The 60-second version

A $1,000 investment in Starbucks five years ago is worth roughly $1,000 today. Over the same span, the S&P 500 nearly doubled. The popular explanation, mostly imported from politics Twitter, is that “woke” killed the brand. The actual story, pulled directly from Starbucks’ own SEC filings, is operational and geographic:

- China. A company that got kicked off the Nasdaq for accounting fraud in 2020 — Luckin Coffee — quietly built a network of more than 31,000 stores by the end of 2025, roughly four times Starbucks’ China footprint. In November 2025, Starbucks sold 60% of its mainland business at a $4 billion enterprise value.

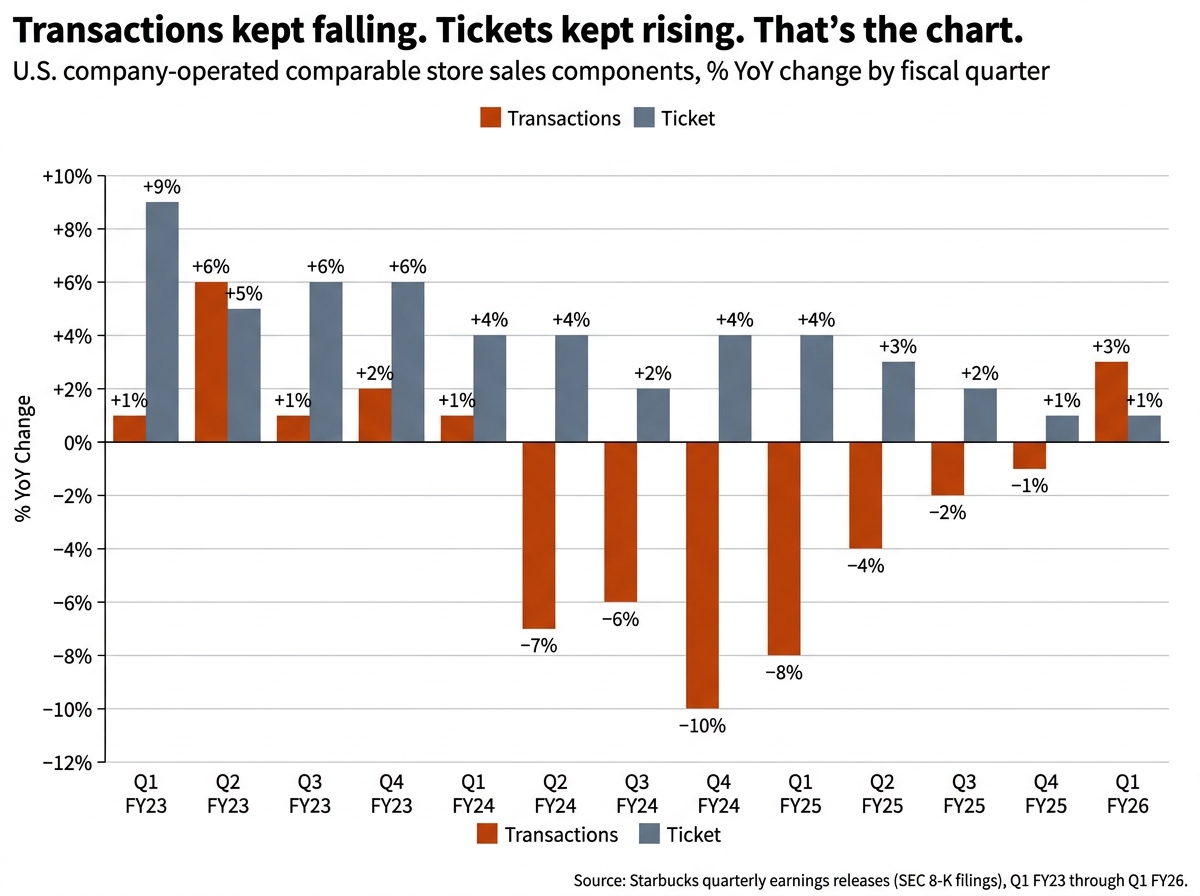

- United States. In Q4 of fiscal 2024, U.S. transactions fell 10% year-over-year while average ticket rose 4%. Translation: Starbucks raised prices on a shrinking base of regulars.

