A line-by-line read of Airbnb’s 2024 and 2025 financials reveals an interest-income business that doesn’t appear on the company’s cover slide. It also reveals why the next two years will look different from the last two.

The 60-second version

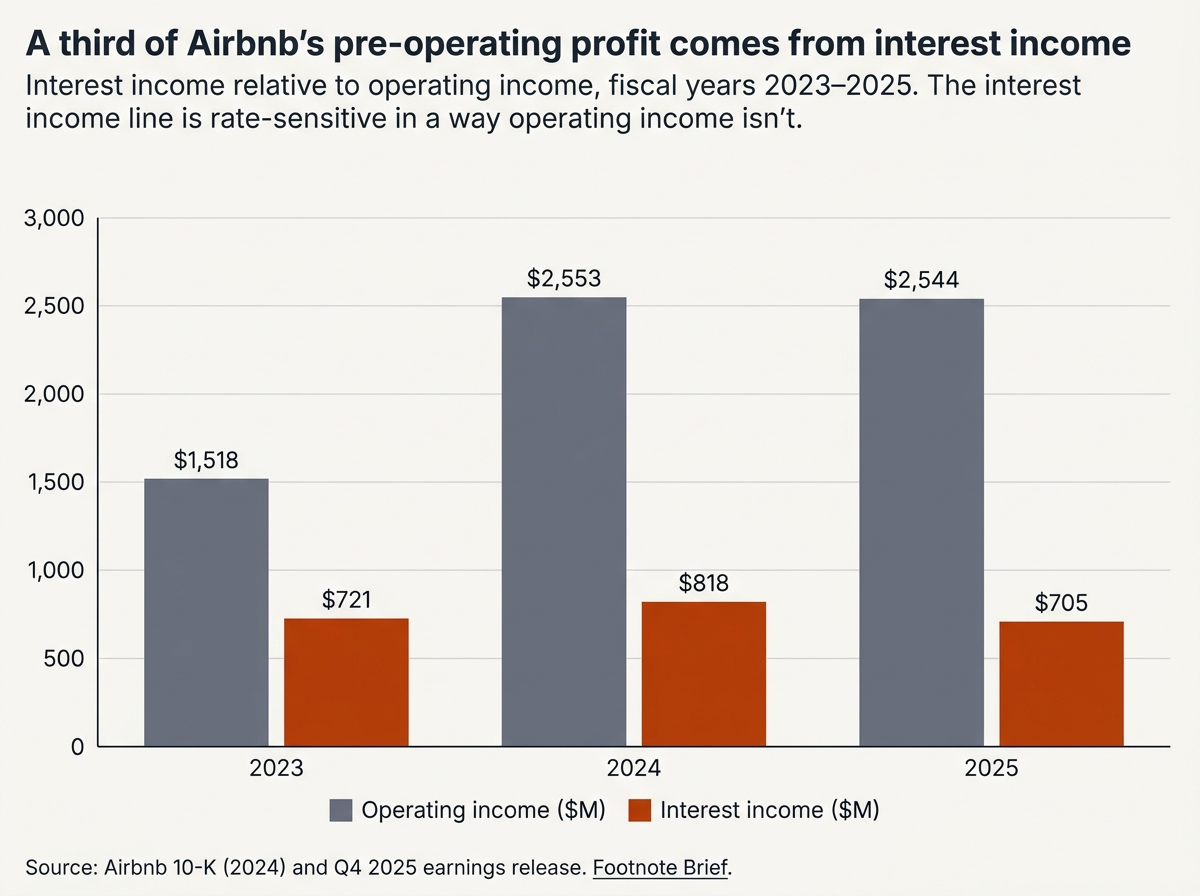

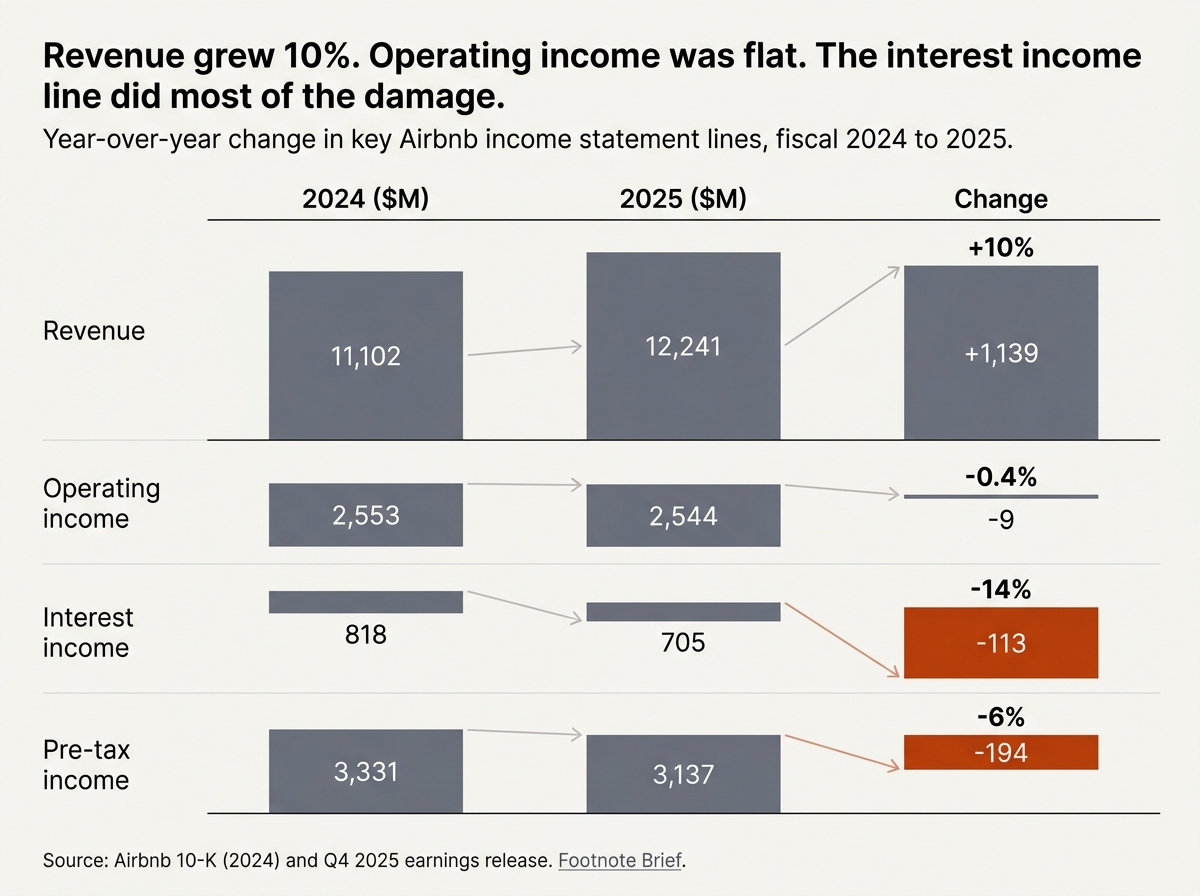

Airbnb earned $818 million in interest income in 2024 — equivalent to 32% of operating income. That money came from sitting on a combination of corporate cash and customer float averaging close to $19 billion across the year. In 2025, with the Fed funds rate down roughly 175 basis points from its 2023 peak, interest income fell to $705 million while operating income went flat at $2.5 billion despite revenue growing 10%. The contrarian point: a meaningful slice of Airbnb’s “operating leverage” since 2022 was actually monetary policy, and that subsidy is unwinding in real time. What to watch over the next two years: the interest income line on the quarterly P&L, what Airbnb does with the float duration, and whether core hosting margins can grow fast enough to offset the rate-driven drag.

Skip to the section that interests you most

How Airbnb came to sit on $11 billion of customer cash

The mechanic is buried in the 10-K but it’s not complicated. When a guest books a stay on Airbnb, the guest pays at booking. The host doesn’t get the money. Airbnb does. The host gets paid roughly 24 hours after the guest checks in, barring cancellations.

The window between “guest pays” and “host gets paid” averages several weeks for a typical booking and stretches to months for trips booked far in advance — the European summer reservations made in February, the Christmas-week trip to Aspen booked in October. Multiply that timing gap across every booking on the platform globally and Airbnb is permanently sitting on a large pool of other people’s money.

