The 60-second version

For three years, Temu and Shein looked like a magic trick. Two-dollar earbuds. Three-dollar dresses. Free shipping from Guangzhou in under a week. Most people assumed it was just cheap Chinese factories and aggressive pricing. It wasn’t. Both companies built their U.S. businesses around the same 1930s tariff exemption — a customs rule called de minimis that let any package under $800 enter the United States duty-free and with minimal customs inspection.

The numbers, pulled directly from White House fact sheets, executive orders, and Sensor Tower data:

- De minimis volume. The U.S. processed 134 million de minimis shipments in 2015. By 2024, it was 1.36 billion. By June 2025 (FY25 to date), it had hit 309 million in nine months alone.

- Trump killed it. Executive Order 14256 (signed April 2, 2025) ended de minimis for China and Hong Kong on May 2, 2025. EO 14324 (July 30, 2025) suspended it globally on August 29, 2025. The One Big Beautiful Bill Act repealed the underlying statute permanently, effective July 1, 2027.

- The market response was instant. Sensor Tower reported Temu’s U.S. daily active users fell 52% in May vs. March; Shein’s fell 25%.

- Temu’s ad pullback was nuclear. Temu was running 8,900 active Meta ads in January 2024. By mid-April 2025, that number had dropped to four. Google Shopping ad impression share went from ~20% to zero in three days.

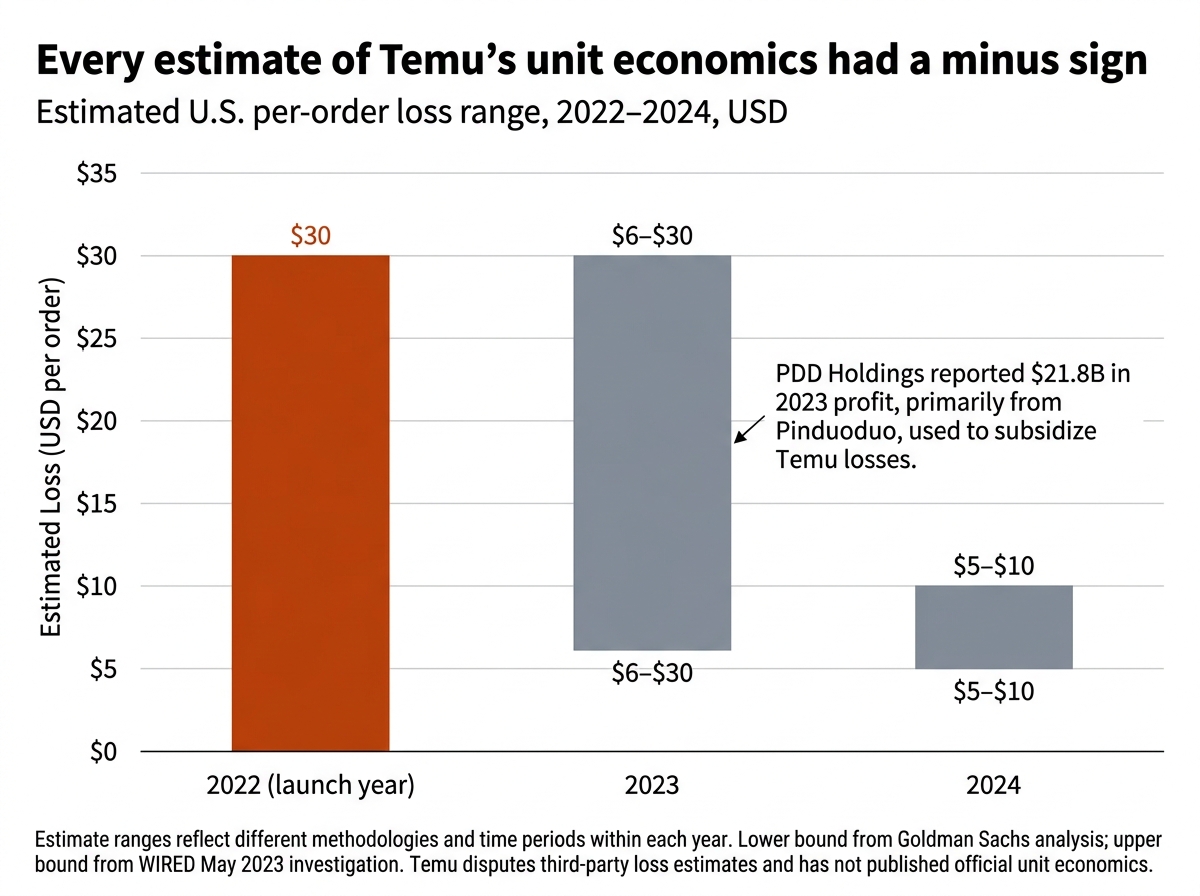

- The model was already losing money. Goldman Sachs estimated Temu was losing $6-7 per U.S. order in 2023; an earlier WIRED analysis put the figure as high as $30 per order in mid-2023. Annual losses were estimated at $588 million to $954 million.

If your story about Temu and Shein is “ruthless Chinese efficiency disrupting American retail,” the filings say something else. Both companies built their growth on a tariff exemption written before the modern global supply chain existed, and neither had a profitable unit economic model when that exemption disappeared.