- Operations. The menu had ballooned to 170,000+ possible drink combinations on Starbucks’ own count, slowing service to a crawl.

- Middle East. A pro-Palestinian boycott — driven from the political left — pushed Starbucks’ MENA franchise to fire 2,000 workers in March 2024.

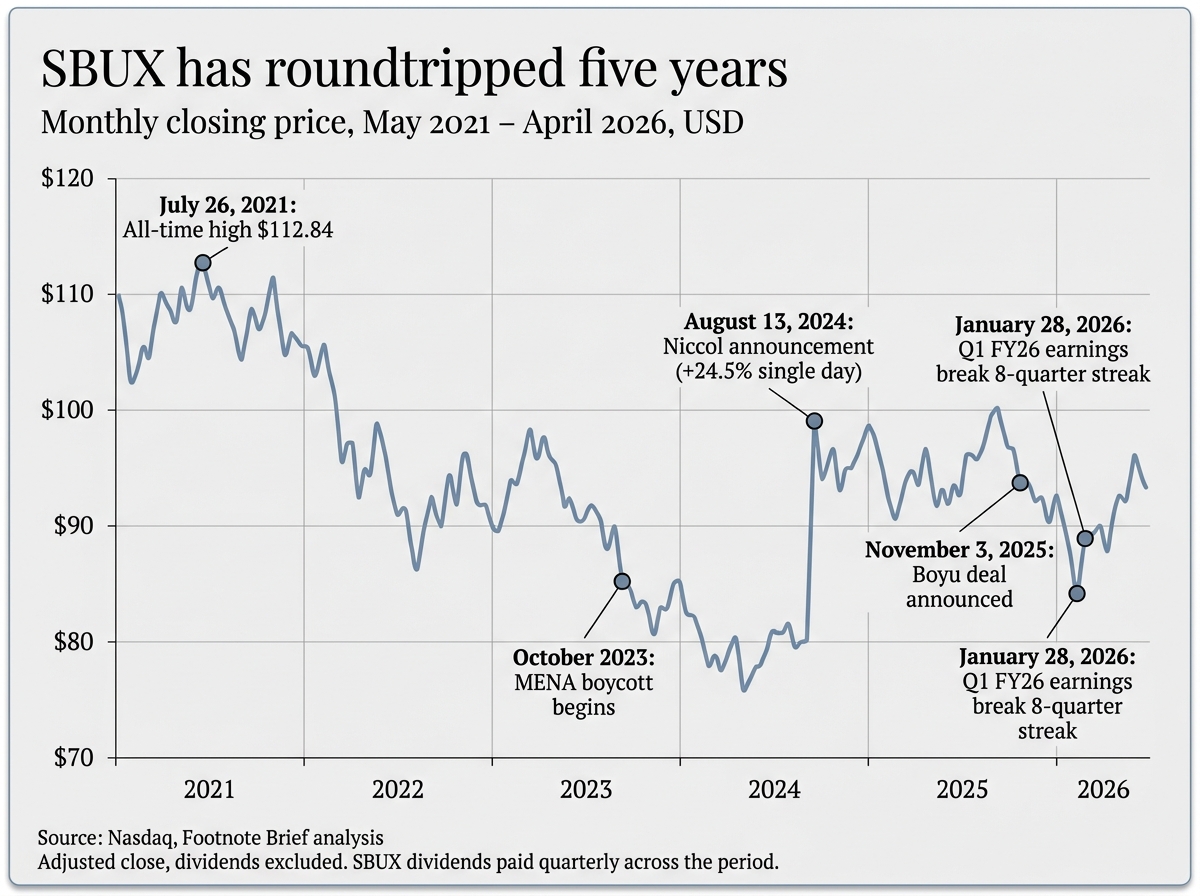

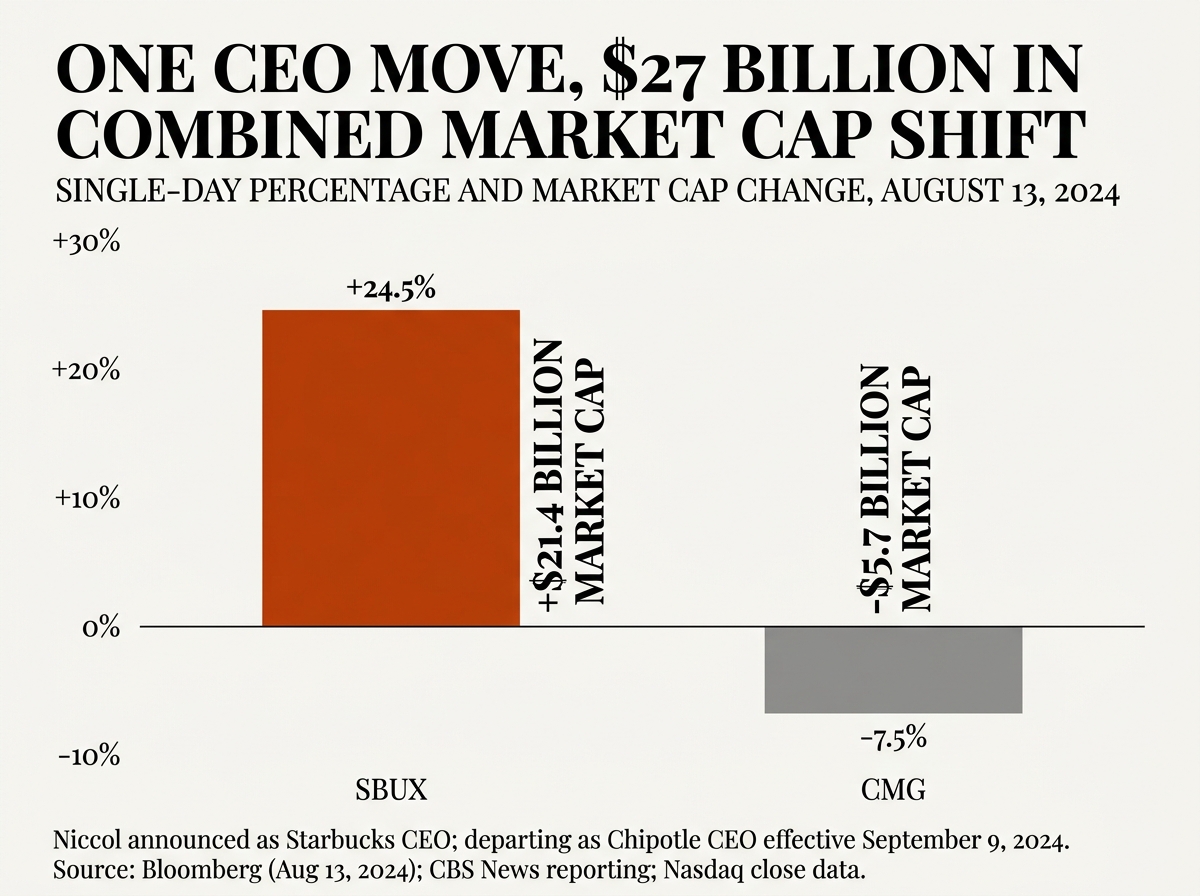

When Brian Niccol, the former Chipotle CEO, was named Starbucks chairman and CEO on August 13, 2024, the stock added $21.4 billion in market cap in a single session. Not because he promised to “fight wokeness,” but because he promised to fix the operations. By Q1 fiscal 2026 (quarter ending December 28, 2025), Starbucks broke an eight-quarter U.S. transaction-decline streak.

If “woke culture” really killed Starbucks, the cure wouldn’t look like a fast-food operator cutting 30% of the menu and selling China to a private equity firm.

Skip to the section that interests you most

The Five-Year Stock Chart Doesn’t Lie — But It Doesn’t Explain Itself

Starbucks shares hit an all-time closing high of $112.84 on July 26, 2021. As of late April 2026, SBUX trades around $97 — roughly 14% below that peak almost five years on. Over that same span, the S&P 500 has effectively doubled. Total return for SBUX over five years, dividends included, sits in the low single digits.

