The 60-second version

In 2024, McDonald’s collected $10.0 billion in rent from its franchisees — substantially more than the $5.6 billion it collected in royalties on Big Mac sales. That’s the headline number that has fueled a decade of “McDonald’s is secretly a real estate company” coverage, and the underlying financial reality is real:

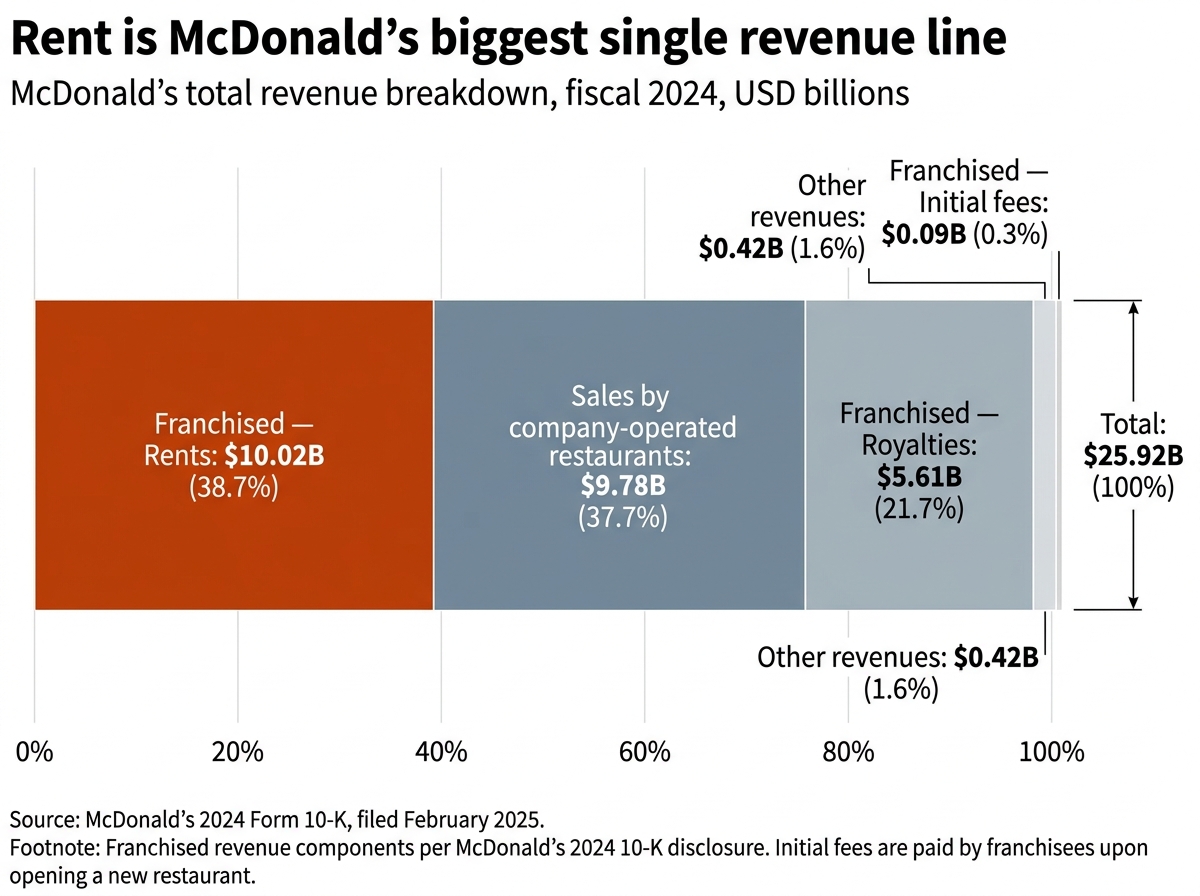

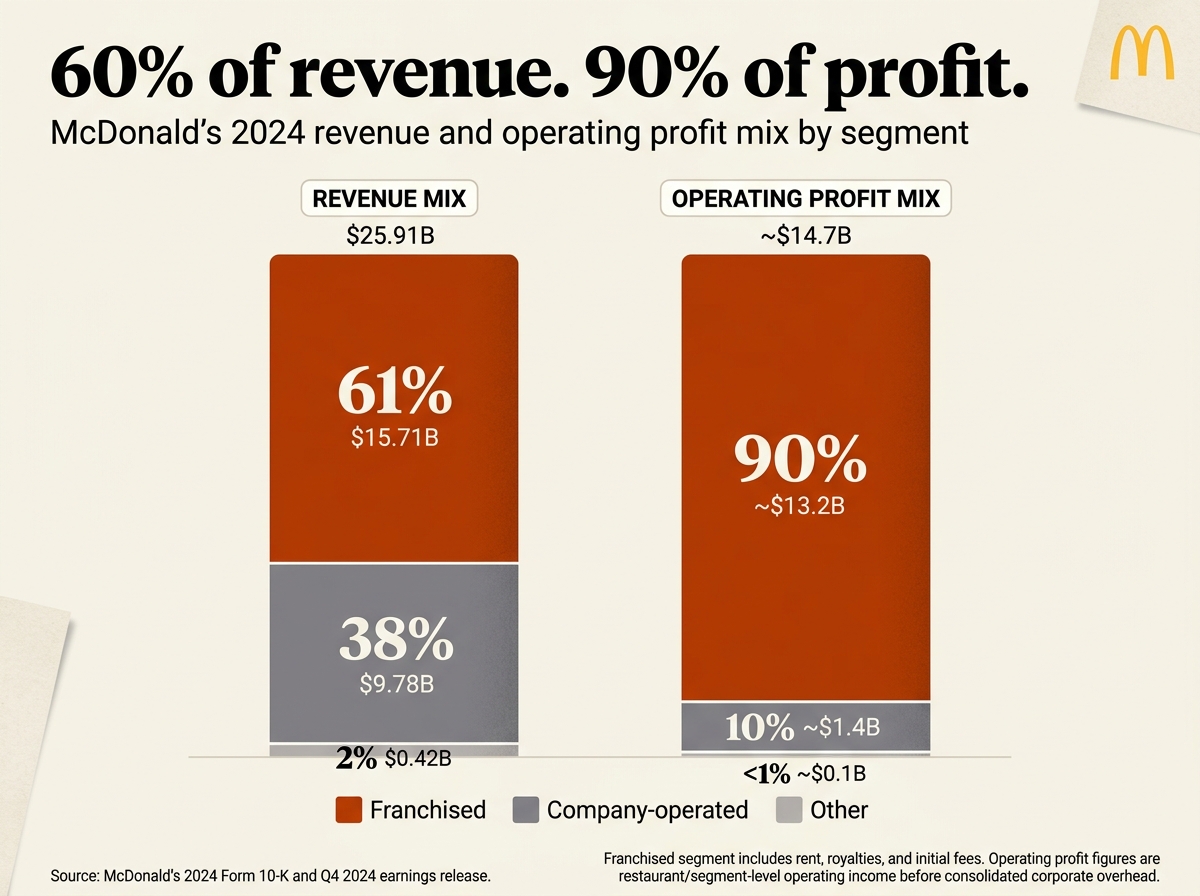

- Rent vs royalties. Per the 2024 10-K, McDonald’s franchised-restaurant revenue split out as $10.0B in rent, $5.6B in royalties, $0.09B in initial fees. Total franchised revenue: $15.7 billion of $25.9 billion in total company revenue (61%).

- Property footprint. McDonald’s owns the land underlying approximately 45% of its restaurants and the buildings for approximately 70%, per recent investor disclosures. With 43,477 restaurants worldwide at year-end 2024, that’s roughly 19,500 owned land parcels and 30,400 owned buildings — a portfolio comparable in scale to mid-sized public REITs.

- Book value vs market value. The 2024 balance sheet carries $25.3 billion in net property, plant, and equipment. That’s the depreciated GAAP book value. Analyst estimates of the market value of the underlying real estate portfolio range widely — from roughly $40 billion (conservative) to $120 billion or more (aggressive). The wide range reflects the fact that nobody outside McDonald’s has audited access to the underlying property-by-property data, and analyst methodologies differ substantially.

