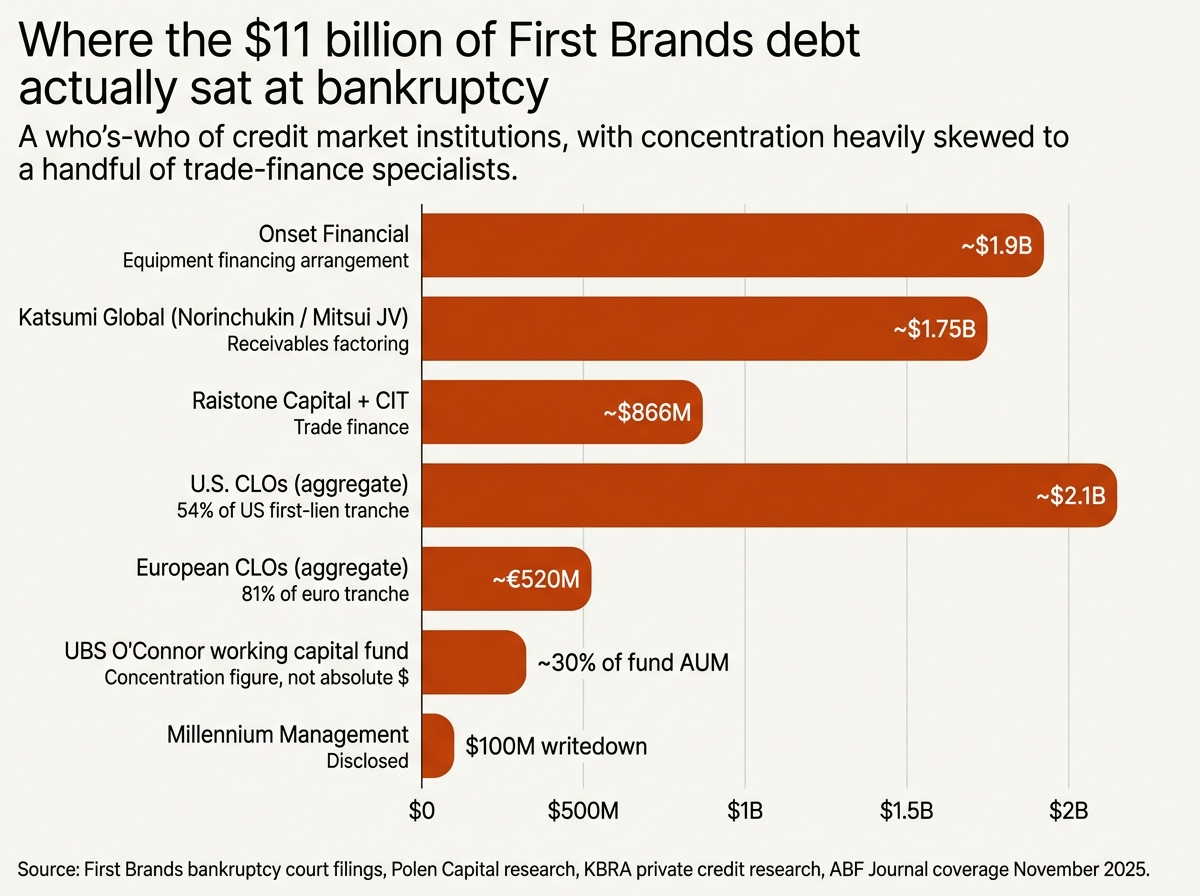

UBS O’Connor’s working capital finance fund held roughly 30% of the fund’s assets in First Brands exposure, the highest concentration of any institutional fund. Millennium Management took a roughly $100 million writedown. Onset Financial led a $1.9 billion equipment financing arrangement to purchase and lease inventory and equipment to First Brands. Katsumi Global, the Norinchukin / Mitsui JV, has approximately $1.75 billion of exposure. Raistone Capital and CIT, two trade finance specialists, have a combined $866 million in exposure. Apollo, in a rare positive note for an institution that’s normally on the wrong side of these stories, took a short position months before the collapse and made money.