That’s not a Boeing or a Disney. It’s not a disaster. But it’s not the chart you’d expect from a brand that owns most of America’s coffee retail real estate, prints cash, and has paid a growing dividend every quarter since 2010.

So what happened?

The lazy answer that circulates online — that customers fled because Starbucks went “woke” — has three problems. First, the stock peaked in mid-2021, when the company’s most overtly progressive moves (the 2018 racial-bias training, the 2017 refugee hiring pledge) were already years in the rearview mirror. Second, the same American consumer who allegedly fled woke Starbucks pushed Chipotle (also liberal-leaning corporate America, also active under Niccol) to roughly a 770% gain over Niccol’s tenure there. Third, and most damning: the geographic distribution of the decline doesn’t fit the narrative.

The decline is overwhelmingly Chinese and operational. The U.S. weakness is real but secondary, and even the U.S. weakness reads as a transaction-volume problem (people coming less often, paying more per visit) — not an “I refuse to spend my money here for ideological reasons” problem.

Let’s go in order.

Luckin Coffee: How a Delisted Chinese Company Tripled Starbucks’ Store Count

Most American investors heard the name Luckin Coffee exactly once: in 2020, when the company was delisted from the Nasdaq after fabricating roughly $310 million in 2019 sales. The fraud was real. The CEO and COO were fired. The stock collapsed. Most U.S. observers wrote Luckin off as a Chinese knockoff that got caught.

That’s the last time most American investors thought about Luckin Coffee. It’s also the moment they stopped paying attention.

By the end of 2023, Luckin had 16,218 stores in mainland China. Starbucks had 6,975 — a number it had spent more than two decades building. By the end of 2024, Luckin was at 22,340 stores. By the end of 2025, per the company’s Form 6-K, Luckin operated 31,048 stores worldwide (20,234 self-operated and 10,814 partnership), the overwhelming majority of them in China. Starbucks China sat at roughly 8,000.

That’s not a competitor. That’s a takeover.

Luckin’s model is the inverse of everything Starbucks is. Starbucks is the “third place” — a sit-down environment, premium pricing, hand-crafted drinks, full-service baristas. Luckin is app-first pickup: small footprint, no seating in most locations, prices that run roughly half of Starbucks China, and an algorithmic discount engine that hands you a coupon every time you open the app. A Luckin latte runs 10–20 yuan ($1.40 to $2.75); the Starbucks equivalent in the same neighborhood is closer to 30 yuan.

Luckin doesn’t compete with Starbucks on Starbucks’ terms. It rewrote what coffee retail looks like in China. Starbucks tried to respond — store growth, mobile ordering, China-specific products — but every quarter, the China same-store-sales line in the filings showed deeper damage. In Q3 fiscal 2024, Starbucks reported a 14% decline in China comparable sales. By that point, Luckin had already passed Starbucks in both store count (in 2019) and total China revenue (in 2023).

The $4 Billion Surrender

On November 3, 2025, Starbucks announced it had agreed to sell 60% of its China retail business to Boyu Capital, a Hong Kong–based alternative investment firm, at an enterprise value of approximately $4 billion. Starbucks retained 40% and the licensing economics. The total value of the China business — including the retained stake and ongoing licensing payments — was framed by Starbucks at “more than $13 billion.” The deal closed April 2, 2026.

Read the language carefully. This is a company that, for two decades, told investors China was its most important growth market. In 2015, China was already Starbucks’ second-largest market. The 2024 strategic deck still referenced “tens of thousands” of future China stores. As recently as the FY2024 earnings call, the prior CEO was defending the corporate operating model.

Eighteen months later, Starbucks sold control. Not because China stopped being important — Boyu and Starbucks publicly target 20,000 China locations from the current ~8,000 — but because Starbucks itself could no longer execute against a local competitor that had reset the rules. The implicit admission in that filing is that the global Starbucks playbook does not work in mainland China against a digitally native, ultra-low-price local competitor. The path forward is to license the brand, take a passive minority stake, and let local operators run a Chinese coffee chain that happens to wear the Starbucks logo.