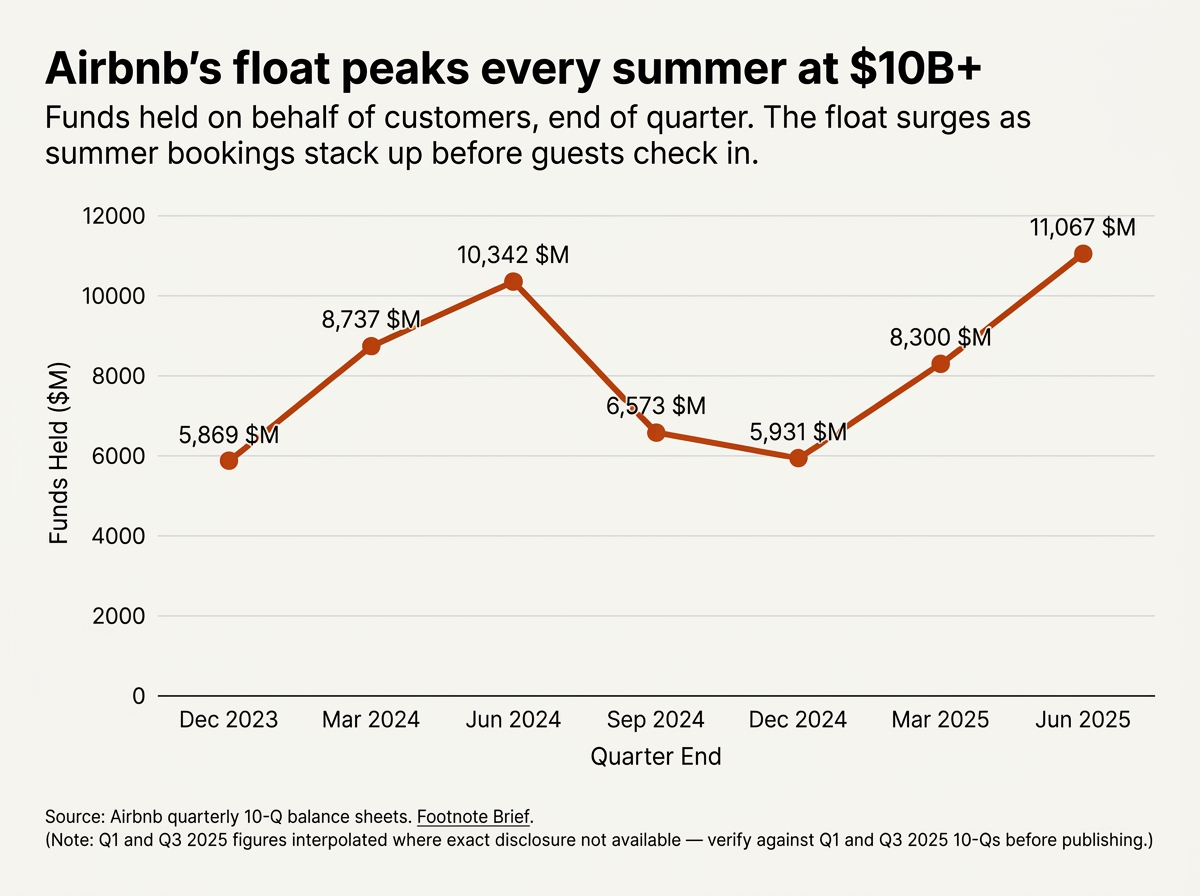

That pool appears on the balance sheet as “funds receivable and amounts held on behalf of customers.” A matching liability — “funds payable and amounts payable to customers” — appears on the other side. The balance is highly seasonal and tracks the booking calendar. It peaks in Q2 each year as summer reservations stack up, then drains through Q3 and Q4 as guests check in and hosts get paid.

The pattern is visible in the quarterly disclosures. End-of-quarter funds held on behalf of customers:

- Dec 2023: $5.9 billion

- Mar 2024: $8.7 billion

- Jun 2024: $10.3 billion (summer peak)

- Sep 2024: $6.6 billion

- Dec 2024: $5.9 billion

- Jun 2025: $11.1 billion (new summer peak)

The float is structurally growing alongside gross booking value. As Airbnb’s bookings expand, the average dollar amount the company is sitting on at any given moment grows in proportion. This is not a side effect of the marketplace. It is a direct consequence of the payment architecture Airbnb chose.

What the 10-K actually says about how Airbnb invests this money

The FY2025 10-K is unusually direct on this. The funds, per Airbnb’s own filing, are “generally held in bank deposit accounts and in money market funds.” Elsewhere the same filing notes the company holds significant amounts of “money market funds, certificates of deposit, U.S. government debt securities, commercial paper, corporate debt securities, government agency debt securities, mortgaged-backed and asset-backed securities” — both for corporate cash and “for funds held on behalf of our hosts and guests.”

That is the asset mix of a treasury operation at a regional bank. The duration is mostly short. The credit quality is high. The yield tracks short-term rates closely.

Airbnb does not disclose the average yield on these holdings or break out interest income between corporate cash and float. But the 10-K specifies that “interest earned on these funds” flows through the company’s income statement as part of consolidated interest income. There is no separate “float income” line. The full interest income figure on the P&L is the combined yield on every dollar of cash, short-term investments, and customer float the company holds at any given moment.

That combined number was $818 million in 2024 and $705 million in 2025.

The $818 million number nobody is talking about

To put $818 million in context: in 2024, Airbnb’s total revenue was $11.1 billion. Operating income was $2.55 billion. Interest income was $818 million. Pre-tax income was $3.33 billion.

Interest income, then, was equivalent to 32% of operating income and 24.6% of pre-tax income. That is not a footnote-sized number. That is a major P&L line that, in a different industry presentation, would be called out and discussed on every earnings call.