Beyond the named institutions, U.S. CLOs hold approximately $2.1 billion of First Brands’ first-lien debt — about 54% of the dollar tranche. European CLOs hold an additional €520 million, about 81% of the euro tranche. KBRA research has noted that this represents only about 0.2% of overall CLO collateral in both markets, suggesting limited systemic risk at the CLO level even if individual deals take meaningful hits.

But CLOs are only the visible part of the loss exposure. The $5.4 billion of off-balance-sheet financing — factoring, SPV inventory finance, supply-chain finance — sits with a more diffuse set of holders: trade finance funds, asset-based lenders, working capital specialists, and the Japanese and European banks that increasingly fund this corner of the market. Recoveries on the off-balance-sheet structures depend heavily on whether the underlying invoices and inventory existed at all, which is exactly what the bankruptcy court is now trying to determine through forensic discovery.

The $1.1 billion in debtor-in-possession financing First Brands received to fund the restructuring was characterized by lenders in a court filing as “arguably among the riskiest in recent history” given the open fraud investigation.

The Greensill parallel

The First Brands collapse has drawn comparisons to the 2021 collapse of Greensill Capital, a UK-based supply-chain finance specialist whose unwinding cost Credit Suisse approximately $10 billion and contributed to that bank’s eventual collapse and absorption by UBS.

The parallels are real. Both involved off-balance-sheet supply-chain finance that masked the true leverage of the underlying borrowers. Both involved opaque private credit structures sold to institutional investors based largely on representations that turned out to be false. Both ended in fraud allegations against the principal — Lex Greensill, like Patrick James, has been the subject of civil litigation alleging he misrepresented the underlying receivables.

What didn’t happen after Greensill is also relevant. The Bank of England studied supply-chain finance disclosure. The Financial Stability Board issued guidance. Accounting standard-setters (IFRS in particular) considered tightening derecognition rules and issued limited guidance in 2023. None of it produced a meaningful change in how supply-chain finance and off-balance-sheet receivables programs are disclosed by private companies in the United States.

If the regulatory response to Greensill had hit harder, First Brands’ specific structure would have been at least partially visible to its own term-loan lenders. The disclosure regime that existed in 2021 is essentially the disclosure regime that existed in 2025. The market response to Greensill was higher pricing on the relevant structures and greater diligence at the deal level. The structural response was minimal.

The Patrick James indictment

On January 29, 2026, the U.S. Attorney’s Office for the Southern District of New York unsealed an indictment charging Patrick James, 61, of Chagrin Falls, Ohio, and his brother Edward James, 60, of Canton, Ohio, with nine federal counts. The headline charge is operating a continuing financial crimes enterprise, which carries a maximum sentence of life in prison. The other counts include conspiracy to commit wire fraud, conspiracy to commit money laundering, multiple counts of wire fraud, and bank fraud.

Both brothers were arrested in Ohio. A third defendant — Peter Andrew Brumbergs, 45, also of Chagrin Falls — pleaded guilty separately and is cooperating with the government. Brumbergs’s role in the alleged fraud has not been fully detailed publicly, but his guilty plea suggests the government has built its case on insider testimony in addition to forensic financial evidence.

Patrick James has denied the charges through a spokesperson, who said James “built First Brands from nothing into a global industry leader.” Edward James, through attorney Seth DuCharme, has called the indictment a “long list of accusations” without supporting evidence and said his client looks forward to defending himself in court.

The criminal case will turn on the government’s ability to prove specific intent — that Patrick James and Edward James knew the invoices were fraudulent and personally directed the fraud — across the full breadth of the seven-year period the indictment covers. The civil bankruptcy proceedings will continue separately, with Charles Moore and the new First Brands board pursuing claw-back actions against James and his entities. Both proceedings will likely run for years.