This is the single biggest reason the stock has gone nowhere. Investors had been paying for “Starbucks the global growth story.” China was the engine. China is now a 40% stake in a joint venture, with most of the operational upside accruing to a private equity firm.

In the United States: Pricing Your Regulars Out of the Cafe

The China story is the headline. The U.S. story is more uncomfortable, because Starbucks did it to itself.

Look at the Q4 fiscal 2024 release — the one that landed weeks after Niccol’s appointment, dated late October 2024:

- North America comparable store sales: −6%

- Comparable transactions: −10%

- Average ticket: +4%

That combination — transactions falling 10% while ticket rises 4% — is the chart of a brand that is pricing out its regulars and getting partially compensated by the customers who remain spending more per visit. It is, quite literally, the textbook signature of demand destruction in a premium consumer brand.

Q2 FY2024 had already shown the pattern: U.S. transactions −7%, ticket +4%. By Q4 FY2024 the gap had widened to 14 percentage points. Starbucks management spent most of 2023 and 2024 attributing the issue to macro factors — inflation pinching working-class consumers, labor strikes, weather — but the math kept telling a more brand-specific story.

The mistake was structural. Starbucks ran an aggressive multi-year price-mix strategy: bigger drinks, more add-ons, more “premium” beverage tiers (the cold-foam line, the salted-caramel innovations, eventually the olive-oil “Oleato” platform under Howard Schultz’s third stint as CEO). Each year, average ticket inched up. Each year, transactions held — until they didn’t.

A consumer who used to come in three times a week for a $4.50 latte does not, when the latte hits $6.75, simply absorb the increase. They come twice. Then once. Then they buy a Nespresso. The math is brutal for any brand that depends on frequency.

This isn’t a culture-war story. It’s a pricing-elasticity story.

The 170,000-Drink Problem

Starbucks itself, in public statements throughout 2024, used the figure of 170,000 possible drink combinations on its menu. Bloomberg’s analysis — once you account for every modifier permutation — pegged the real number closer to 383 billion. Either way, the operational implication is the same: any given customer order is a near-unique production task for the barista on shift.

I want to be careful here, because “the menu is too complicated” is one of those evergreen consultant complaints that often translates to nothing. In Starbucks’ case, the consequences are concrete and visible in the filings. Three problems compound.

First, service speed. A complex modifier order — oat milk, three pumps of sugar-free vanilla, extra espresso, light ice, half foam — takes meaningfully longer to make than a standard latte. Stack a peak-hour line of those and throughput per barista collapses.

Second, mobile ordering pile-up. The mobile app, originally designed to reduce in-store wait times, became a dumping ground for the most complex customizations. Baristas describe the morning rush as drowning in the printer feed. Customers waiting in person stare at coffees being made for people who aren’t even in the building. Niccol himself, in his first letter to shareholders, called out mobile order and pay as a system that had begun overwhelming partners during peak hours.

Third, labor cost per drink. Starbucks’ margin compression isn’t just commodity inputs — it’s the rising number of barista-minutes baked into each transaction. The company’s operating margins fell from low double-digits historically to around 9% in Q1 FY2026.

Niccol’s response, announced on the Q1 FY2025 earnings call in January 2025: a planned 30% reduction in beverage and food SKUs by the end of fiscal 2025. The first round in February 2025 cut 13 specific drinks, including most of the Frappuccino lineup. Olive-oil Oleato was killed in October 2024, less than a year after national rollout. The company also stopped charging extra for non-dairy milk in North America and paused price increases at company-operated stores through at least fiscal 2025.

This is what an operational fix looks like. It is the opposite of a culture-war pivot. None of these moves had anything to do with reversing a political stance.

The Middle East Boycott — From the Left

Of all the threads in this story, this is the one most misunderstood by people who haven’t read the actual reporting.