Skip to the section that interests you most

The 1930 Rule That Built a $50 Billion Business

Section 321 of the Tariff Act of 1930 was written for a different world. Its purpose was administrative: U.S. Customs spent more processing tiny packages — birthday gifts, magazine subscriptions, hobbyist parts — than it collected in duties on them. The economic logic was simple. Below a certain dollar threshold, the cost of inspecting and taxing each shipment exceeded the revenue gained.

The threshold drifted upward over the decades. It was $200 for most of the late 20th century. In 2016, Congress raised it to $800 — the highest de minimis threshold of any major economy in the world. China’s threshold, by comparison, sits at roughly RMB 50 (~$7). The EU’s was €22 (~$23) until reform proposals advanced in 2025.

The number that matters is the volume change. According to a White House fact sheet from July 2025, the U.S. processed 134 million de minimis shipments in 2015. By 2024, that number was 1.36 billion — a 10x increase in nine years. CBP was processing more than 4 million de minimis packages per day. By the first three quarters of fiscal 2025, the volume had hit 309 million packages, up from 115 million in all of fiscal 2024 — a 168% acceleration.

That growth was not random. It was Temu and Shein.

According to a House Select Committee on the CCP report cited by TIME, roughly 30% of all small packages entering the United States in 2023 came from those two companies. Both built their entire U.S. distribution model on the assumption that every individual customer order would slip under the $800 threshold and arrive in the U.S. as a tax-free de minimis shipment. A Chinese factory in Guangdong shipped directly to a customer in Ohio, and the package paid no tariff on the way in.

The cost advantage was not a few percentage points. Tariffs on the relevant product categories — apparel, footwear, consumer electronics, household goods — typically ran 7.5% to 25% before any of the Trump-era reciprocal duties. A U.S. retailer importing the same products in bulk paid those duties at the port. Temu and Shein didn’t. Stacked across millions of packages a day, the gap was structural, not marginal.

This is what allowed a $3 dress and a $2 earbud to exist. Not “Chinese efficiency.” Not “scale.” A 1930 customs rule that was never written to handle 1.4 billion individual consumer parcels a year.

Temu’s Real Business Model: Lose Money, Capture Users, Sort It Out Later

Now layer on the second mechanic, because the de minimis story is only half of why these prices were so low. The other half is that Temu was deliberately, structurally unprofitable.

The numbers vary by source, and the article’s transparency depends on you knowing that. WIRED’s May 2023 investigation, the most aggressive estimate, put Temu’s loss at roughly $30 per U.S. order during its first year of explosive growth — implying $588 million to $954 million in annual losses. By 2023, Goldman Sachs estimated the loss had narrowed to roughly $6-7 per U.S. order as average order values rose and shipping consolidation improved. Tech Buzz China’s analysis pegged 2023 unit cost at about $32 per order, including $8-9 in logistics. The point is not which number is exactly right; the point is that every credible estimate of Temu’s per-order economics had a minus sign in front of it for the entire 2022-2024 period.

That was the strategy. Temu’s CFO David Liu was on record telling Chinese media that Temu’s focus was not profit but market development. The company was prepared to lose money for three years, the same way its sister company Pinduoduo had done in mainland China before turning profitable six years in. Parent PDD Holdings reported $34.8 billion in revenue and $21.8 billion in profit in 2023, almost all of it from the domestic Chinese Pinduoduo platform. Temu was funded by Pinduoduo’s profits.

So the U.S. consumer, buying a $4.99 phone case from a Guangdong factory, was being subsidized twice. Once by the de minimis exemption, which let the package arrive with no duty. And once by PDD Holdings, which was eating a per-order loss to acquire the customer.

Read that sentence again. Two layers of subsidy. The cheap price was not a market-clearing price. It was a customer acquisition cost being paid out of a Chinese conglomerate’s domestic profits, propped up by an American customs exemption written when “international trade” meant ships, not phones.

When either subsidy went away, the pricing model couldn’t survive on its own.

The Super Bowl Tell

If you wanted one piece of evidence that Temu’s economics were not what they appeared, look at February 2024.

In February 2023, Temu ran its first Super Bowl ad. By February 2024 — barely a year after launching in the U.S. — it ran three 30-second spots during the game, plus three more after. According to Bloomberg via The Robin Report, each prime-time spot cost $7 million in airtime. That’s $21 million in airtime alone. Add the $15 million in coupons and giveaways the company committed to in the same campaign window, and the all-in spend hits roughly $36 million for one weekend.