- Margin asymmetry. McDonald’s retains roughly 82 cents of every revenue dollar from franchised restaurants as gross profit, versus roughly 16 cents from company-operated restaurants. The franchise/real-estate side is structurally a much higher-margin business.

The story most coverage tells — McDonald’s is “secretly a real estate company” hiding inside a burger chain — captures something true. But it overstates the precision of the implied valuation, ignores the legal structure that prevents the company from being a REIT, and under-tells the more interesting story: a 1957 strategic decision by an obscure CFO that compounded into one of the most durable corporate disguises in American business history.

Skip to the section that interests you most

What McDonald’s Revenue Actually Looks Like

Pull McDonald’s 2024 Annual Report on Form 10-K and read the revenue section carefully. The total revenue figure of $25.9 billion has four components, and how those four components break down is the entire argument.

Sales by company-operated restaurants: $9.78 billion (37.7% of revenue)

This is McDonald’s selling burgers directly to consumers in the roughly 5% of stores it owns and operates. Revenue is recognized at the point of sale. After paying for ingredients, labor, rent (when the location is leased from a third party), and operating expenses, this segment generated approximately $1.4 billion in restaurant-level operating profit — a margin of about 14%.

Revenues from franchised restaurants: $15.71 billion (60.6% of revenue)

This is the segment everyone is talking about. It breaks into three sub-components disclosed in the 10-K:

- Rents: $10.02 billion

- Royalties: $5.61 billion

- Initial fees: $0.09 billion

Notice the proportion. Rent revenue from franchisees is nearly double the royalty revenue. McDonald’s collects more from being a landlord than from being a franchisor of intellectual property — and has every year since at least 2015.

