The 60-second version

The case in five sentences: Netflix stopped reporting subscriber numbers in Q1 2025, launched an ad tier that now has 94 million users (40% of accounts), signed billions of dollars in live sports rights including WWE and NFL, raised US prices three times in 14 months, and is bundling distribution through ISP and wireless partnerships. Stack those moves together and the result is a near-perfect rebuild of HBO’s 1995 business architecture — premium pricing, originals as the moat, ad-supported lower tier, exclusive sporting rights, bundled distribution.

The contrarian point: Streaming didn’t kill the cable bundle. It rebuilt it with software margins. Netflix’s 29.5% operating margin at 325 million subscribers is HBO’s profit profile at scale — the outcome the cable industry would have wanted if it could have shed its physical infrastructure costs.

Why hiding the subscriber count was the tell: Net subscriber adds dropped from 41 million in 2024 to 23 million in 2025 — a 44% deceleration. Removing the metric reduced investor focus on the slowdown. The Apple precedent (stopped reporting iPhone units in 2018 right as growth decelerated) is the closest playbook.

What to watch: The ad tier holding above 50% of new sign-ups, additional live sports rights (especially NFL Sunday), more ISP/carrier bundling, a third price increase before 2027, and ad revenue growth holding 100%+ annual rates toward $5-6 billion in 2027.

Skip to the section that interests you most

In April 2024, Netflix made an announcement that should have been the most-discussed sentence in modern media. Buried in a quarterly shareholder letter that mostly celebrated record subscriber growth, the company said it would stop reporting quarterly subscriber numbers starting in Q1 2025.

Wall Street noticed — Netflix shares dropped 9.1% the next day. But the analysis that followed mostly framed the move as a maturity signal, a company graduating from growth-stage metrics to profit-stage ones. That’s the surface read. The deeper read, when you stack the announcement against everything else Netflix did in 2024 and 2025, is harder to dismiss: Netflix is rebuilding cable’s business model, with better margins and better delivery.

This is a comprehensive analysis of how Netflix is recreating the cable bundle’s economic structure — premium pricing, advertising-supported lower tiers, live event programming, opaque metrics — and what it means for investors, advertisers, and the future of streaming.

The four moves that reveal Netflix’s real strategy

The case isn’t built on any single decision. It’s built on four moves taken together, each of which mirrors how premium cable networks operated for thirty years.

Move 1: Netflix stopped reporting subscriber numbers in 2025

In its Q1 2024 earnings, Netflix announced it would no longer disclose quarterly membership numbers or average revenue per member (ARM) starting in Q1 2025. The company’s stated reasoning, per its shareholder letter: “the number of members times the monthly price is increasingly less accurate in capturing the state of the business.”

The change took effect with Q1 2025 results. Netflix continues to disclose annual revenue and operating income forecasts, regional revenue breakdowns, and quarterly EPS — but the metric that defined streaming wars coverage for fifteen years is gone.

Wall Street’s reaction was telling. Wedbush Securities analyst Alicia Reese noted in an April 2025 research note that the change allowed Netflix to “obscure subscriber churn while showing meaningful revenue growth.” Macquarie’s Tim Nollen drew a direct parallel to Apple’s 2018 decision to stop reporting iPhone unit sales — a move that came right as iPhone unit growth was decelerating sharply.

Netflix’s growth has, in fact, been decelerating. The company added approximately 41 million net subscribers in 2024 but only 23 million in 2025 — a 44% drop in net adds. US penetration has reached 53%. UK penetration is 57%. Australia is at 65%. The “easy” markets are saturating.

When a high-growth company stops reporting growth metrics, the most parsimonious explanation is rarely “the metric became less relevant.” It’s “the metric became less flattering.”

Move 2: The ad tier became the dominant new sign-up

Netflix launched its Standard with Ads tier in November 2022 at $6.99/month — a steep discount from its then-$15.49 standard ad-free plan. The launch was widely interpreted as Netflix bowing to investor pressure after the company’s first-ever subscriber decline in early 2022.

What happened next reframes the entire decision.

By May 2025, Netflix’s ad-supported tier had reached 94 million monthly active users globally — roughly 40% of total active accounts. In markets where the ad tier is available, more than half of new subscribers now choose the ad-supported option over ad-free plans.