In Airbnb’s case, it isn’t. The shareholder letter highlights revenue, nights and experiences booked, gross booking value, net income, adjusted EBITDA, and free cash flow. Interest income gets a line in the table and a brief mention when explaining a quarterly net income beat or miss.

The reason this matters is that the $818 million is rate-sensitive in a way that the rest of Airbnb’s income statement isn’t. A 100 basis point change in short-term rates moves this line meaningfully — likely $150–200 million annually on a steady-state basis. That same rate move does very little to the host take rate, the marketing efficiency, the headcount, or any of the operating-level drivers analysts spend most of their time modeling.

In other words, a third of Airbnb’s pre-operating profitability has been levered to a variable that has nothing to do with how well the marketplace is running.

How interest income shows up below operating income – and why that matters for valuation

Interest income is a non-operating line. It sits below operating income on the income statement and above pre-tax income. This accounting treatment has a non-trivial implication for how Airbnb gets valued.

When analysts and the financial press cite “operating margin” or “EBIT margin” as a proxy for business quality, that figure excludes interest income entirely. Airbnb’s operating margin in 2024 was 23.0%. In 2025 it was 20.8%. By those numbers alone, the business looks like it had a margin compression year — revenue up 10%, operating profit flat.

But “net income margin” includes interest income. And on that basis, 2025 was a flat-ish year masked by the offset between rising operating income (+$0M) and falling interest income (-$113M). The all-in story tells you the float income subsidized profitability for several years. The operating margin alone tells you about the marketplace.

Both metrics are correct. They just answer different questions. The question Airbnb’s investors should be asking — and aren’t, often enough — is: how much of the multiple I’m paying assumes a continued contribution from interest income, versus a multiple on the marketplace alone?

If you back out interest income entirely and value Airbnb on operating profit alone, the implied multiple looks meaningfully higher than the consensus number. That’s not necessarily wrong. But it’s a different bet than the headline numbers suggest.

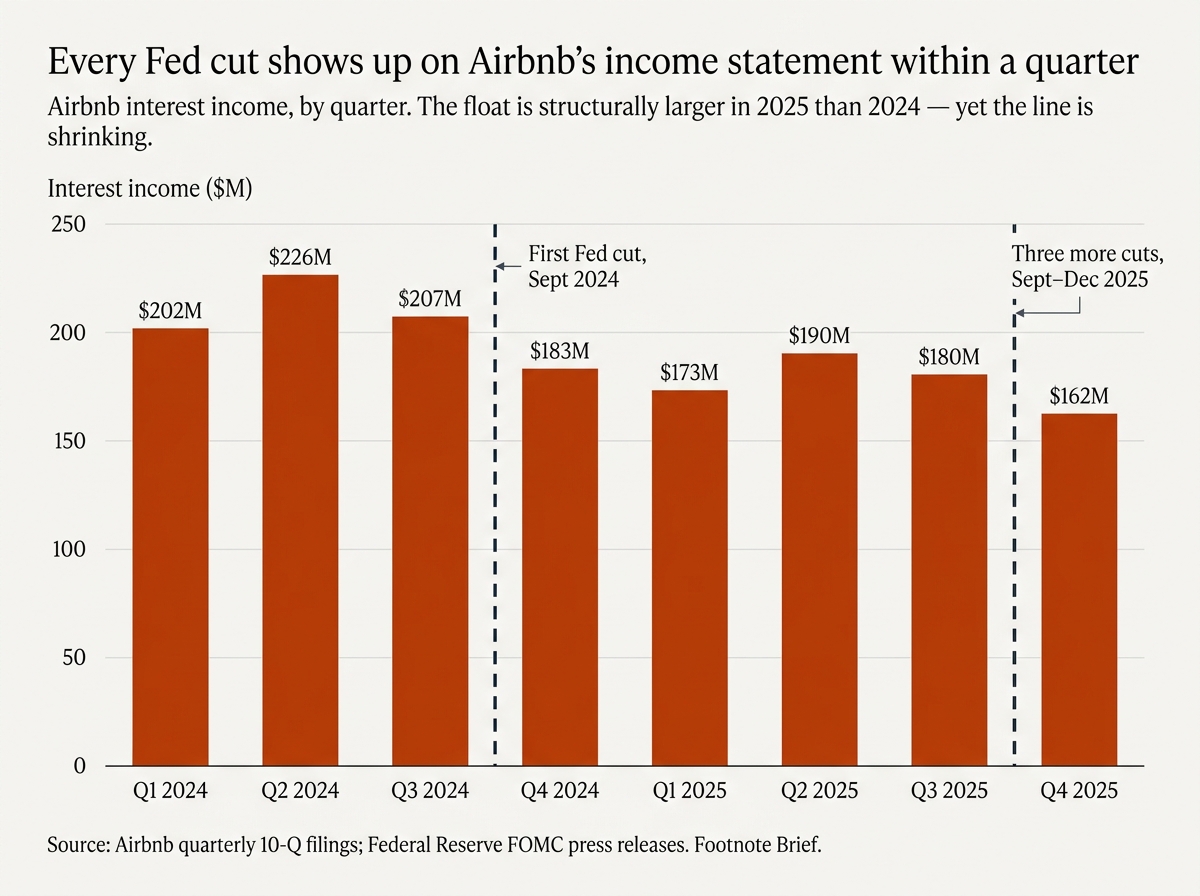

The Fed cut rates. Here’s what happened, quarter by quarter.