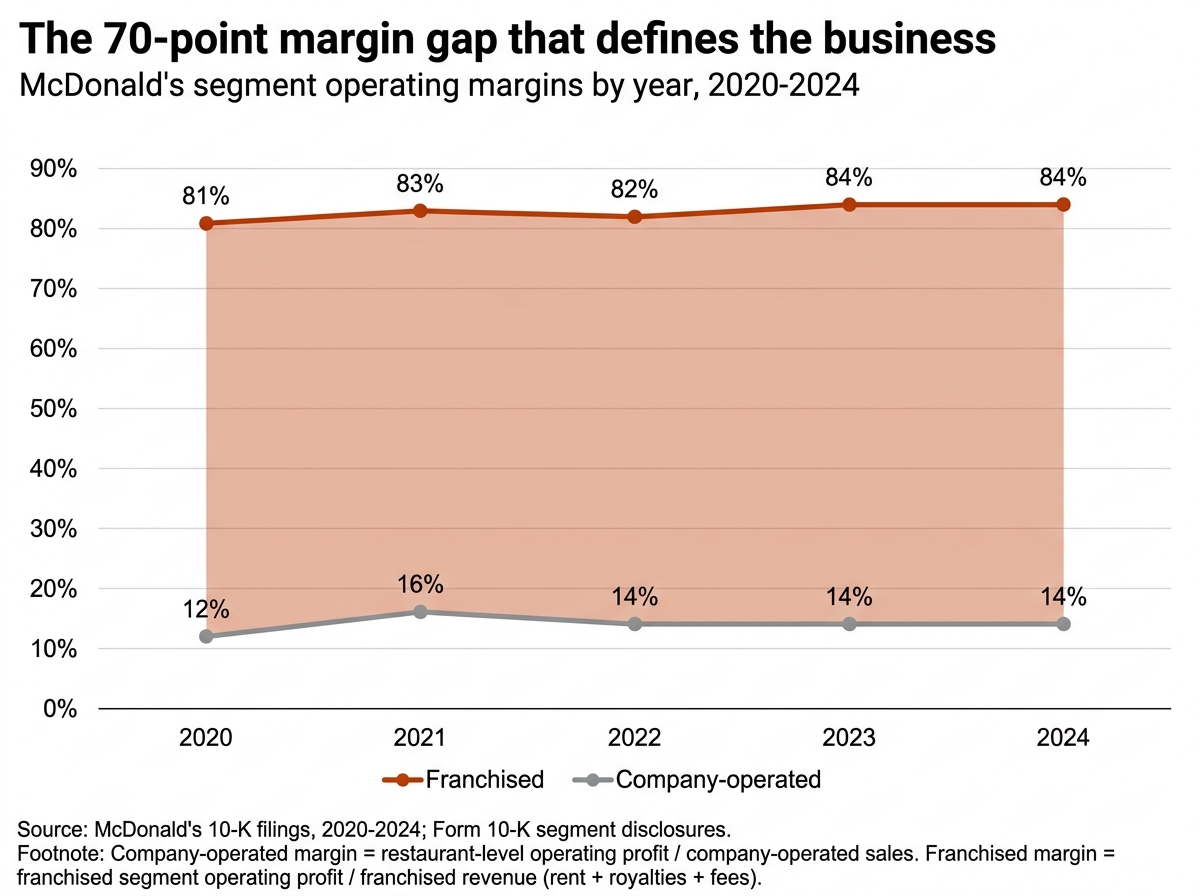

After paying for operating expenses associated with owning and maintaining the property base, the franchised-restaurant segment generated approximately $13.2 billion in operating profit. That’s a margin of about 84% — closer to a software business than a restaurant business.

Other revenues: $0.42 billion (1.6% of revenue)

This is technology fees from franchisees and brand licensing. Small in the context of the company.

Now do the math the script doesn’t do explicitly. The company-operated segment produces $9.8 billion of revenue and $1.4 billion of profit (14% margin). The franchised segment produces $15.7 billion of revenue and $13.2 billion of profit (84% margin). Even though company-operated revenue is more than half of franchised revenue, franchise profits are nearly ten times company-operated profits.

The company makes its money as a landlord and licensor, not as a restaurant operator. The roughly 1,800 stores McDonald’s directly operates (out of 43,477 total) function as a strategic operating laboratory — used for testing menu items, training franchisees, evaluating real estate locations, and demonstrating operational standards. They are not the profit engine.

That’s the structure. The next question is how it got that way.

1957: The Decision That Changed Everything

The standard story of McDonald’s begins in 1955 with Ray Kroc opening his first restaurant in Des Plaines, Illinois. The actual financial architecture began two years later, in 1957, when Kroc’s first chief financial officer — a former Tastee-Freez executive named Harry J. Sonneborn — proposed something his boss didn’t initially understand.

The problem Sonneborn was solving: McDonald’s at that point made a 1.4% royalty on every franchised store’s gross sales — a tiny number. Franchisees were running off with most of the value. Banks wouldn’t lend to McDonald’s against future royalty income because the cash flows were considered unstable. Kroc had ambition but no capital.

Sonneborn’s solution was to insert McDonald’s between the franchisee and the land. A new subsidiary — Franchise Realty Corporation — would lease or buy the land for each new restaurant, then sub-lease it to the franchisee. Franchisees would pay rent (a fixed minimum plus a percentage of sales) on top of their existing royalty. The genius was that bank lenders, who wouldn’t lend against royalties, would lend against the underlying real estate — meaning McDonald’s could now finance its expansion through mortgage debt secured by the land it was assembling, rather than through royalty-backed financing.

The historical line attributed to Sonneborn captures the strategy directly: “We are not technically in the food business. We are in the real estate business. The only reason we sell hamburgers is because they are the greatest producer of revenue, from which our tenants — franchisees — can pay us rent.” The quote is recorded in John F. Love’s 1995 book McDonald’s: Behind the Arches and has been widely repeated in business journalism since.

What’s important for the financial argument is what Sonneborn’s structure produces over time. As inflation lifts both food prices and commercial rents over decades, McDonald’s collects expanding rent payments on real estate it acquired at 1960s, 70s, and 80s prices. The accounting depreciation steadily lowers the book value of those properties on the balance sheet. The market value of those same properties — appreciating with the surrounding commercial real estate market — keeps rising. This is why the 10-K shows $25.3 billion of property at depreciated book value and analyst estimates can credibly argue the underlying portfolio is worth multiples of that.