The financial impact is accelerating. Netflix reported Q3 2025 ad revenue of $662.3 million, representing about 5.8% of the quarter’s $11.51 billion total revenue. The company has guided to roughly $3 billion in 2026 ad revenue — double the 2025 figure — and analysts at Ainvest project the trajectory could reach $9 billion by 2028-2029.

Critically, more than 50% of new subscribers in eligible markets are choosing the ad tier. This is not a small experimental option. It’s the dominant entry point for new customers.

A premium subscription service where the majority of new sign-ups choose a cheaper, ad-supported tier isn’t really a pure subscription business. It’s a hybrid model — exactly what cable channels operated as for decades. Cable channels charged operators carriage fees (the subscription analog) and sold advertising inventory to brands (the ad revenue analog). Netflix now does both.

Move 3: Netflix moved aggressively into live sports and events

Netflix executives spent years insisting they had no interest in live sports. Sports rights were too expensive. The economics didn’t work. The platform was about on-demand entertainment.

Then 2024-2025 happened.

In January 2024, Netflix announced a 10-year, $5 billion deal for WWE Raw, which began streaming weekly in January 2025. The deal also gives Netflix global rights outside the US to all WWE programming including SmackDown, NXT, pay-per-view events, and the WWE library.

In March 2024, Netflix acquired NFL Christmas Day games, with two games in 2024 and at least one annual game in 2025 and 2026. The 2024 Christmas games averaged 26.5 million US viewers each.

In November 2024, Netflix streamed the Jake Paul vs. Mike Tyson boxing match, which the platform reported drew approximately 108 million viewers globally.

In 2025, Netflix added the Katie Taylor vs. Amanda Serrano boxing rematch and the Canelo Álvarez vs. Terence Crawford fight. The company also acquired exclusive rights to the FIFA Women’s World Cup for 2027 and 2031, the 2026 World Baseball Classic in Japan, and a package of MLB special events including the Field of Dreams game and Home Run Derby starting in 2026.

The pattern is precise: Netflix is acquiring exactly the sports rights that defined what cable channels were for thirty years. Wrestling. Boxing. Tentpole NFL events. International soccer. Tournament-style baseball broadcasts.

Netflix executives have been explicit they don’t want full-season league deals — they want what cable always wanted: appointment-viewing live events that anchor the bundle and reduce churn. Netflix calls this an “events over seasons” strategy. It’s the precise structure that made HBO and ESPN the most profitable networks of the cable era.