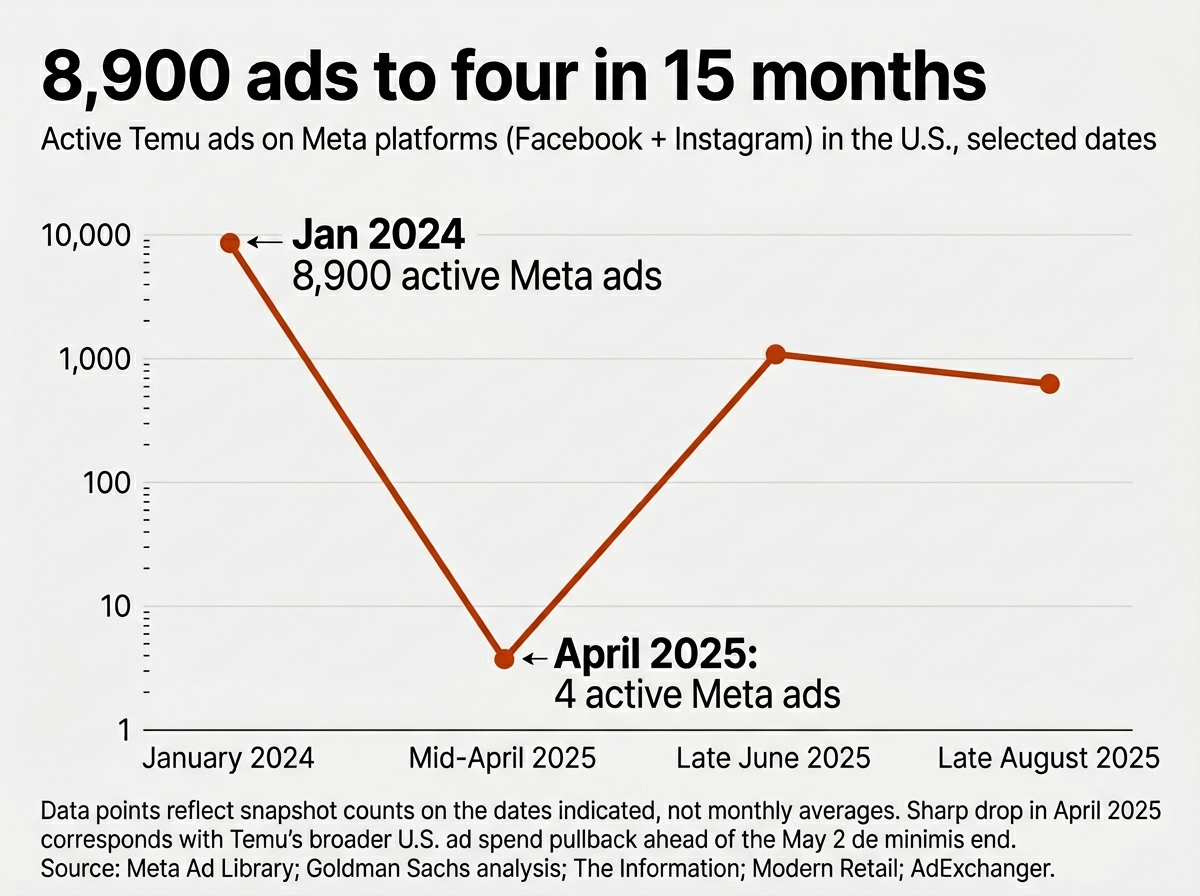

Goldman Sachs estimated Temu spent approximately $3 billion on advertising globally in 2023, with roughly $1.2 billion of that going to Meta alone. Meta’s own data showed Temu running 8,900 active ads on Facebook and Instagram in a single month — January 2024 — which made the company the second-largest advertiser on Facebook in Q4 2023, behind only Amazon. JPMorgan estimated Temu’s 2024 marketing budget at $3 billion total — roughly $250 million per month, or about $1 billion per quarter on customer acquisition.

For context: that’s not the marketing budget of a profitable retailer. That’s the marketing budget of a venture-stage company in a customer-acquisition land grab. The closest analogues are Uber circa 2015 and DoorDash circa 2018 — companies that subsidized ride and delivery prices below cost while burning through investor capital to build network effects. Both eventually had to find a profit path, and both required years of price increases and operational restructuring.

Temu’s path had a specific dependency neither Uber nor DoorDash had. Both of those companies could, in theory, raise prices to clear the market once they had captured enough customers. Temu’s pricing only worked if the de minimis exemption stayed intact, because the exemption was structural, not a function of subsidy duration. Take away the customs advantage and the floor of the pricing model goes up regardless of how much PDD Holdings is willing to keep losing.

That dependency became a problem the moment the executive orders started arriving.