Compounded over 65+ years, on tens of thousands of properties, in essentially every developed-economy commercial real estate market on Earth, the result is a property portfolio that is genuinely difficult to value precisely but unambiguously a strategic asset of the same order of magnitude as the McDonald’s brand itself.

The Numbers Nobody Reads in the 10-K

Most readers of the McDonald’s 10-K stop at the income statement. The interesting numbers are deeper.

Property and equipment at cost: $44.18 billion (2024)

- Land: $7.25 billion

- Buildings and improvements (on owned land): $20.49 billion

- Buildings and improvements (on leased land): $14.39 billion

- Equipment, signs, and seating: $2.05 billion

Less accumulated depreciation: ($18.88 billion)

Net property and equipment (book value): $25.30 billion

Two things to note immediately. First, McDonald’s has been depreciating its property base for decades — accumulated depreciation of $18.9 billion against $36.6 billion of buildings. This is normal GAAP accounting; depreciation reduces book value by a fixed percentage each year regardless of what the property is actually worth in the market. Second, the land line ($7.25 billion at cost) is not depreciated under GAAP — land is held at original cost forever, even if its market value has multiplied since acquisition.

To understand why this matters, consider a McDonald’s location in suburban Chicago acquired in 1972 for $150,000 of land and $200,000 of building. Fifty years of depreciation drives the building’s book value to roughly zero. The land is still on the books at $150,000. The actual market value of the parcel — a corner lot in a now-densely-developed suburb, zoned commercial, with road frontage — is plausibly $3-5 million. The 10-K doesn’t show that. It shows the original $150,000 plus a near-zero remaining building value, for a total around $200,000 against a market value 15-25x higher.

Multiply this dynamic across 19,500 owned land parcels and 30,400 owned buildings, almost all acquired between 1960 and 2010, and you get the structural reason why analyst estimates of the real estate portfolio’s market value range so widely. The book value is anchored to historical cost. The market value is anchored to current commercial real estate prices, which have risen substantially over the same period.

Sample analyst estimates of the underlying real estate market value:

- Macquarie Asset Management research (2025): approximately $120 billion (as cited in popular finance media; original report not publicly archived)

- Conservative book-value-multiple analyses: $40-50 billion (assuming the depreciated buildings are worth less than naive multiples imply)

- Mid-range commercial-cap-rate estimates: $70-90 billion (capitalizing the $10B rent stream at typical net lease cap rates of 5-7%, then adjusting for portfolio quality)

The honest answer is that the precise figure is unknowable without property-by-property auditing that nobody outside McDonald’s has done. But every credible methodology produces a number meaningfully higher than the GAAP book value — the question is by how much.

Why Franchise Margins Dwarf Restaurant Margins

This is the other side of the story. Even if the real estate isn’t formally a REIT, the economics of being a landlord-licensor are dramatically better than being an operator.

Across the McDonald’s segments, the 2024 operating margin profile:

- Company-operated restaurants: ~14% restaurant-level margin

- Franchised restaurants: ~84% segment-level margin

- Consolidated company operating margin: ~46%

The 70-percentage-point gap between the two segment margins is not driven by McDonald’s being a particularly efficient operator — its company-operated stores produce margins similar to or slightly below industry peers. The gap is driven by the structural asymmetry: when a franchisee pays McDonald’s rent and royalties, McDonald’s has almost no associated cost of goods sold, almost no labor, almost no inventory, almost no waste. The cost of being a landlord is property tax, insurance, and depreciation. The cost of being a licensor is essentially zero on a marginal basis.

Compare to a pure-play restaurant operator like Chipotle or Texas Roadhouse, both of which run consolidated operating margins in the 12-17% range. McDonald’s blended 46% operating margin is double or triple those, and the explanation is entirely the franchise/landlord structure.