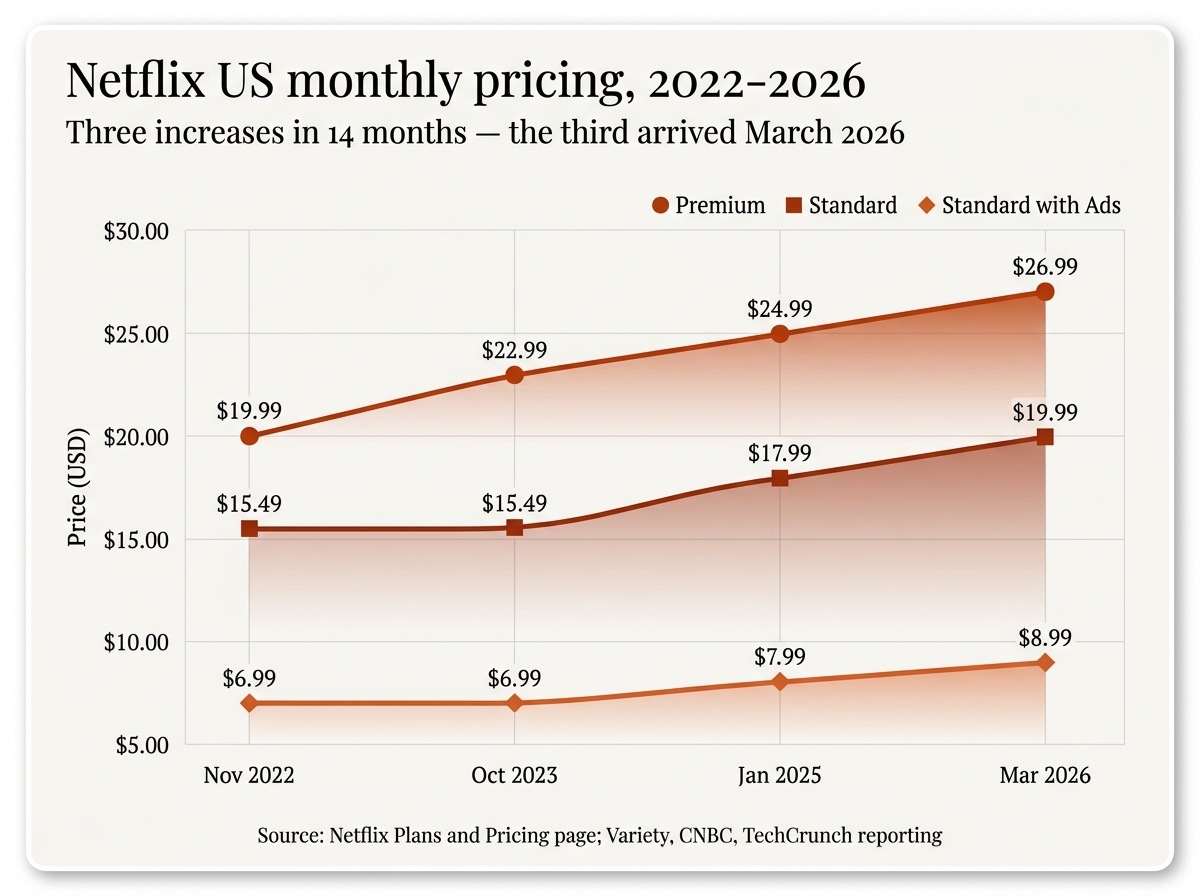

Move 4: Premium pricing power, repeated price increases

Netflix has raised US prices three times in 14 months as of March 2026.

The pricing trajectory:

- Standard with Ads: $6.99 (Nov 2022 launch) → $7.99 (Jan 2025) → $8.99 (March 2026)

- Standard ad-free: $15.49 → $17.99 (Jan 2025) → $19.99 (March 2026)

- Premium: $22.99 → $24.99 (Jan 2025) → $26.99 (March 2026)

According to TD Cowen estimates, the March 2026 price increase represents an 11% blended increase across Netflix’s product suite, and will lift average revenue per US subscriber by 6% year-over-year in 2026.

What’s notable is the market’s acceptance. MoffettNathanson research estimates Netflix delivers approximately 48 cents per hour of viewing — the lowest revenue-per-hour metric among major streamers, well below Disney+/Hulu (64 cents), Peacock, HBO Max, and Paramount+ (which range from 64-93 cents per hour viewed). That gap signals Netflix has additional pricing power before competitive pressure becomes meaningful.

This is the exact pricing dynamic HBO operated under at its peak. HBO commanded premium prices because its brand could carry them, and customers stayed because the content quality justified the gap.

How this compares to HBO’s playbook from 1995

The HBO comparison isn’t decorative. It’s structural.