The Fed funds rate peaked at 5.25–5.50% in August 2023 and held there through August 2024. The first cut came in September 2024, followed by November and December cuts that took the range to 4.25–4.50% by year-end. After a long pause through summer 2025, the Fed cut three more times — September, October, December 2025 — to today’s range of 3.50–3.75%, where it has held for the past three meetings.

Roughly 175 basis points of cuts from peak. Airbnb’s quarterly interest income, in millions:

- Q1 2024: $202

- Q2 2024: $226

- Q3 2024: $207

- Q4 2024: $183

- Q1 2025: $173

- Q2 2025: $190

- Q3 2025: $180

- Q4 2025: $162

Q4 2025 interest income was 28% lower than Q2 2024 — a $64 million decline. And this happened despite the float being structurally larger. End-of-period funds held on behalf of customers were $11.1 billion at June 2025, the highest in company history. More float, less yield per dollar. The result is a falling line.

The Q4 2025 figure of $162 million annualizes to roughly $650 million if rates hold. That’s $170 million below 2024’s run rate — equivalent to nearly 7% of operating income — gone, before any further Fed action.

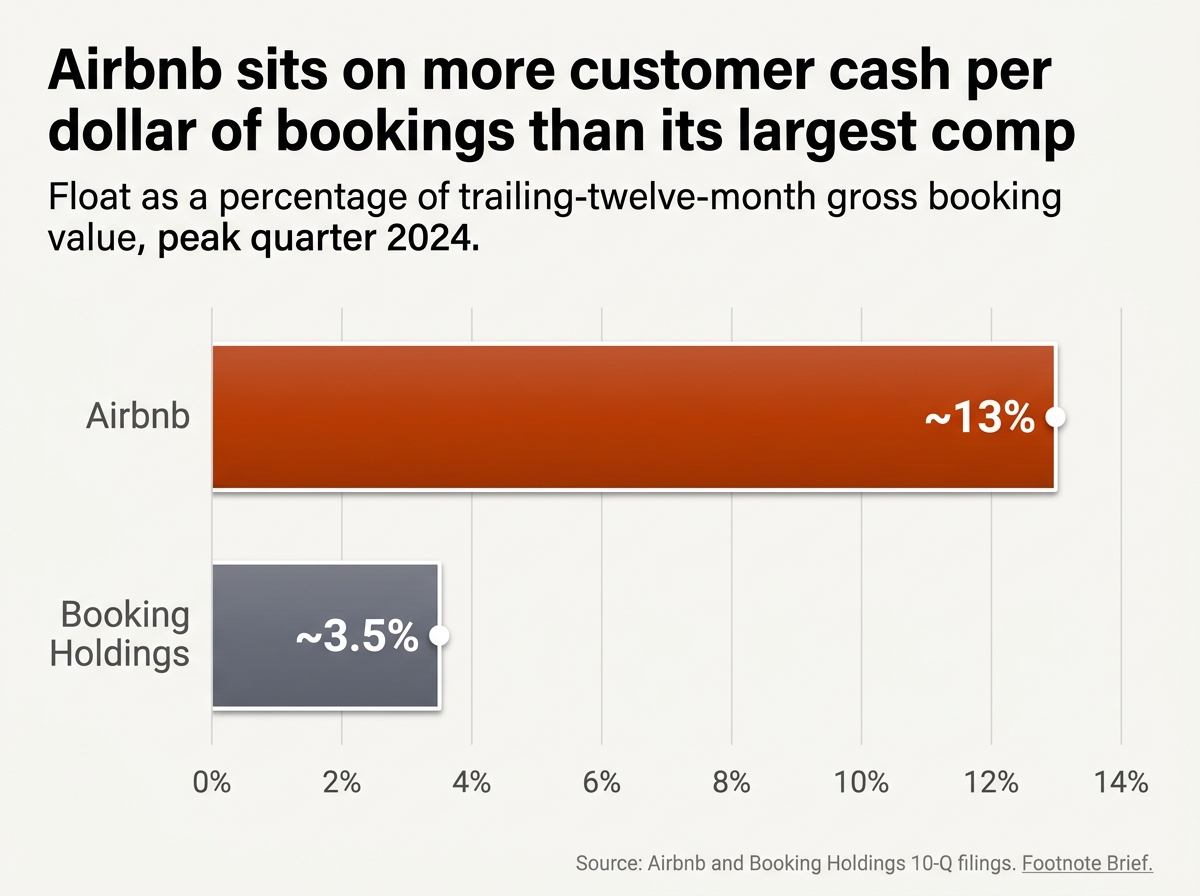

Why Airbnb is structurally more rate-sensitive than Booking Holdings

The most useful comp for Airbnb’s float economics is Booking Holdings. Both run cross-border travel marketplaces. Both have meaningful payment volume. Both report interest income.