The Executive Order That Broke the Model

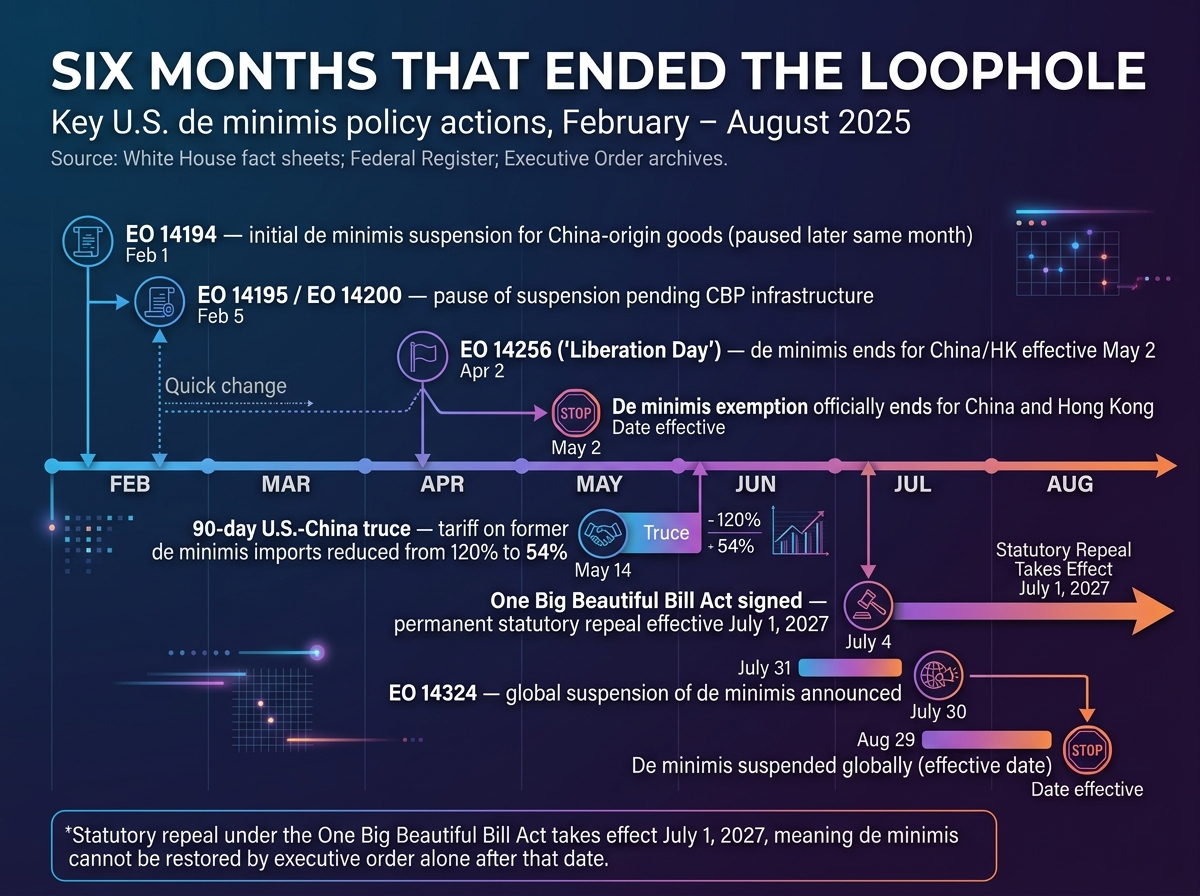

The Trump administration’s de minimis crackdown happened in three legal steps. Each one is documented in primary White House and CBP releases.

Step one — February 2025. Executive Order 14195 first paused, then re-paused, the suspension of de minimis for China — citing the lack of CBP infrastructure to actually collect duties on the volume.

Step two — April 2, 2025. Executive Order 14256 (“Liberation Day”) ended de minimis for China and Hong Kong effective May 2, 2025. Goods that previously qualified for the exemption became subject to all applicable duties, plus a separate punitive structure for postal shipments — initially set at 30% of value or $25 per item, then ratcheted up to 120% or $100 per item, then $200 per item starting June 1.

Step three — July 30, 2025. Executive Order 14324 suspended de minimis globally, effective August 29, 2025. Every country was now subject to the same rules. CBP began enforcement on the August 29 effective date.

Step four — July 4, 2025 (independent of the EOs). The One Big Beautiful Bill Act was passed and signed, repealing the statutory basis for de minimis worldwide. The repeal takes effect July 1, 2027. Even if a future administration wanted to restore the exemption by executive order, the underlying law it relied on will be gone.

For Temu and Shein, the May 2, 2025 effective date was the moment the model broke. Tariffs on former de minimis imports from China were initially 120% on postal items and up to 145% on commercial carrier shipments before being reduced to 54% under a 90-day U.S.-China trade truce in mid-May. By any of those rates, the math was unsurvivable. Tech Buzz China’s pre-crackdown research had identified roughly 50% as the tariff threshold at which Temu would lose its core price advantage. The actual tariff rates landed well above that line.

This is the economic event the script’s “Trump killed it” framing is referring to. It’s accurate as a headline. As a precise legal description, the cause of death is broader: an April executive order, an August executive order, and a July statute, working together to close every possible reopening of the loophole.

The 30 Days After May 2: The Numbers

The market reaction is documented in app intelligence data, ad transparency tools, and PDD Holdings’ own quarterly earnings.