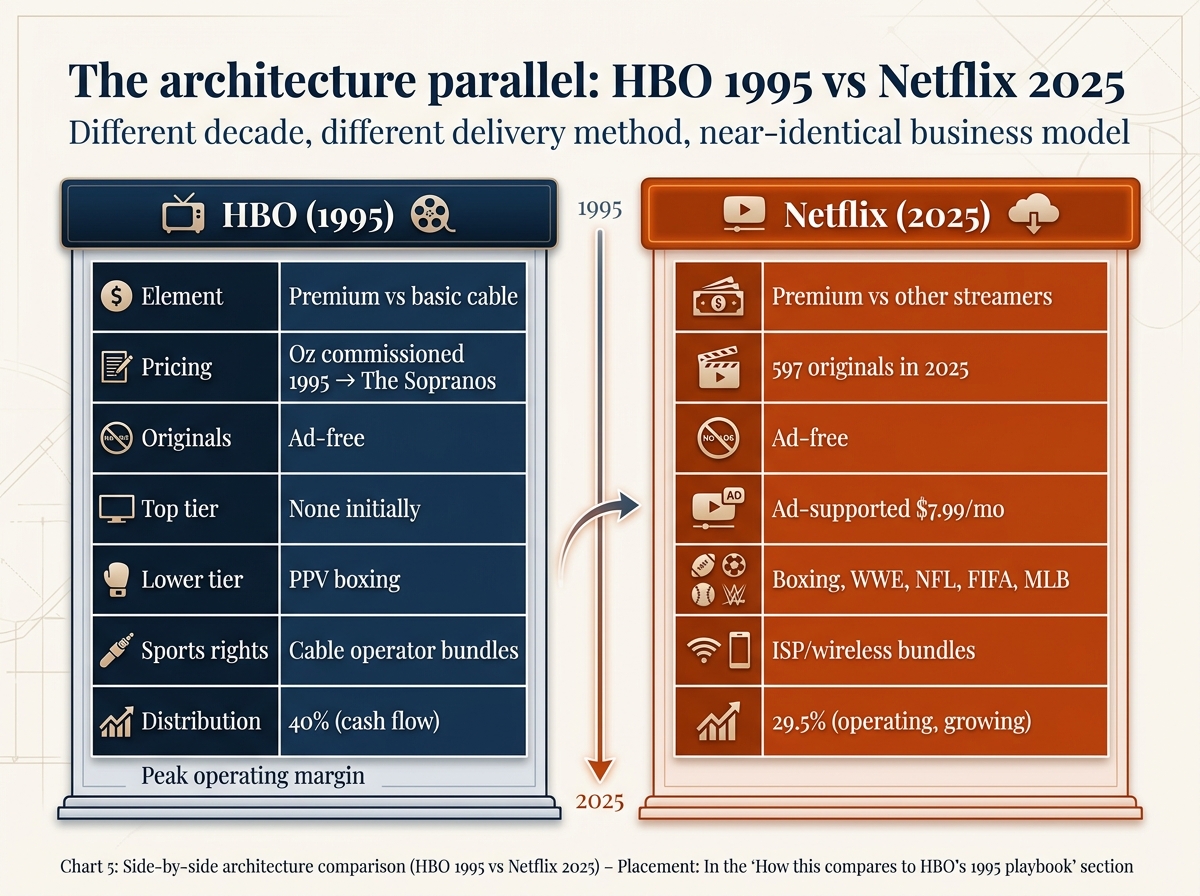

In 1995, HBO was operating with a specific business architecture that defined premium cable for two decades:

- Premium pricing versus basic cable channels

- Original programming as the moat (Oz was commissioned in 1995, premiered in 1997, and kicked off the prestige TV era that culminated in The Sopranos)

- Ad-free at the top tier

- Exclusive sporting rights, including pay-per-view boxing

- Bundled distribution through cable operators that made the actual cost feel invisible to consumers

By the mid-2000s, HBO was generating $1.2-1.5 billion in annual profits at a 40% cash flow margin, making it the third most profitable network in the world.

Netflix in 2025-2026 operates with the same architecture:

- Premium pricing versus other streaming services (with the lowest revenue-per-hour, suggesting more headroom)

- Original programming as the moat (Netflix released 597 originals in 2025, planning $20 billion in content spend for 2026)

- Ad-free at the top tier with a cheaper ad-supported option below

- Exclusive sporting rights, including boxing, WWE, NFL, FIFA Women’s World Cup

- Bundled distribution through Comcast’s Xfinity StreamSaver, Verizon’s plans, and various ISP partnerships

The financial outcomes are converging too. Netflix reported 2025 operating margin of 29.5% and is guiding to 31.5% in 2026 on $50.7-51.7 billion in revenue. That’s not yet HBO at peak but it’s closing fast — and Netflix has 325 million subscribers versus HBO’s peak of roughly 35 million US subscribers in the mid-2000s.

What about cord cutting? Didn’t streaming kill cable?

Here’s where the conventional narrative fails.