The difference is in the payment model.

Booking Holdings runs a hybrid. A large slice of its bookings flow through the agency model, where the property collects payment from the guest directly and Booking takes a commission later. The merchant model — where Booking holds the cash like Airbnb does — is growing but is still a smaller share of total volume. The result is that Booking’s deferred merchant bookings balance is around $5–7 billion at peak quarters, despite Booking processing roughly twice the gross bookings of Airbnb.

Airbnb’s float-to-GBV ratio is therefore roughly four times higher than Booking’s. Per dollar of bookings on the platform, Airbnb sits on more cash for longer.

Two other differences matter. Booking carries meaningful long-term debt and has interest expense to offset its interest income — net interest contribution is much smaller than Airbnb’s. And Booking’s float is denominated across more currencies with more complex hedging, which dampens net yield. Airbnb runs net interest positive at scale because the company’s balance sheet is largely debt-free and its float is concentrated in dollar-denominated instruments.

The takeaway: when rates rise, Airbnb benefits more than Booking. When rates fall, Airbnb gives back more. The structural exposure is a feature of the payment architecture, and it isn’t going away unless Airbnb fundamentally changes how it pays hosts.

The PayPal comparison is cleaner than the Booking comparison

If you want to understand the rate-sensitivity of Airbnb’s float economics, the more instructive comparison isn’t Booking — it’s PayPal.

PayPal holds customer balances on its platform — the money sitting in user PayPal wallets, in transit between buyer and seller, in dispute, or otherwise unsettled. PayPal calls these “customer balances” or “funds receivable and customer accounts” depending on the disclosure. They function as float in essentially the same way Airbnb’s customer funds do. PayPal invests them in money market funds, US government securities, and similar short-duration instruments, and books the resulting yield as interest income.

PayPal is open about how rate-sensitive this line is. The company breaks out interest earned on customer balances as a distinct revenue line — “other value added services” includes it — and discusses rate impact explicitly in earnings commentary. When rates rose in 2022–2023, PayPal’s interest revenue from customer balances became a meaningful contributor to total revenue. When rates fall, the line declines.

Airbnb has the same dynamic but treats it differently in disclosure. The interest income is reported but not isolated from corporate cash interest. Investors who want to model the rate sensitivity have to do the math themselves using balance sheet line items.

This disclosure choice has practical consequences. PayPal investors price in rate sensitivity explicitly because the company highlights it. Airbnb investors largely don’t, because the company doesn’t. That gap between actual exposure and perceived exposure is part of what makes the rate-cut story underweighted in current Airbnb consensus.

If Airbnb chose to break out float-derived interest income as its own line — quarterly, with disclosure of average float balance and effective yield — analysts would price the rate sensitivity in much faster, and the stock multiple would probably contract slightly to reflect the lower-quality nature of that income. There is essentially no reason for Airbnb to make that disclosure change voluntarily. Investors are getting the lower-disclosure benefit, which is to say, they are paying for something they don’t fully see.

The honest accounting: float-derived interest vs corporate cash interest

A precise version of the rate-sensitivity argument has to acknowledge that not all of Airbnb’s $818 million of interest income comes from customer float. Airbnb runs an unusually large corporate balance sheet, at year-end 2024, the company had roughly $10.6 billion of cash, cash equivalents, and short-term investments on top of $5.9 billion of customer float. Both pools earn interest. The 10-K does not break out the split.

A reasonable estimate, using approximate average balances and similar yields, would put float-derived interest at $300–400 million of the 2024 total, with the remainder attributable to corporate cash and short-term investments. That estimate could be off by 20–30% in either direction depending on the actual mix of instruments and the seasonal pattern of float.

This split matters less than it might seem. Both pools are equally rate-sensitive. A 100 basis point cut in short-term rates hits the corporate-cash interest line about as hard as it hits the float-derived line. The “Airbnb is a bank” framing is loose; the more precise framing is “Airbnb is a company with a $19 billion combined treasury operation that earns short-term rates and is therefore highly exposed to monetary policy.”

That is a less catchy framing. It is also more accurate. Either way, the directional argument — that interest income materially augments Airbnb’s reported profitability and is now declining, holds across both pools.