The compounding effect is what makes McDonald’s stock such a long-duration asset. A company-operated restaurant pays McDonald’s fixed wages, food costs, and lease payments quarterly. Those costs rise with inflation. A franchisee pays McDonald’s rent and royalties as a percentage of sales — meaning McDonald’s revenue from each franchise rises automatically with menu price inflation, with effectively no incremental cost. The structural inflation hedge built into the model is the reason McDonald’s has been able to grow free cash flow consistently for decades while operators of similar age have struggled with margin compression.

Where This Would Rank Among Actual REITs

Here’s where the popular framing — “McDonald’s would be the largest REIT on Earth” — needs careful unpacking.

Top US REITs by market capitalization (Q1 2025):

- Welltower (WELL) — Healthcare/senior housing — ~$128 billion

- Prologis (PLD) — Industrial/logistics — ~$98 billion

- American Tower (AMT) — Communications towers — ~$102 billion

- Equinix (EQIX) — Data centers — ~$95 billion

- Simon Property Group (SPG) — Retail malls — ~$53 billion

- Realty Income (O) — Net lease retail — ~$50 billion

- Public Storage (PSA) — Self-storage — ~$50 billion

If McDonald’s real estate portfolio were valued at a midpoint of credible estimates — call it $90 billion — it would rank fourth or fifth, comparable to Equinix or larger than Simon Property Group. At the aggressive end of $120 billion, it would compete with Welltower and Prologis for the top spot. Even at the conservative end of $40 billion, it would rank in the top 25 US REITs by market cap.

The “largest REIT on Earth” framing is plausible but not certain. The defensible claim is that McDonald’s real estate portfolio, if spun off and properly valued, would unambiguously rank among the largest commercial real estate holdings in the world. Whether it would specifically be number one depends on which valuation methodology you pick.

What’s more interesting than the ranking is the type of real estate. Most large REITs specialize: Welltower in healthcare, Prologis in logistics, Simon in malls, Equinix in data centers. McDonald’s real estate is essentially a portfolio of high-traffic, road-frontage commercial corner lots in nearly every developed-economy market in the world. That kind of geographic and demographic diversification is genuinely rare in public-market real estate.

Spin It Off, or Keep the Disguise?

The question of whether McDonald’s should spin off its real estate into a standalone REIT is not new. Activist investors raised it in 2015. Larry Robbins of Glenview Capital pushed it. Bill Ackman has flirted with it. McDonald’s management has consistently said no.

The argument for a spin: Unlock value. The market currently values McDonald’s at roughly $200 billion enterprise value. If the real estate portfolio alone is worth $90-120 billion, the implied valuation of the operating brand+franchise business is between $80-110 billion — meaning the market is arguably underpricing one or both pieces. A spin-off would force a clean public-market valuation on each.

The argument against a spin: The structure is the moat. The reason McDonald’s franchise model works is precisely because the parent company controls the real estate and can use rent escalation to discipline franchisee behavior, evict underperformers, and capture the inflation hedge described above. Separating the real estate into a REIT structure would convert McDonald’s from a vertically integrated landlord-franchisor into a franchisor that pays rent to a third party — destroying the integration that makes the existing economics work.

There’s also a tax problem. To qualify as a REIT under U.S. tax code, an entity must distribute at least 90% of its taxable income as dividends. That’s a very high payout ratio that would constrain McDonald’s ability to reinvest in the operating business. The current structure lets McDonald’s keep more cash inside the corporate entity for menu innovation, technology investment (loyalty apps, kiosks, drive-thru improvements), and international expansion. A REIT spin would force a different capital allocation discipline.

Then there’s the disclosure problem. As a single corporate entity, McDonald’s reports the real estate portfolio as part of its broader operations. Property-by-property valuations are not disclosed. A REIT spin would force detailed disclosure of every property’s location, size, lease terms, and rent — information that McDonald’s currently treats as competitively sensitive.

Management’s argument, articulated repeatedly across multiple investor calls, has been: the integrated structure produces a higher long-term return on capital than the sum of two separate entities would. Whether that’s true is genuinely contested. Activists have data showing the spin could create $20-30 billion of value via re-rating. Management has data showing the integration is worth more than the re-rating gain. The board has consistently sided with management.

What This Actually Means for the MCD Investment Thesis

Step back from the real estate framing.