Starting in late 2023, Starbucks faced a pro-Palestinian boycott across the Middle East and North Africa. The trigger: an October 2023 lawsuit Starbucks filed against Workers United — its U.S. union, which had organized employees at roughly 370 American stores — over a pro-Palestinian post made on the union’s social media account in the days after October 7. Starbucks asked a court to force the union to stop using the Starbucks name and likeness. The lawsuit was widely interpreted across MENA as Starbucks distancing itself from Palestinian solidarity.

The interpretation, fair or not, traveled fast. Across the region, Starbucks became a target. The Kuwait-based Alshaya Group, which holds the Starbucks franchise across Bahrain, Egypt, Jordan, Kuwait, Lebanon, Morocco, Oman, Qatar, Saudi Arabia, Turkey, and the UAE — about 1,900 stores employing more than 19,000 staff — saw traffic collapse over the winter of 2023–24.

On March 5, 2024, Alshaya confirmed it was firing approximately 2,000 workers across its MENA Starbucks operations, citing “continually challenging trading conditions” — a phrase that, in plain English, meant the boycott was real and the franchise needed to shrink to survive. The 2,000 layoffs represented just over 10% of the regional Starbucks workforce.

Here’s where the right-wing “woke killed Starbucks” narrative completely breaks down: the boycott that materially damaged Starbucks’ international franchise came from the political left. It came from consumers who believed Starbucks was insufficiently supportive of Palestinians, not consumers who believed it was too progressive. It cost real jobs in real places. It is documented in news archives, in franchisee statements, and in subsequent SEC filings — not in conjecture.

If your story about Starbucks is “the woke mob ruined them,” and the largest documented ideological boycott against the company came from the opposite political direction, your story doesn’t survive contact with the data.

Why the Burrito Executive Got a $21.4 Billion Welcome

On Tuesday, August 13, 2024, Starbucks announced that Brian Niccol — Chipotle’s CEO since 2018 and the architect of one of the most dramatic restaurant turnarounds of the past decade — would replace Laxman Narasimhan as Starbucks’ chairman and CEO, effective September 9.

The market reaction was the largest single-day market cap gain in Starbucks’ history. The stock surged roughly 24.5%, adding $21.4 billion in market value. Chipotle, on the other side of the trade, lost about $5.7 billion. One CEO transfer — between an espresso chain and a burrito chain — moved more than $27 billion in combined enterprise value in a single session.

That is not a market reacting to a culture-war repositioning. The press release didn’t mention Palestine, didn’t mention diversity initiatives, didn’t mention any social or political stance. What it mentioned was: Niccol had grown Chipotle’s revenue by roughly 100% and profits by nearly 800% over six and a half years. He had engineered a turnaround at a brand that, in 2018, was reeling from an E. coli outbreak. He had a documented track record of operational excellence — fixing throughput, simplifying menus, cleaning up store experience, improving the in-store labor model.

That’s what investors paid $21.4 billion to buy in a single day. Operations.

The other tell is what the Chipotle stock did on the same day: it fell 7.5%. Markets weren’t valuing some imaginary “culture turnaround.” They were valuing the man who had specifically been good at running large quick-service-restaurant networks, and they were marking down the company that no longer had him.

The Eight-Quarter Streak Breaks

On January 28, 2026, Starbucks reported Q1 fiscal 2026 results. The headline numbers from the company’s own 8-K:

- Global comparable store sales: +4% (transactions +3%, ticket +1%)

- North America and U.S. comparable sales: +4% (transactions +3%, ticket +1%)

- China comparable sales: +7%

- Consolidated revenue: $9.9 billion, up 6% year-over-year

- “First U.S. comparable transaction growth in eight quarters”

That last line is the one that matters. Starbucks had not posted a positive U.S. transaction quarter since fiscal Q1 2024. Eight quarters — two full years — of declining footfall. The streak broke on Niccol’s watch, in the quarter ending December 28, 2025, roughly 16 months after he started.

I want to be honest about what this is and isn’t. One quarter is not a turnaround. EPS in that same quarter fell 19% year-over-year. Operating margins compressed to around 9%, well below the company’s historical low double-digits. The “Back to Starbucks” plan is expensive — more labor in stores, paused price increases in North America, free non-dairy milk, the SKU cuts — and the cost flows through the P&L before the revenue does. Niccol himself, on the call, framed the result as the strategy being “ahead of schedule,” not as the work being finished.