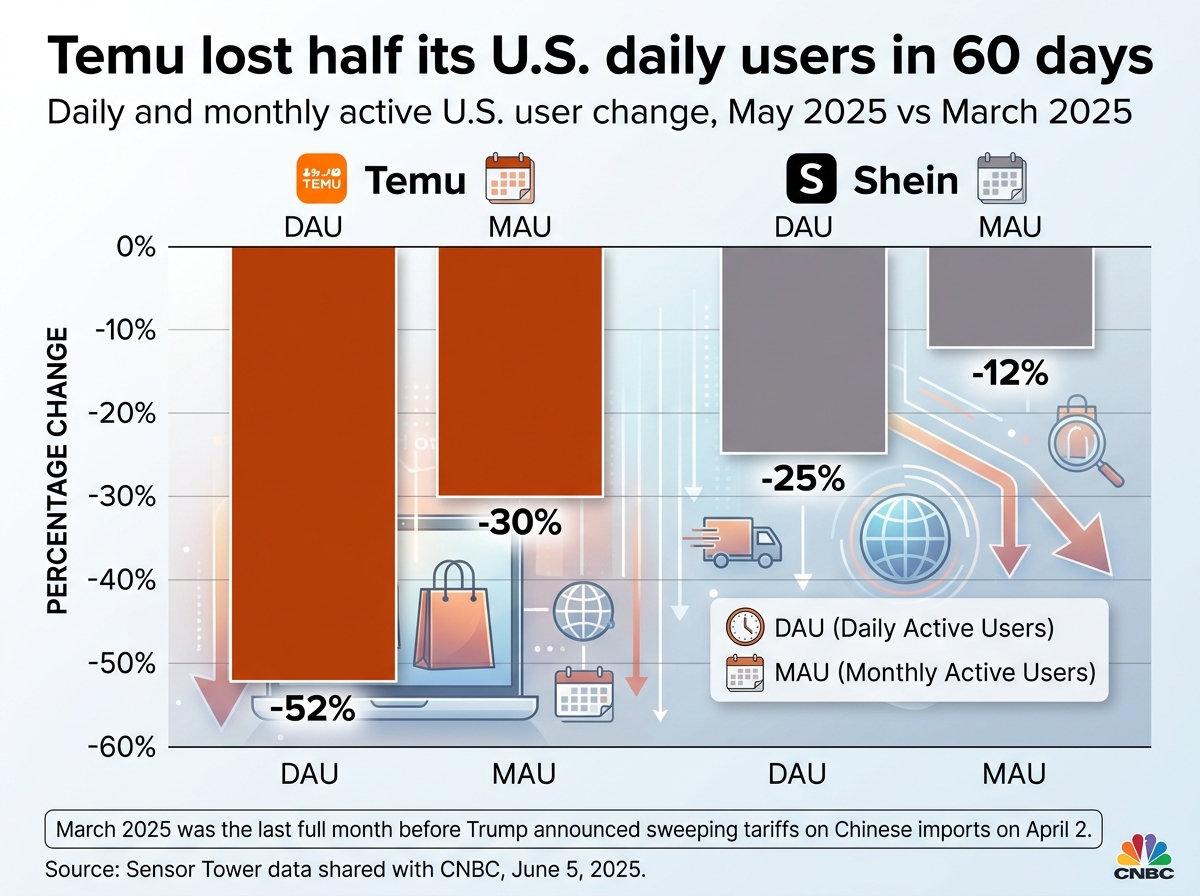

Sensor Tower, the market intelligence firm, shared the following data with CNBC in early June 2025, comparing May to March (before the tariffs were announced):

- Temu U.S. daily active users: −52%

- Shein U.S. daily active users: −25%

- Temu U.S. monthly active users: −30%

- Shein U.S. monthly active users: −12%

App Store rankings collapsed in parallel. Temu averaged a U.S. App Store rank of 132 in May 2025, down from a top-three position the year before. Shein averaged 60, down from a top-ten ranking. Both apps had lost roughly an order of magnitude in download visibility in twelve months.

The advertising pullback was, if anything, more dramatic. Working with the original primary sources rather than the secondary summaries:

- Temu’s daily Google ad placements went from 30,000–60,000 between April 6 and 9 to just 14 by April 12 (Google Ads Transparency Centre, via SCMP).

- Temu’s Google Shopping ad impression share went from approximately 20% in early April to zero by April 12 (Smarter Ecommerce analysis).

- Temu’s active Meta ads in the U.S. dropped to 4 by mid-April 2025 (The Information), down from 8,900 in January 2024 (Goldman Sachs / Meta data).

- In May 2025, Temu’s U.S. ad spend was down 95% year-over-year (Sensor Tower). Shein’s was down 70%.

That’s not a “decline.” That’s a controlled shutdown of the customer acquisition engine that had built the business. Temu publicly announced price increases starting April 25, 2025, citing “recent changes in global trade rules and tariffs.” Shein issued an effectively identical statement on the same day. Both companies began shifting away from China-direct drop-shipping toward U.S. warehouse fulfillment — a logistics overhaul that adds working capital requirements, fixed costs, and lead time, and eliminates much of the structural cost advantage that made the platforms cheap in the first place.

PDD Holdings reported Q1 2025 earnings in late May 2025 that missed analyst estimates. The company’s net income fell 47% year-over-year. CEO Lei Chen, on the call, told analysts that tariffs had “created significant pressure for our merchants, who cannot often adapt quickly and effectively.” Translation: many of the small Chinese sellers that had been Temu’s supply base couldn’t reorient to bulk shipping into U.S. warehouses fast enough, and the platform was losing supply liquidity at the same time it was losing demand.

Shein: Same Scam, Different Outcome

Most coverage treats Temu and Shein as variants of the same business. That’s roughly right — both depend on direct-from-China shipping and the de minimis exemption — but the financial profiles are meaningfully different, and the post-May 2025 data shows it.

