Two policy choices buried in the property and equipment notes of Microsoft, Google, Meta, and Oracle’s 10-Ks — combined with a circular capital flow between Nvidia, OpenAI, Oracle, and CoreWeave — explain a meaningful slice of what hyperscaler AI-era profits actually look like. This is what the filings show, what the math produces, and what could break.

The 60-second version

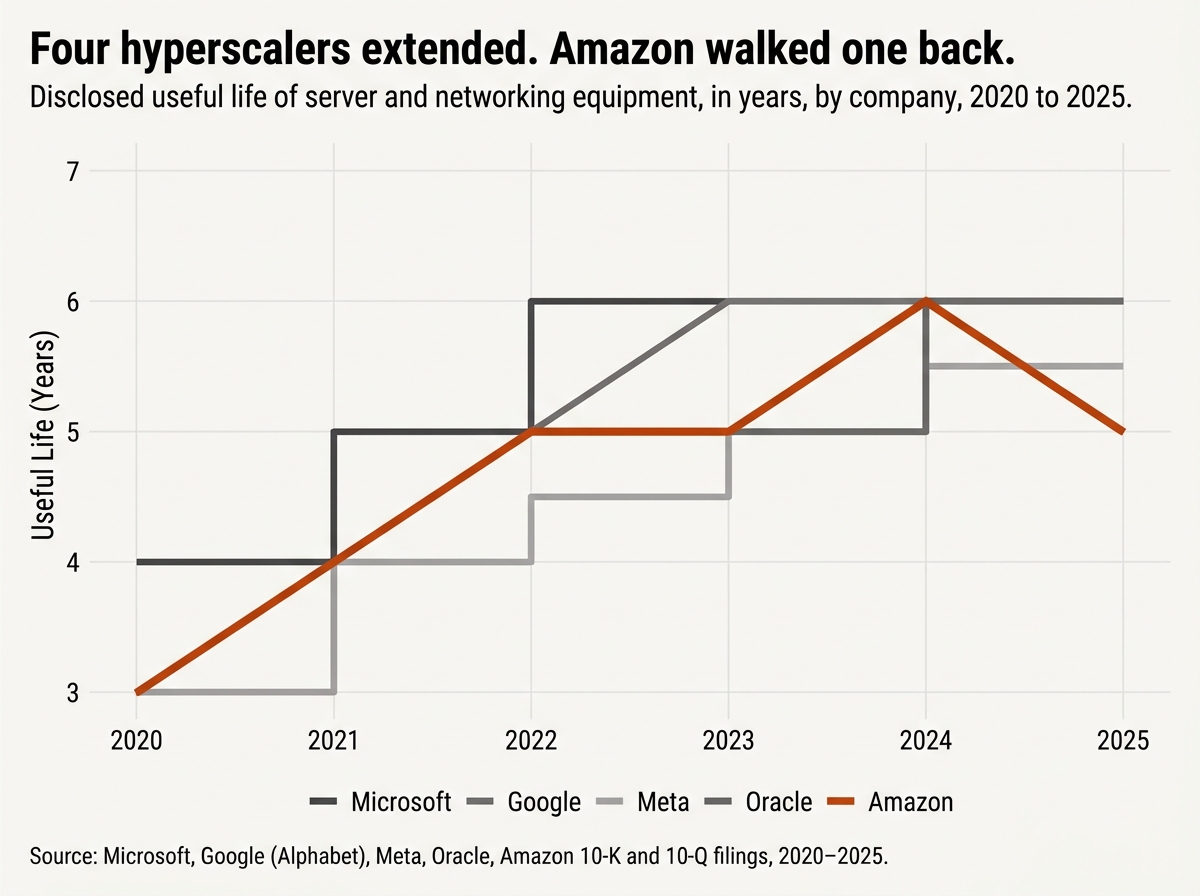

Between 2022 and 2024, Microsoft, Google, Meta, and Oracle each extended the assumed useful life of their server and networking equipment from roughly four years to five or six. The mechanical effect is lower depreciation expense and higher reported operating income — disclosed first-year benefits totaling more than $10 billion across the group, with more to come as capex compounds.

In February 2025, Amazon broke ranks. It shortened the useful life of a subset of servers and networking equipment from six years back to five, citing the “increased pace of technology development, particularly in the area of artificial intelligence and machine learning.” That divergence — under identical underlying technology — is the cleanest signal that the longer schedules at the other four are aggressive.