But the direction changed. Comparable transactions — the cleanest signal in the entire restaurant industry, the question of whether you actually attracted more customers this quarter than last — turned positive in both the U.S. and globally. China posted +7% comp sales in the quarter immediately before the Boyu deal closed. The eight-quarter streak is over.

For a stock that had been priced for terminal decline since 2021, the read-through is significant. The bull case isn’t “Starbucks is back to growth.” It’s “Starbucks isn’t dying.”

What This Actually Means for the SBUX Investment Thesis

Step back from the noise.

If you go to the SEC EDGAR site, pull up every Starbucks 10-K and earnings release from 2021 through Q1 FY2026, and read them in chronological order, the story that emerges has nothing to do with American culture wars. It is, in order:

- A Chinese competitor whose model Starbucks could not match.

- A pricing strategy in the U.S. that shrank the customer base.

- An operational complexity problem (menus, mobile ordering) that broke unit-level throughput.

- A regional boycott in MENA that came from the political left.

- A leadership change priced at $21.4 billion in a single day, justified explicitly by operational expertise.

- Eight quarters of declining U.S. transactions, broken in the quarter ending December 28, 2025.

None of those six items, in any priority order, requires a culture-war frame to explain. The “woke killed Starbucks” narrative isn’t so much wrong as it is missing the point. Starbucks lost half a decade of stock performance because it lost China to a delisted-and-resurrected local competitor, mismanaged its U.S. pricing, drowned its baristas in menu complexity, and got caught in a cross-fire it didn’t see coming in MENA. The leadership response — selling control of China, simplifying menus, freezing North American prices, cutting upcharges, hiring an operations specialist — is a direct response to those operational problems, not to any political ones.

For the investor, the implication is straightforward. If your thesis on SBUX is “the cultural backlash will reverse and the brand will return to glory,” the data does not support that thesis. There is no documented cultural backlash of meaningful financial significance from the political right; the documented boycott of meaningful significance is from the political left, regional in scope, and tied to a specific lawsuit. If your thesis is “an operational turnaround under a proven CEO will restore unit-level economics in the U.S. and reset the China business as a licensing engine rather than an operating one,” the early data — one quarter of positive U.S. transactions, a $4 billion deal with a clear capital-allocation story, a structural menu reset — supports the thesis directionally.

That’s not the same as being a buy. The valuation question — a forward P/E around 26x at $97, with EPS still under pressure as the turnaround spend hits the income statement — is its own debate, and one I’ll get into in a separate piece. But the story you should be using to debate it is the one in the filings, not the one on cable news.

The numbers were never about politics. They were about Luckin, ticket inflation, 170,000 drink combinations, a misjudged lawsuit, and an operational debt that compounded faster than management could pay it down.

The cure is what cures any operational debt: a leader who can execute, a simplified menu, a sane price book, and the discipline to walk away from markets you can’t win. Starbucks is in the early innings of all four.

The headlines will keep blaming the wrong things. The filings will keep telling you what’s actually happening.

Frequently Asked Questions

Why has Starbucks’ stock been flat for five years?

Starbucks shares peaked at $112.84 in July 2021 and have round-tripped since, delivering roughly 1.5% total return over the five-year span while the S&P 500 nearly doubled. The decline isn’t ideological — it’s the combination of losing the China market to Luckin Coffee, a U.S. pricing strategy that drove transactions down 10% by Q4 fiscal 2024, operational complexity (a menu with 170,000+ drink combinations), and a Middle East boycott that cost the regional franchise 2,000 jobs. The “Back to Starbucks” turnaround under CEO Brian Niccol produced positive U.S. comparable transactions for the first time in eight quarters in Q1 fiscal 2026.

Did “woke culture” kill Starbucks?

No, and the data points the opposite direction. The most financially significant ideological boycott against Starbucks came from the political left, not the right — the pro-Palestinian boycott across the Middle East and North Africa that pushed franchisee Alshaya Group to lay off 2,000 workers in March 2024. The U.S. weakness is best explained by pricing elasticity: a 4% increase in average ticket alongside a 10% decline in transactions in Q4 fiscal 2024 is the textbook signature of a brand pricing out its regulars, not of consumers boycotting on political grounds.