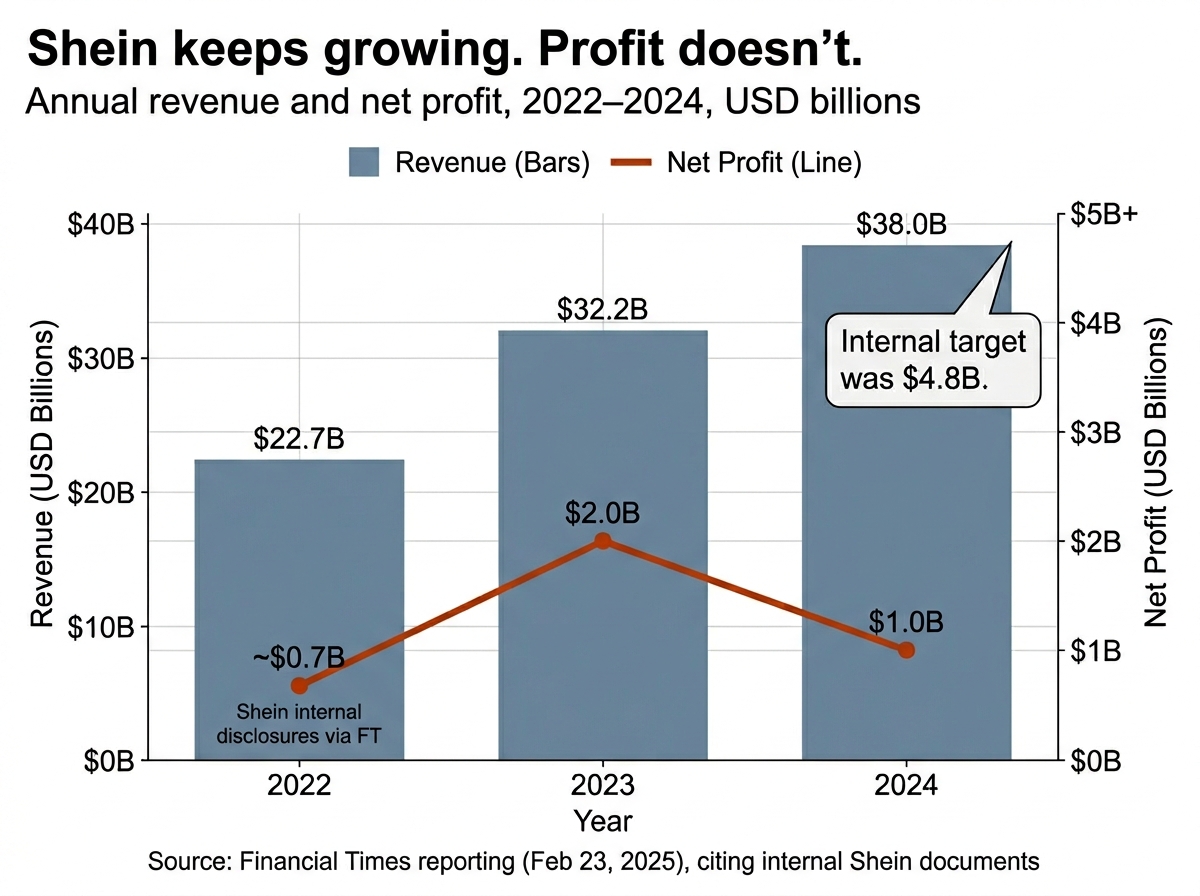

According to documents reviewed by the Financial Times in February 2025:

- Shein 2024 revenue: $38 billion, up 19% year-over-year.

- Shein 2024 net profit: ~$1 billion, down approximately 40% from $2 billion in 2023.

- Shein 2024 internal target (set in 2023): $4.8 billion in net profit, $45 billion in sales. Both targets were missed by wide margins.

Unlike Temu, Shein has been profitable for years. The business doesn’t lose money per order — its problem is margin compression as competition (mostly Temu) drives down apparel pricing and as raw material and logistics costs rise. The 40% profit decline in 2024 happened before the de minimis crackdown, suggesting the structural pressure was already there.

That said, Shein’s tariff exposure is real. The company filed confidentially for an IPO on the London Stock Exchange in 2024 at a target valuation of around $66 billion. Reuters and Bloomberg reported in 2025 that the valuation was being marked down — in some scenarios as low as $30 billion — and the IPO timeline kept slipping. The company eventually pivoted toward a Hong Kong listing, with the parent corporate structure under review for relocation back to mainland China to clear the China Securities Regulatory Commission process.

Why does the consumer behavior split — Temu down 52% on DAUs, Shein down only 25%? Three reasons.

First, product mix. Apparel — Shein’s core — has higher per-unit margin and stickier customer behavior than the commodity electronics, accessories, and household items Temu relies on. A customer who needs a specific dress for a specific event will pay more for it; a customer buying $3 USB cables can wait or substitute.

Second, unit economics. Shein had a profitable business. It can absorb tariff increases by raising prices and still keep the model intact. Temu was already losing money per order; tariffs flipped that from “subsidized growth strategy” to “unsustainable hemorrhage.”

Third, average order value. Shein’s AOV is roughly $80; Temu’s is closer to $30-50. The flat per-package postal duty ($100 to $200 per item depending on the period) is a far heavier proportional hit for Temu’s smaller-ticket orders than for Shein’s.

The result, visible in May 2025 data, is divergence. Shein has been able to keep growing per-customer spending; Temu’s daily traffic has cratered.

Europe Is Coming Next

The American story matters first because the U.S. was Temu and Shein’s largest market. But the parallel European pressure may end up structurally more important, because the EU is moving on safety as well as customs.

In February 2025, the European Commission announced that Temu and Shein would be held legally liable for unsafe products sold on their platforms — a major shift from the prior regime, which treated the platforms as mere intermediaries. The Commission’s statistic: 4.6 billion low-value items below €22 entered the EU in 2024, equal to 12 million parcels per day, 91% of them from China.

In October 2025, Belgian consumer protection group Achats — coordinating with Euroconsumers across multiple EU countries — published the results of an independent product safety investigation. The numbers are damning. Of 162 randomly purchased products tested across both platforms:

- 70% violated EU safety standards, with the majority of failures rated medium-to-high severity.

- All toys tested from Shein, and 26 of 27 from Temu, had defects including dangerous shapes, toxic substances, and small detachable parts.

- 52 of 54 USB chargers failed safety tests, with several reaching temperatures above 100°C under stress.