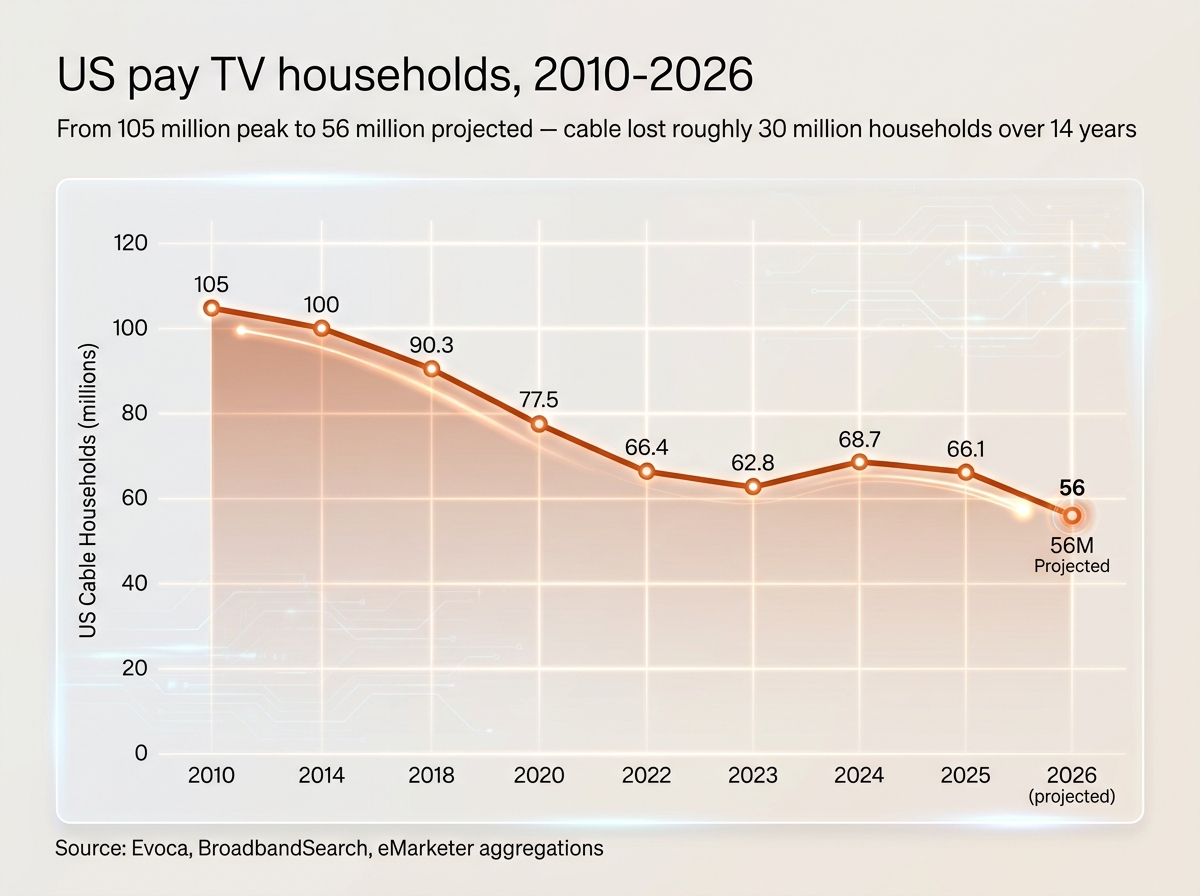

US cable TV has lost approximately 30 million subscribers since 2012, according to industry research aggregated by Zippia, Evoca, and BroadbandSearch. Pay TV revenue dropped from $100 billion in 2017 to $83 billion in 2025. By 2026, US cable subscriber count will fall to around 56 million households, down from 71 million in 2020.

Cable is losing customers. That’s true.

But cable’s business model didn’t die. It was reproduced.

Consider what cable was, structurally:

- A bundled distribution layer (the cable operator)

- Premium and basic content tiers (HBO at the top, ad-supported channels below)

- Live events as anchors (sports, news, awards shows)

- Aggregated billing (one monthly bill, multiple services)

- Geographic and demographic ad targeting (cable’s local advertising business)

Now consider streaming in 2026:

- Bundled distribution through Comcast Xfinity StreamSaver, Verizon’s plans, T-Mobile’s Experience plans, the Disney+/Hulu/HBO Max bundle, and Apple TV+/Peacock bundles

- Premium and ad-supported tiers (Netflix’s $26.99 Premium versus $8.99 Standard with Ads)

- Live events as anchors (NFL, WWE, boxing, MLB events)

- Aggregated billing through ISP and wireless partnerships

- Programmatic ad targeting through Netflix’s Ads Suite, partnerships with The Trade Desk, Amazon, Google DV360, and Yahoo DSP

The cable bundle, examined structurally, is back. The delivery mechanism changed from coaxial cable to broadband internet. The economics — premium content at premium prices, ad-supported tiers at lower prices, live events to anchor retention, bundling to reduce billing friction — are essentially identical.

What changed is the margin structure. Streaming companies don’t pay union-scale field crews to maintain physical infrastructure. They don’t carry the regulatory baggage that came with broadcast and cable licensing. They have software margins on a content delivery business. That’s why Netflix’s 29.5% operating margin matters: it’s HBO’s margin profile at significantly larger scale.