The criminal trial will determine whether two specific people go to prison. It will not determine whether the disclosure regime that allowed the fraud to scale gets fixed.

The risks to the disclosure-gap thesis

This piece argues that the structural failure was disclosure rather than fraud. There are several reasonable challenges to that thesis worth taking seriously.

First, the fraud may have been so brazen that no realistic disclosure regime could have caught it. If invoices are being fabricated and then double-sold to multiple factors, the fact pattern is criminal, not regulatory. A 10-K-style disclosure regime forces companies to describe their factoring programs in footnotes, but it doesn’t audit individual invoices. SEC reviewers don’t catch invoice fraud at private companies — they catch it at public companies, eventually, only after a whistleblower or a short-seller raises the alarm. The disclosure-gap argument may be overweighting how much better the SEC regime would have performed.

Second, sophisticated lenders are supposed to do their own diligence. UBS, Jefferies, and Apollo are not mom-and-pop operations. The fact that some of them — notably Apollo — did identify the problem and took short positions before the collapse suggests the diligence was possible. The lenders who lost money may have failed at their job rather than been blocked by a structural feature of the market. If that’s right, the answer isn’t more disclosure rules; it’s better lending discipline.

Third, the rating agencies hit by criticism have legitimate methodologies and track records that don’t deserve to be smeared by association. KBRA in particular has pushed back on the narrative that smaller agencies are systemically less rigorous, and the data on private credit default rates rated by smaller agencies isn’t yet conclusive that they are inflating ratings on average. The subset of bad ratings (e.g., the 17 NAIC cases) may be exactly that — a subset.

Fourth, a partial response is already underway. CLO lenders have tightened advance rates on receivables (now 80-85%) and inventory (45-50%), with industry sources reporting movement toward continuous collateral monitoring with AI-powered invoice verification. The market is correcting prices and processes even without regulatory intervention. The disclosure-gap thesis may be answering the question of whether there should be a structural fix at the moment when the market is already producing one.

These are real challenges. The strongest version of the disclosure-gap argument is not that better disclosure would have prevented fraud entirely — it’s that better disclosure would have made the fraud harder to scale to $11 billion before anyone noticed.

What to watch in 2026-2027

Three forward-looking signals worth monitoring through the next 18-24 months.

The NAIC moves on private letter ratings. The most consequential possible regulatory response sits with the National Association of Insurance Commissioners, which sets capital treatment for U.S. insurance companies — by far the largest end-buyers of private credit. The NAIC’s Securities Valuation Office has been reviewing privately rated securities since 2018, but the actual capital implications of an SVO override remain limited. If the NAIC moves to require its own designations to govern capital charges across the private credit assets insurers hold, the demand-side economics of insurer-owned private credit change overnight. Insurers would need to either raise more capital against the same assets or sell down exposure. Either response would tighten pricing across the entire private credit market.

The SEC and disclosure threshold rules. The Securities and Exchange Commission has the authority to require enhanced disclosure for large private debt issuances even when those issuances qualify for Rule 144A or other exemptions. The threshold conversation has not started in public yet. After First Brands, it will. Watch for staff guidance, no-action letters, or formal rulemaking proposals — any of which would signal the direction.

The civil case discovery in First Brands. Beneath the criminal trial, the bankruptcy estate’s civil litigation against Patrick James and the James Entities is doing structural work. As discovery proceeds, the question of which lenders knew, or should have known, about the off-balance-sheet structures will get answered in a court of law. Those answers will set precedent for how future fraud-overlay claims get adjudicated and may determine whether tier-2 rating agencies face contractual or tort liability for the structures they signed off on. Watch the docket in the Southern District of Texas (Case No. 25-03803).

The fraud was a $179.84 invoice altered to $9,271.25. The disclosure regime that let the fraud scale to $11 billion is the actual story — and nothing about that regime has yet changed. Expect more First Brands before the rules get rewritten.