McDonald’s stock has compounded at roughly 11% annually over the past 20 years, beating the S&P 500 by a comfortable margin. The story of why it has performed this way is structurally simpler than the “secret real estate company” framing suggests, but it’s the same story.

McDonald’s has three structural advantages stacking on top of each other:

- A globally recognized consumer brand that supports premium royalty rates and franchisee demand

- A real estate portfolio that produces $10 billion of high-margin rent revenue with built-in inflation escalation

- A franchise model that converts a labor-intensive, low-margin restaurant business into a high-margin, capital-light landlord-licensor business

The real estate dimension is the second of those three advantages. It’s not the entire story. But it’s the dimension that most investor and financial coverage misses, and it’s the dimension that makes McDonald’s economics structurally different from peers like Burger King (Restaurant Brands International), Yum! Brands, or Chipotle.

For the investor today: the question is not “is McDonald’s secretly a real estate company” — yes, partially, in a meaningful and demonstrable way. The question is “is the integrated structure being properly priced by the market.” Different analysts will answer that differently. Bulls argue the market underprices the real estate optionality. Bears argue the market correctly prices the structural inflation hedge already, with no further upside. The question turns on what assumption you make about the long-run trajectory of commercial real estate values, which is itself a function of interest rates, urbanization patterns, and the durability of brick-and-mortar retail in an age of digital substitution.

The Headline Takeaway

McDonald’s is, demonstrably, a real estate company in addition to being a restaurant company. The 2024 income statement shows $10.0 billion of rent against $5.6 billion of royalties. The balance sheet shows $25.3 billion of property at depreciated book value, against credible analyst estimates of $40-120 billion at market value. The economics of being a landlord-licensor produce 84% segment margins versus 14% restaurant margins.

Where the popular framing overreaches is in the certainty around exactly how much the real estate is worth, exactly where it would rank if spun off, and exactly what the value would be unlocked. The defensible answer is that McDonald’s real estate portfolio is among the largest privately held commercial real estate holdings in the world, that it produces a structurally higher-margin revenue stream than the food business itself, and that the 1957 strategic decision by Harry Sonneborn to insert the corporation between the franchisee and the land created a compounding advantage that has now run for nearly seven decades.

The headlines will keep calling it a “secret” or a “disguise.” The 10-K has been telling the story openly for 50 years. Most readers just stop at the income statement.

Frequently Asked Questions

Is McDonald’s actually a real estate company?

Functionally, yes, and the 10-K proves it. In 2024, McDonald’s collected $10.0 billion in rent from franchisees versus $5.6 billion in royalties on Big Mac sales. The real-estate side of the business produced approximately 84% segment margins versus 14% for company-operated restaurants. The company owns the land underlying ~45% of its restaurants and the buildings for ~70%, totaling roughly 19,500 owned land parcels and 30,400 owned buildings worldwide. Legally, McDonald’s is a corporation, not a REIT, so it doesn’t qualify as a real estate investment trust under U.S. tax code. But economically, the real-estate function is the larger and more profitable side of the business.

How much rent does McDonald’s collect from franchisees?

Per the 2024 10-K, McDonald’s collected $10.02 billion in rent from franchisees in 2024, up from $9.84 billion in 2023 and $6.84 billion in 2020. Rent revenue has grown consistently every year, driven by new store openings, lease escalations on existing properties, and same-store sales growth (rents are typically calculated as a fixed minimum plus a percentage of franchisee sales). Rent represents approximately 64% of McDonald’s franchised-restaurant revenue, with the rest coming from royalties (~36%) and small initial fees.

Why did Harry Sonneborn change the McDonald’s business model in 1957?

Harry Sonneborn, McDonald’s first chief financial officer, identified a financing problem: McDonald’s was making only a 1.4% royalty on franchised store sales, and banks wouldn’t lend against future royalty cash flows. Sonneborn proposed a new subsidiary, Franchise Realty Corporation, that would buy or lease the land for new restaurant locations, then sub-lease the property to franchisees. Banks would lend against the underlying real estate (which they considered safe collateral), allowing McDonald’s to scale rapidly. Sonneborn is credited with the line “We are not technically in the food business. We are in the real estate business.” Recorded in John F. Love’s 1995 book McDonald’s: Behind the Arches.