What this means for investors

If you accept the analysis that Netflix is rebuilding the cable bundle’s economic structure, several investor implications follow:

The pricing power is real but not infinite. Netflix’s revenue-per-hour-viewed metric of 48 cents is the lowest in the streaming sector. That suggests room to raise prices. But it also reflects Netflix’s volume-driven model — viewers spend more total time on Netflix than competitors, which dilutes the per-hour revenue. The relevant question for the next 24 months isn’t whether Netflix can raise prices (history says yes) but whether subscriber churn accelerates as cumulative price increases stack. The March 2026 increase was the second in 14 months. A third in 12 months would test the elasticity assumption.

Ad revenue is the leverage. Netflix’s ad revenue went from negligible in 2022 to roughly $1.5 billion in 2025 to a projected $3 billion in 2026. That’s growing at roughly 100% annually on a high-margin revenue stream. If the trajectory holds, ad revenue becomes a meaningful piece of Netflix’s profit by 2027-2028. The risk: Netflix is competing for ad dollars against Amazon Prime Video (130 million ad-supported monthly viewers in the US alone), Disney’s combined ad operation across Disney+ and Hulu, and connected TV inventory generally. Pricing power on ad CPMs is less established than on subscriptions.

Live sports rights inflation is the swing variable. Netflix has been disciplined about not buying full-season league rights, which is what’s bankrupted other media companies. But the events-over-seasons strategy still requires Netflix to keep landing tentpole rights as competitors bid them up. The next major test is the NFL — Netflix has signaled interest in a Sunday package, and the league’s next broadcast deal could open negotiations this year. A multibillion-dollar NFL Sunday package would change Netflix’s content cost structure materially.

The hidden subscriber count makes diligence harder. With Netflix no longer disclosing subscriber counts, investors have to rely on third-party estimates from Ampere Analysis and similar firms, plus Netflix’s “milestone” announcements when they cross significant thresholds. This is a real reduction in transparency, and it should be priced as such. Apple stopped reporting iPhone unit sales in 2018; the stock has performed extraordinarily well since, but the period between 2018 and 2020 saw repeated questions about whether Apple’s growth was real or financial-engineering-driven. Netflix is entering the same disclosure-opacity zone now.

What this means for advertisers

For advertisers, Netflix’s transformation creates one of the most significant new connected TV inventories in the market.

The audience composition is genuinely different from cable. Netflix’s ad tier now has more 18-34 year-old viewers than any US broadcast or cable network. This is exactly the demographic advertisers have been losing access to as cable declined. Netflix’s combination of premium content environment, non-skippable formats, high completion rates, and significant 18-34 reach is a genuine new offering, not a like-for-like replacement for cable.

CPMs are negotiable. Netflix’s stated CPM range of $30-50 reflects the platform’s premium positioning, but in practice advertisers are negotiating below those rates. As inventory grows (Netflix’s ad load remains light at 4-5 minutes per hour) and as more ad markets come online, expect Netflix to lean toward volume over premium pricing through 2026-2027.

Programmatic access is opening up. Netflix’s transition to in-house ad tech, completed across all 12 ad markets by Q2 2025, means programmatic buying through The Trade Desk, Amazon DSP, Google DV360, and Yahoo DSP is now standard. This makes Netflix accessible to a broader range of advertisers than the Microsoft-partnership era allowed.

The risks to the cable-rebuild thesis

The argument that Netflix is becoming cable has real challenges, and intellectual honesty requires naming them.

Cable’s profitability cratered. Streaming’s might not. HBO at peak generated 40% cash flow margins. Netflix is at 29.5% operating margin. The structural reason cable was so profitable was bundle economics — customers paid for hundreds of channels they never watched, and the unwatched channels still collected carriage fees. Streaming bundles are smaller and tighter. The math may not produce the same margins.

Competition is meaningfully different. HBO competed against Showtime, Cinemax, Starz — a small set of premium networks with similar models. Netflix competes against Amazon Prime Video, Disney+/Hulu, HBO Max, Paramount+, Peacock, Apple TV+, and emerging vertical-video and free ad-supported (FAST) services. The competitive dynamics are genuinely more complex.

Live sports are a margin trap. The reason cable could afford sports rights was the unique bundling math — carriage fees scaled with the entire subscriber base, not just sports viewers. Netflix has to fund sports from its general operating budget. If sports rights inflation continues at recent rates, the events-over-seasons discipline may become harder to maintain.