FAQ

Why did First Brands Group go bankrupt?

The proximate cause was a failed refinancing in summer 2025, when lenders refused to roll the company’s debt at the marketed terms. The deeper cause was a fraud — alleged in civil and criminal proceedings — that involved inflated invoices, double-pledged collateral, and off-balance-sheet financing routed through founder-controlled entities. By the time of the September 2025 bankruptcy filing, the company had $12 million in cash and over $9 billion in liabilities, with another $5+ billion in off-balance-sheet obligations.

Who is Patrick James and what is he charged with?

Patrick James, 61, is the Malaysian-born founder and former CEO of First Brands Group. He founded what became First Brands in 2013. On January 29, 2026, he and his brother Edward James were indicted on nine federal felony counts including a continuing financial crimes enterprise charge that carries up to life in prison, plus conspiracy to commit wire fraud, conspiracy to commit money laundering, and multiple substantive wire and bank fraud counts. James has denied the charges through his lawyers.

How much money is missing from First Brands?

The bankruptcy estate has identified roughly $11 billion in total liabilities, of which approximately $5.4 billion was off-balance-sheet (not disclosed on the company’s reported financial statements). Federal prosecutors have separately alleged that more than $700 million of corporate cash flowed to Patrick James personally and to entities he controlled between 2018 and 2025. Approximately $12 billion total moved through Bowery Finance II — an account controlled by James — between 2022 and 2025.

What is private credit and how is it different from public debt?

Private credit refers to loans made by non-bank lenders — primarily asset managers, business development companies, insurance companies, and private credit funds — directly to companies, typically without the loans being publicly traded. The market has roughly doubled to $3 trillion since 2023. Unlike public debt, which trades on regulated exchanges and is subject to SEC disclosure rules at the issuer level, private credit operates under direct lender-borrower contracts with no centralized disclosure regime and no equivalent of the 10-K. Most institutional private credit assets are rated, but increasingly by smaller agencies issuing private letter ratings rather than the Big Three.

What are private letter ratings and why do they matter?

Private letter ratings are credit assessments issued for specific debt instruments and shared only with the issuer and certain investors, rather than published. They are used primarily by insurance companies (to satisfy NAIC capital requirements) and by asset managers (to satisfy fund-level mandates). The market has grown alongside private credit and is dominated by a clutch of smaller agencies — Egan-Jones, KBRA, Morningstar DBRS, AM Best, HR Ratings — that have taken share from Moody’s, S&P, and Fitch. The NAIC has reported that smaller agencies’ ratings average about 3 notches more favorable than the regulator’s own assessments, raising concerns about systematic rating inflation in the segment.

Could this happen again?

Yes. The structural conditions that allowed First Brands to scale a multi-layer financing fraud — fragmented disclosure across factoring, inventory finance, and supply-chain finance regimes; private letter ratings filling the gap left by the Big Three; no SEC equivalent of the 10-K for large private companies — remain in place. CLO lenders are tightening advance rates and adopting AI-powered invoice verification, but those are market-level responses to specific fraud risks, not structural fixes to the disclosure gap. Until the NAIC, SEC, or accounting standard-setters move, the conditions persist.

This analysis is based on public bankruptcy court filings in In re First Brands Group, LLC (S.D. Tex. Case No. 25-03803), the federal indictment of Patrick James and Edward James unsealed January 29, 2026, the November 3, 2025 declaration of Charles Moore (Chief Restructuring Officer), the Federal Reserve’s November 2025 Financial Stability Report, NAIC Capital Markets Bureau research on private letter ratings, and reporting from Bloomberg, Reuters, the Financial Times, Fortune, Morningstar, ION Analytics / Debtwire, ABF Journal, Global Trade Review, Polen Capital, and CNBC.

— Hamza, Footnote Brief