Why isn’t McDonald’s a REIT?

Two reasons. First, to qualify as a REIT under U.S. tax code, an entity must distribute at least 90% of its taxable income as dividends, a very high payout ratio that would limit McDonald’s ability to reinvest in the operating business (technology, international expansion, menu innovation). Second, the integrated structure is part of the moat: by controlling both the real estate and the franchise relationship, McDonald’s can use rent terms to discipline franchisee behavior and capture inflation upside. Activist investors have repeatedly proposed spinning off the real estate into a standalone REIT to unlock valuation; management has consistently declined.

How much is McDonald’s real estate portfolio actually worth?

The honest answer is that no one outside McDonald’s knows precisely. The 2024 balance sheet carries $25.3 billion in net property, plant, and equipment at depreciated book value. Analyst estimates of the market value range widely: conservative book-multiple analyses suggest $40-50 billion; mid-range cap-rate methodologies (capitalizing the $10B rent stream at typical net lease cap rates of 5-7%) produce $70-90 billion; aggressive estimates including portfolio quality and inflation upside reach $120 billion or more. The wide range reflects the absence of property-by-property data outside the company. What’s certain is that the market value substantially exceeds the book value, because GAAP holds land at historical cost and depreciates buildings over 25-40 years regardless of what they’re actually worth.

How does McDonald’s make money?

McDonald’s has three revenue streams. First, sales by company-operated restaurants (~38% of 2024 revenue, ~14% margin), direct food sales at the ~5% of restaurants McDonald’s runs itself. Second, rent and royalties from franchised restaurants (~61% of revenue, ~84% margin), the core profit engine. Within franchise revenue, rent is roughly $10B and royalties are roughly $5.6B annually. Third, technology fees and brand licensing (~2% of revenue). The franchise/real-estate side of the business contributes roughly 90% of consolidated operating profit despite being slightly less than two-thirds of revenue.

Should McDonald’s spin off its real estate?

Activists have proposed it repeatedly (Bill Ackman, Larry Robbins, others). Management has consistently declined. The argument for: a clean public-market valuation of the real estate portfolio could unlock $20-30 billion of value through re-rating. The argument against: the integrated structure is the moat, separating the real estate would weaken franchisee discipline, force REIT-mandated 90% dividend payouts that constrain reinvestment, and require detailed property-by-property disclosure that McDonald’s treats as competitively sensitive. The board has consistently sided with management’s position that the integrated structure produces higher long-term returns than the sum of two separate entities would.

What percentage of McDonald’s restaurants does the company own?

Of McDonald’s 43,477 restaurants worldwide at year-end 2024, approximately 95% are operated by franchisees and ~5% are company-operated. However, the ownership picture for the underlying real estate is different and more important: McDonald’s owns the land for roughly 45% of all restaurants (regardless of who operates them) and the buildings for roughly 70%. For the remaining locations, McDonald’s holds long-term leases from third-party landlords and sub-leases to franchisees, capturing a markup on the rent.

Footnote Brief reads public companies’ filings so you don’t have to. Twice-weekly breakdowns at footnotebrief.com.

Sources: McDonald’s 2024 Annual Report on Form 10-K (filed February 2025), SEC; McDonald’s Q4 2024 earnings release; McDonald’s Investor Overview Deck (June 2025); Macquarie Asset Management — “McDonald’s: A Real Estate Powerhouse” research note (2025); S&P Global Market Intelligence — “Largest US Equity REITs by Market Cap” (January 2025); John F. Love, “McDonald’s: Behind the Arches” (Bantam Books, 1995); The Motley Fool — “Largest Real Estate Companies by Market Cap” (April 2026); Statista / Financial Times — Global REIT market cap rankings (April 2025); Stock-Analysis-on-Net — McDonald’s revenue and property breakdown (2024); Young Investor Journey / FourWeekMBA / mmcginvest.com — secondary financial framework analyses.