- One Shein necklace contained cadmium at 8,500 times the EU permitted limit.

Shein removed the flagged products quickly. Temu was slower. Both platforms are now subject to ongoing EU Consumer Protection Cooperation Network investigations. The EU is also considering closing the equivalent customs loophole (the €150 threshold) as part of its broader Customs Union Reform Package.

The European safety probe is qualitatively different from the U.S. tariff fight. Tariffs raise costs and push the model toward unprofitability. Product safety liability changes what the platforms can sell at all. A regulator who finds a Shein-listed seller’s USB charger heating to 100°C under stress can require the platform to verify compliance for every charger before listing — a level of upfront SKU-level diligence that’s incompatible with the platforms’ “list everything, take it down if reported” model.

Temu and Shein can survive higher tariffs by raising prices. They cannot survive a regulatory regime that requires every SKU to be pre-cleared by a Western standards lab, because the entire business model depends on tens of thousands of new SKUs going live every week.

What Happens to the Apps Now

The two-sided framing matters here, because the future is genuinely uncertain.

The bull case for Temu is that PDD Holdings is one of the most profitable e-commerce operators in the world, with the cash to fund a multi-year rebuild of the U.S. business under the new tariff regime. The company has begun building U.S. warehouse infrastructure and shifting toward a “half-custody” model where Chinese factories ship goods in bulk to U.S. fulfillment centers rather than parcel-by-parcel direct. By July 2025, Temu’s app downloads had recovered substantially — daily visits were up 97% month-over-month versus June, and the app had returned to top-three rankings in the U.S. App Store. Temu’s non-U.S. business is also growing fast: HSBC estimated that 90% of Temu’s 405 million global monthly active users in Q2 2025 were outside the U.S., with the swiftest growth in Europe and Latin America.

The bear case is structural. The de minimis exemption is permanently gone in the U.S. starting July 2027, and the EU is on a similar trajectory. The structural cost advantage that built both businesses is being legislated out of existence in the platforms’ two largest non-China markets. Shein’s profit fell 40% in 2024 before the new tariffs took effect; Temu was already losing $6-30 per order before a 54% tariff was added on top. The platforms can rebuild around U.S. warehouses, but doing so makes them functionally similar to Amazon Haul (Amazon’s discount product offering, launched in November 2024) — and Amazon already has the warehouses, the brand trust, the Prime members, and the Kindle/Echo/AWS ecosystem to fund losses in a way Temu can’t.

Amazon understands the threat clearly. Haul launched at sub-$20 price points specifically to compete on the categories Temu had taken, and a 2025 Omnisend survey found 28% of U.S. consumers shopping on Temu monthly versus 16% on Amazon Haul — a number that has narrowed quickly since Temu’s pricing advantage eroded.

For the reader trying to forecast whether Temu and Shein survive in the U.S. market, the cleaner framing is not “are they dying” but “what does the post-de-minimis Temu and Shein actually look like, and is that business big enough to justify the valuations they had at peak?” Shein’s IPO valuation has already been marked down from $66 billion to as low as $30 billion. PDD Holdings’ market cap is roughly half of its 2024 peak. Both companies still have valuable pieces — Shein’s apparel supply chain, Temu’s global scale outside the U.S. — but the version of these businesses that priced $2 earbuds with free shipping into Cleveland is over.

The Headline Takeaway

The story that sells on social media is “Trump tariffs killed Temu” or “Chinese e-commerce is collapsing.” Both are too simple. The accurate story is that two companies built U.S. businesses on top of a 1930 customs rule, raised the threshold to $800 in 2016, watched it scale to 1.36 billion shipments a year by 2024, and never developed a unit-economic model that worked without the exemption. When that exemption disappeared — first for China, then globally, then permanently by statute — the model didn’t slowly degrade. The customer acquisition engine got switched off in a week, daily traffic halved in 30 days, and the parent companies pivoted to U.S. warehouses with logistics and capital structures they had spent three years specifically not building.

For investors, the lesson is clean. Any business model that depends on a regulatory exemption is one regulator’s signature away from being a different business model. Uber needed cities to let it operate; DoorDash needed restaurants to accept low commissions; WeWork needed long-term leases at favorable rates. Each company’s stress test came when the regulatory or contractual structure changed. Temu and Shein’s stress test was Section 321 of the Tariff Act of 1930.

The headlines will keep blaming tariffs as if they were the asteroid. The filings will tell you the dinosaurs were already in trouble.

Frequently Asked Questions

Why is Temu so cheap?

Temu’s prices were structurally low for two reasons working together. First, the U.S. de minimis exemption (Section 321 of the Tariff Act of 1930) allowed any package valued under $800 to enter the United States duty-free. Temu shipped almost every order directly from Chinese factories to U.S. consumers, avoiding the 7.5%-25% tariffs that traditional retailers paid on bulk imports. Second, parent company PDD Holdings deliberately subsidized Temu’s per-order economics — Goldman Sachs estimated losses of $6-7 per U.S. order, while a 2023 WIRED analysis put it as high as $30 per order — to capture market share. Both subsidies are now under pressure. The de minimis exemption ended for China on May 2, 2025, and globally on August 29, 2025.

What is the de minimis loophole?