What a duration extension on the float would look like

Airbnb’s current treasury policy is conservative. The 10-K describes a portfolio dominated by overnight bank deposits, money market funds, and short-duration investment-grade paper. This makes sense for the customer float — the company has a fiduciary obligation to the cash, and a host can demand payment as soon as a guest checks in. Airbnb cannot afford a liquidity mismatch on customer money.

But a portion of the corporate cash could, in principle, be held in longer-duration instruments. Two-year Treasuries currently yield meaningfully more than overnight money. If Airbnb laddered, say, $3–4 billion of its corporate cash into 1–2 year Treasuries, the company could lock in current yields for longer and reduce the rate-sensitivity of the interest income line for at least the next 18 months.

The cost is duration risk: if the Fed cuts faster than expected, longer-duration Treasuries gain in mark-to-market value but the company has committed to lower yields. If the Fed pauses or hikes, longer-duration positions lose value. Most public-company CFOs are reluctant to take meaningful duration risk on shareholder cash precisely because the downside shows up in earnings while the upside often doesn’t get credit.

There is no public indication Airbnb is considering this. But the option exists, and a more activist CFO could meaningfully change the rate-sensitivity profile of the company over a 12–18 month horizon. This is the kind of decision a real bank would make automatically and a marketplace company often doesn’t think to make at all.

What this means for the buyback program

Airbnb repurchased $3.4 billion of stock in 2024 and continued an aggressive buyback program through 2025, including a $1.0 billion repurchase in Q2 2025 alone. The buyback is funded out of free cash flow, which in 2024 came in at roughly $4.5 billion against $11.1 billion of revenue — a free cash flow margin near 40%.

A meaningful chunk of that free cash flow margin is interest income. Operating cash flow benefits dollar-for-dollar from interest received. As interest income declines, free cash flow growth decelerates even if operating cash flow holds. That decelerated free cash flow growth is what funds buybacks, dividends, or M&A.

Put differently: the rate cycle isn’t just an income statement issue for Airbnb. It compresses the cash flow available for capital return. A company running flat operating income with a declining interest income line and a $3+ billion annual buyback target eventually has to choose between drawing down cash, slowing the buyback, or finding new sources of cash flow growth.

This is a slow-burning issue, not a 2026 issue. Airbnb’s net cash position is large enough to absorb several years of mismatch. But the trajectory matters.

What consensus analyst models tend to miss

Sell-side models for Airbnb almost universally project interest income flat or growing modestly off the 2024 base. This makes sense as a default assumption — most modelers don’t have an explicit Fed rate forecast and don’t want to make one — but it’s also where the consensus models go wrong.

If you build out the model with a more granular rate path, the picture changes meaningfully. Assume the Fed funds rate averages roughly 3.50% in 2026 (consistent with the current dot plot) and Airbnb’s average earning balances grow 8% with the business. The interest income line in 2026 likely lands somewhere between $620 million and $680 million, a $130–200 million decline from the 2024 peak. That’s roughly $0.20–0.30 of per-share earnings, depending on share count assumptions, that the typical consensus model is implicitly assuming will hold flat.

The issue isn’t that the consensus is wildly wrong on Airbnb. It’s that the consensus has lazy assumptions on a line item that’s both large and rate-driven. When the rate-driven decline shows up, quarter by quarter through 2026 — the analyst notes will start adjusting downward, and the cumulative effect over a year of revisions is meaningful.

This kind of slow-grind earnings revision is rarely a thesis-breaking event for a stock. It’s more often a thesis-dragging event. The stock doesn’t crash on any single quarter; it just underperforms peers as estimates get cut. That’s a tougher pattern to trade against than a clear miss, which is part of why the float-income decline hasn’t gotten more attention.

The risks to the rate-sensitivity thesis

Three things could break the argument as written.

The Fed reverses. The current dot plot signals one cut in 2026 and one in 2027, but plots have been wrong by hundreds of basis points in either direction over the past four years. A reacceleration of inflation, driven by tariffs, energy shocks, or fiscal policy, could push the Fed back into a holding pattern at current rates or even into hikes. Under that scenario, Airbnb’s interest income line stabilizes, and the rate-sensitivity drag stops. The 2025 numbers would then look like the trough rather than the start of a multi-year decline.

Float continues to grow faster than yields fall. If Airbnb’s gross booking value grows aggressively, say, 15%+ per year through new geographies or the Services and Experiences expansion, the float can grow fast enough to partially offset the yield decline. A float growing 15% with a yield falling 10% still produces growing interest income in absolute dollars. This is the “we’re going to grow the bank faster than the rates fall” defense, and it’s not absurd. Q2 2025 float at $11.1 billion was already 7% above the prior summer peak.

Airbnb extends duration on the float. As discussed above, the company has the option to ladder a portion of its cash into longer-duration instruments and lock in current yields for 12–24 months. This wouldn’t reverse the trend but would smooth it. It’s a CFO decision, not a market event.