Who is Brian Niccol and why did Starbucks hire him?

Brian Niccol was the CEO of Chipotle from March 2018 to August 2024 and engineered one of the most successful restaurant turnarounds of the past decade — Chipotle’s stock rose roughly 770% during his tenure, and revenue roughly doubled. Starbucks announced his appointment as chairman and CEO on August 13, 2024, and the stock added $21.4 billion in market cap in a single session, its largest one-day gain ever. He was hired explicitly for operational expertise: simplifying menus, fixing throughput, and improving the in-store experience — not for any cultural or political repositioning.

What is Luckin Coffee and how did it beat Starbucks in China?

Luckin Coffee is a Chinese coffee chain founded in 2017 that was delisted from the Nasdaq in 2020 after a $310 million accounting fraud was uncovered. It rebuilt under new management with a digital-first, ultra-low-price model — most stores are small pickup-only locations where drinks cost roughly half the Starbucks China price. By the end of 2025, Luckin operated 31,048 stores worldwide compared to Starbucks’ roughly 8,000 in mainland China. Luckin had already passed Starbucks in China store count in 2019 and in China revenue in 2023.

Why is Starbucks selling 60% of its China business?

On November 3, 2025, Starbucks announced it would sell a 60% stake in its China retail operations to private equity firm Boyu Capital at an enterprise value of approximately $4 billion; the deal closed April 2, 2026. Starbucks retained 40% and ongoing licensing economics, valuing the total business at more than $13 billion. The move acknowledges that the corporate operating model could not compete with Luckin and other local chains — going forward, Starbucks China runs as a licensed brand under local operators, with a stated target of 20,000 stores up from the current ~8,000.

What caused the Starbucks boycott in the Middle East?

The boycott began in late 2023 after Starbucks filed a lawsuit in October 2023 against its U.S. union, Workers United, over a pro-Palestinian post on the union’s social media account. The lawsuit was widely interpreted across the Middle East and North Africa as Starbucks distancing itself from Palestinian solidarity, triggering consumer protests across the region. By March 5, 2024, Kuwait-based franchisee Alshaya Group confirmed it was firing approximately 2,000 workers — over 10% of its regional Starbucks staff — citing “continually challenging trading conditions.”

Is the Starbucks turnaround working?

Early signals are directionally positive but incomplete. Q1 fiscal 2026 (the quarter ending December 28, 2025) delivered the first positive U.S. comparable transactions in eight quarters, with global comparable sales up 4% and China comparable sales up 7%. However, EPS in the same quarter fell 19% year-over-year and operating margins compressed to roughly 9% as turnaround spending hits the income statement. One quarter of traffic recovery is a direction, not a conclusion.

Is Starbucks stock a buy in 2026?

That depends on which thesis the filings support. The “cultural backlash will reverse” thesis isn’t supported by the data — the documented financial damage came from operational missteps and a regional boycott from the political left. The “operational turnaround under a proven CEO will restore unit economics” thesis is directionally supported by Q1 fiscal 2026 results, but valuation (a forward P/E in the mid-20s with EPS still under pressure as turnaround spend flows through) is its own debate. This article is reporting on what the filings show — not investment advice. Read the 10-Ks and decide for yourself.

Footnote Brief reads public companies’ filings so you don’t have to. Twice-weekly breakdowns at footnotebrief.com.

Sources: Starbucks Q4 FY2024, Q1 FY2025, Q4 FY2025, Q1 FY2026 earnings releases (SEC); Starbucks Form 8-K, Nov. 3, 2025 (Boyu joint venture); Starbucks Form 8-K, April 2, 2026 (JV closing); Luckin Coffee Form 6-K, FY2025; Bloomberg (Aug. 13, 2024; Nov. 3, 2025); Reuters / CNBC / CNN MENA layoff reporting (March 5–6, 2024); Restaurant Business; CBS News; Macrotrends.Partager