De minimis is a U.S. customs rule from Section 321 of the Tariff Act of 1930 that exempted low-value imports from duties and most customs inspection. The threshold was raised to $800 per package in 2016 — the highest in any major economy. Originally designed to streamline trivial shipments like personal gifts, the exemption was used by Chinese e-commerce platforms like Temu and Shein to ship 1.36 billion packages into the U.S. duty-free in 2024. The exemption ended for China and Hong Kong on May 2, 2025, ended globally on August 29, 2025, and is set for permanent statutory repeal on July 1, 2027 under the One Big Beautiful Bill Act.

Did Trump kill the de minimis loophole?

Yes, primarily through two executive orders. EO 14256 (signed April 2, 2025) ended de minimis for imports from China and Hong Kong, effective May 2, 2025. EO 14324 (signed July 30, 2025) suspended de minimis globally, effective August 29, 2025. Trump also signed the One Big Beautiful Bill Act in July 2025, which permanently repeals the underlying statute on July 1, 2027 — meaning even a future administration cannot restore the exemption by executive order alone.

Is Temu going out of business?

No, but the U.S. business is materially smaller and structurally different than it was at peak. Temu’s U.S. daily active users fell 52% from March to May 2025, according to Sensor Tower data shared with CNBC. The company has shifted away from China-direct drop-shipping toward U.S. warehouse fulfillment, raised prices, and cut U.S. ad spend dramatically. Parent company PDD Holdings remains highly profitable from its domestic Chinese Pinduoduo operation, which gives Temu the runway to rebuild. Outside the U.S., Temu is still growing — HSBC estimated 90% of Temu’s 405 million Q2 2025 global monthly active users were non-U.S. The business will survive; the version that priced $2 earbuds with free shipping is over.

What is Shein’s business model?

Shein is a fast-fashion e-commerce platform that designs and produces clothing in small batches based on real-time trend data, then ships directly to consumers globally. Like Temu, Shein historically relied on the U.S. de minimis exemption to ship low-value parcels duty-free. Unlike Temu, Shein has been profitable — $1 billion in net profit on $38 billion in 2024 sales, per FT reporting. The company filed confidentially for an IPO on the London Stock Exchange but has shifted toward a Hong Kong listing. Valuation expectations have fallen from $66 billion in 2023 to as low as $30 billion in 2025 reporting.

How much did Temu lose per order?

Estimates vary by source and time period. A WIRED investigation from May 2023 estimated Temu was losing approximately $30 per U.S. order during its first year. Goldman Sachs, in analysis published in 2024, estimated the loss had narrowed to roughly $6-7 per U.S. order as average order values rose and shipping costs improved. Tech Buzz China analysis pegged total per-order cost at about $32 in 2023, including $8-9 in logistics. Annual losses were estimated at $588 million to $954 million. Every credible estimate from the 2022-2024 period showed negative unit economics; Temu was deliberately unprofitable as a customer-acquisition strategy.

What’s the difference between Temu and Shein?

Both are Chinese-origin e-commerce platforms that sell low-priced goods directly to global consumers using the de minimis exemption. The differences: Shein was founded in 2008 and focuses on apparel; Temu launched in 2022 and sells everything (electronics, household goods, accessories, plus some apparel). Shein has been profitable since at least 2022; Temu has been deliberately loss-making to grow share. Shein’s average order value is roughly $80; Temu’s is $30-50. After the May 2025 de minimis crackdown, Temu’s U.S. daily active users fell 52% while Shein’s fell only 25% — Shein’s higher-margin product mix and profitable unit economics gave it more cushion to absorb tariff costs.

Will Temu prices keep rising?

Almost certainly, yes. Temu publicly announced price increases starting April 25, 2025, citing “changes in global trade rules and tariffs.” With the de minimis exemption now globally suspended and permanently repealed effective July 1, 2027, Temu can no longer avoid tariffs on individual U.S. shipments. The platform is rebuilding around U.S. warehouse fulfillment, which adds inventory carrying costs, lead time, and complexity that the China-direct model didn’t have. Combined with reduced ad spending and slower customer growth, the structural pressure on prices is upward, not downward.

Footnote Brief reads public companies’ filings so you don’t have to. Twice-weekly breakdowns at footnotebrief.com.

Sources: White House Executive Orders 14256 and 14324 (April 2 and July 30, 2025); U.S. Customs and Border Protection enforcement guidance (August 29, 2025); Section 321, Tariff Act of 1930; One Big Beautiful Bill Act (July 2025); Sensor Tower via CNBC (June 5, 2025) — Temu and Shein U.S. DAU and ad spend data; Goldman Sachs / Meta ad library data via Modern Retail (March 2024) — Temu Meta ad count and spend estimates; The Information (April 2025) — Temu Meta ads drop to four; South China Morning Post (April 16, 2025) — Google Ads Transparency Centre data; WIRED (May 2023) — Temu loss-per-order analysis; Tech Buzz China (Rui Ma) — Temu unit economics; Wall Street Journal — Goldman Sachs per-order loss estimates; PDD Holdings Q1 2025 earnings call (May 27, 2025); Financial Times (February 23, 2025) — Shein 2024 profit and revenue; Reuters — Shein IPO valuation reporting (2025); CNN / Digital Commerce 360 / The Robin Report — Temu Super Bowl ad spend (February 2024); Euroconsumers / Achats (October 30, 2025) — EU product safety investigation; European Commission / CNBC (February 5, 2025) — EC liability ruling and CPC Network probe; House Select Committee on the CCP — de minimis shipment share data; HSBC analyst note (Q2 2025) — Temu global MAU split.