Operating leverage in the marketplace finally arrives. The bull case on Airbnb’s marketplace assumes that as the platform matures, fixed costs grow more slowly than revenue and operating margins expand. If that finally happens, say, operating margin expands from 21% to 25% over two years, the rising operating income masks the falling interest income. This was the pre-2024 thesis on the company and it hasn’t played out, but it isn’t dead.

What to watch in 2026 and 2027

Three indicators will tell the story over the next eighteen months.

The interest income line on the quarterly P&L. This is the single cleanest read on the rate-sensitivity dynamic. Q1 2026 results land in early May 2026. If interest income comes in below $160 million for the quarter, the trend is intact. If it rebounds to $180M+, something has changed, either Airbnb extended duration, the float grew sharply, or rate expectations shifted.

Operating income in Q2 and Q3 2026. Q3 is Airbnb’s seasonal strength quarter. If Q3 2026 operating income comes in below Q3 2025’s $1.5 billion despite revenue growth, operating leverage in the core business is genuinely deteriorating, and the rate cushion that previously masked it is gone. If Q3 operating income grows in line with revenue, the marketplace is fine and the interest income drag becomes a manageable line item.

Float duration and treasury commentary in the 10-K. Airbnb does not currently break out the duration profile of its investment portfolio in much detail, but the 10-K filed in February each year includes a section on market risk and interest rate sensitivity. Watch for any language about extending portfolio duration, increasing allocations to longer-dated Treasuries, or changes in the investment policy. A shift would signal that the CFO is actively managing the rate exposure rather than letting it ride.

The buyback pace. The 2025 program continued aggressively. If the 2026 program decelerates meaningfully, say, repurchases drop below $2.5 billion for the year, that’s the signal that interest income compression is starting to affect capital return.

Frequently asked questions

Is Airbnb actually a bank?

No, in the regulatory sense Airbnb is not a bank. It is not chartered as a depository institution. It does not have FDIC-insured deposits or central bank access. The “bank” framing is a metaphor for the underlying economics: Airbnb holds large amounts of customer cash, invests it in short-term instruments, and earns interest. That is bank-like behavior. But Airbnb is regulated as a money transmitter, not a bank, and the customer float is held in segregated accounts on behalf of customers, it is not Airbnb’s money to lend.

How much of Airbnb’s profit comes from interest income?

In 2024, interest income of $818 million was equivalent to 32% of operating income ($2,553M) and 24.6% of pre-tax income ($3,331M). In 2025, those ratios fell to 27.7% of operating income and 22.5% of pre-tax income. The exact percentage depends on which denominator you use, but in both years the interest income line was a major contributor to reported profitability.

Could Airbnb just hold the cash longer to earn more interest?

In theory, yes, Airbnb could delay host payouts further and earn more days of interest per booking. In practice, host payment timing is a competitive variable. Hosts choose platforms partly based on how quickly they get paid. Airbnb already pays slower than some smaller booking platforms, and hosts complain about this regularly. Extending the payment window would generate more interest income but at the cost of host satisfaction and potential migration to faster-paying platforms.

Why doesn’t Airbnb buy longer-dated Treasuries to lock in higher yields?

The customer float has fiduciary constraints, the cash needs to be available on short notice to pay hosts, so most of it can’t be locked into multi-year instruments. The corporate cash portion (roughly half of total interest-bearing balances) could in principle be invested longer, but doing so introduces duration risk that most public-company CFOs prefer to avoid. There is no public indication Airbnb is planning to extend duration meaningfully.

How does this compare to other tech companies with large cash balances?

Airbnb is somewhat unusual in two respects. First, the customer float is a structural feature of the business model, most tech companies don’t sit on third-party cash at all. Second, Airbnb has very little debt, so its net interest income is nearly pure interest income, whereas companies with meaningful debt balances see interest income partially offset by interest expense. The cleanest comp on net interest income from short-term holdings is probably PayPal, which similarly holds customer balances and earns interest on them.

Should I value Airbnb differently because of this?

That depends on whether you believe rate-driven interest income should be capitalized at the same multiple as operating income from the core marketplace. Most investors implicitly treat interest income as lower-quality earnings, more cyclical, less defensible, less indicative of the underlying business. Under that view, Airbnb’s “true” earning power is closer to its operating income alone, and the multiple on the stock should reflect that. The valuation implication is that Airbnb may look cheaper than it is on a P/E basis if a meaningful slice of those earnings is just monetary policy in disguise.

This analysis is based on public filings, earnings releases, and industry research from the Securities and Exchange Commission, Airbnb investor relations, Federal Reserve press releases and the FOMC dot plot, and Booking Holdings public filings.

By Hamza Benarba — Footnote Brief.