International growth dynamics differ. HBO’s premium model was largely a US phenomenon. Netflix’s profitability depends on continued international growth, especially in EMEA (currently 38% penetration vs. 62% in North America) and Asia-Pacific. International markets have lower ARPUs and higher content localization costs, which strain the cable-style margin thesis.

What to watch in 2026-2027

If the Netflix-as-cable thesis is right, several signals will confirm it through 2027:

- Continued ad tier dominance in new sign-ups. If the percentage of new subscribers choosing the ad tier stays above 50%, that confirms the hybrid subscription/ad-supported model is the real Netflix product.

- Additional live sports rights, particularly NFL Sunday. If Netflix lands a Sunday package, the cable-rebuild becomes undeniable.

- Bundled distribution expanding. More ISP and wireless carrier bundles indicate Netflix is comfortable with cable-style aggregated billing.

- A third price increase before 2027. Two increases in 14 months was already aggressive. A third within 12 months would signal Netflix is leaning hard into price as the primary revenue lever.

- Ad revenue growth maintaining 100%+ annual rates. If ad revenue trajectory hits $3 billion in 2026 and continues toward $5-6 billion in 2027, the hybrid model is working as projected.

Frequently asked questions

Is Netflix actually trying to become cable?

The company would never frame it that way publicly. Netflix’s marketing still emphasizes the streaming-versus-cable distinction. But the operational decisions — ad-supported tiers, live sports rights, bundled distribution, opaque subscriber metrics — are the structural elements that defined cable’s business model from 1995-2015. Whether the resemblance is intentional or emergent, the resemblance is real.

Why did Netflix really stop reporting subscriber numbers?

The company’s stated reason is that subscriber count multiplied by monthly price is “less accurate” given multiple price tiers and the extra-member feature. This is technically true but doesn’t fully explain the decision. Subscriber growth was decelerating from 41 million net adds in 2024 to 23 million in 2025 — a 44% drop. Removing the metric reduces investor focus on the deceleration. Apple’s 2018 decision to stop reporting iPhone unit sales is the closest precedent; that change came at a similar inflection point in product unit growth.

How big is Netflix’s ad business compared to cable’s ad revenue at peak?

Cable advertising in the US peaked at approximately $30 billion annually in the mid-2010s. Netflix is targeting $3 billion in 2026 and roughly $9 billion by 2028-2029. Even at the projected high end, Netflix’s ad business is materially smaller than cable’s peak — but it’s also higher-margin and addressable through more sophisticated targeting infrastructure.

Will cable disappear entirely?

No. By 2030, projected US cable penetration is roughly 55% of households (down from 88% peak). Cable retains relevance for live sports completionists, older demographics, and areas with limited broadband. But the trajectory is clear: cable’s role shrinks while streaming reproduces cable’s economic structure.

Is Netflix still a buy at current valuations?

This article doesn’t make investment recommendations. Several legitimate frameworks for valuing Netflix exist. The questions worth examining are: whether the cable-margin parallel will materialize in earnings, how aggressive Netflix can be on price increases without accelerating churn, and whether ad revenue growth holds its current trajectory. Investors should consult licensed financial professionals before making decisions.

The takeaway

Netflix didn’t kill the cable bundle. Netflix rebuilt it — premium-priced, ad-supported on the bottom tier, live-event-anchored, and now hiding the subscriber count the same way cable companies did when their numbers got embarrassing.

The endpoint of the streaming wars isn’t cord-cutting. It’s a better-margined cable bundle delivered through wifi, with software economics replacing legacy infrastructure costs. The disruptor became the disrupted’s mirror image. And the most successful streaming company in history is the one that figured out how to charge HBO prices for an HBO-style product with software margins.

That’s the story the filings tell. The press releases will continue to call it streaming.

This analysis is based on public filings, earnings releases, and industry research aggregated from Netflix’s quarterly reports, Variety, CNBC, Adweek, Wikipedia (HBO history and sports licensing), Evoca, Zippia, BroadbandSearch, MoffettNathanson research, and TD Cowen estimates as referenced throughout. For full sources and citations, see footnotebrief.com/sources.

Hamza Benarba writes Footnote Brief, a twice-weekly newsletter on what public companies’ financials actually say. Subscribe at footnotebrief.com.