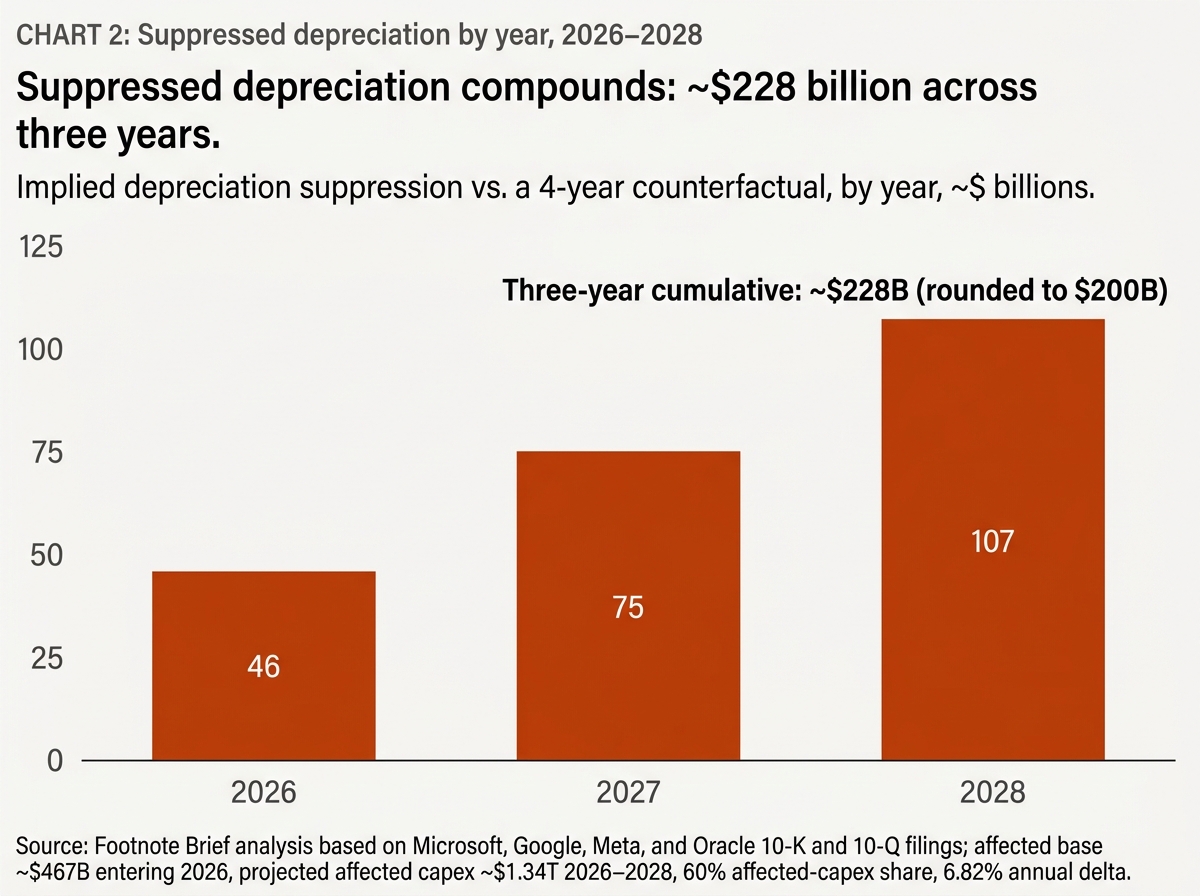

Run a four-year counterfactual against the affected base and projected 2026–2028 capex, and the suppressed depreciation comes to roughly $228 billion cumulatively, rounded conservatively to ~$200 billion. Michael Burry’s published number, $176 billion through 2028, sits in the same neighborhood with slightly more conservative assumptions.

Layered on top is a circular capital flow. Nvidia has equity stakes and capacity backstops in CoreWeave; CoreWeave’s revenue is concentrated 62–67% in Microsoft. Nvidia signed a letter of intent to invest “up to $100 billion” in OpenAI; OpenAI committed to buy $300 billion of compute from Oracle starting 2027; Oracle expects to borrow ~$100 billion to fund the build, a meaningful share of which becomes Nvidia chip revenue. The closest historical analog is Lucent and Nortel’s 1999–2001 vendor financing collapse.

Skip to the section that interests you most

The headline number: ~$200 billion through 2028

Hyperscaler AI capex is approaching half a trillion dollars annually across Microsoft, Meta, Google, Amazon, and Oracle. Most of that spending lands on the balance sheet as property, plant, and equipment, then runs through the income statement over multiple years as depreciation. The pace at which it runs through is a management estimate.

That estimate has shifted meaningfully. The cumulative effect of the shifts — through 2028, on a four-year counterfactual basis — comes to approximately $200 billion in suppressed depreciation, distributed roughly $46 billion in 2026, $75 billion in 2027, and $107 billion in 2028. Every dollar of suppressed depreciation is a dollar of additional reported operating income. None of it represents operational improvement.

The number is large but not surprising once the inputs are laid out: an existing affected asset base of roughly $467 billion entering 2026, projected affected capex over 2026–2028 of approximately $1.34 trillion, and an annual delta of about 6.82% between the disclosed schedules and a 4-year counterfactual. The methodology is detailed in the math section below.

What makes this estimate worth paying attention to is not its precision. It is the existence of a hyperscaler — Amazon — whose own 10-K filings now suggest the four-year counterfactual is closer to operational reality than the schedules its peers are using.

How four hyperscalers bought themselves billions in earnings

The depreciation schedule changes happened in a tight window between 2022 and early 2025. Each is documented in the issuer’s own SEC filings.

Microsoft. In Q4 FY2022, CFO Amy Hood told investors the company was extending the depreciable useful life for server and network equipment in cloud infrastructure from four years to six. The disclosed FY2023 benefit was approximately $3.7 billion, with $1.1 billion in Q1 FY2023 alone.

Google (Alphabet). In its January 2023 earnings release, Google announced a similar extension following a lifecycle assessment — servers and certain network equipment moved from four years to six. Disclosed full-year FY2023 depreciation reduction was approximately $3.4 billion, with the earnings impact reported around $3.0 billion.

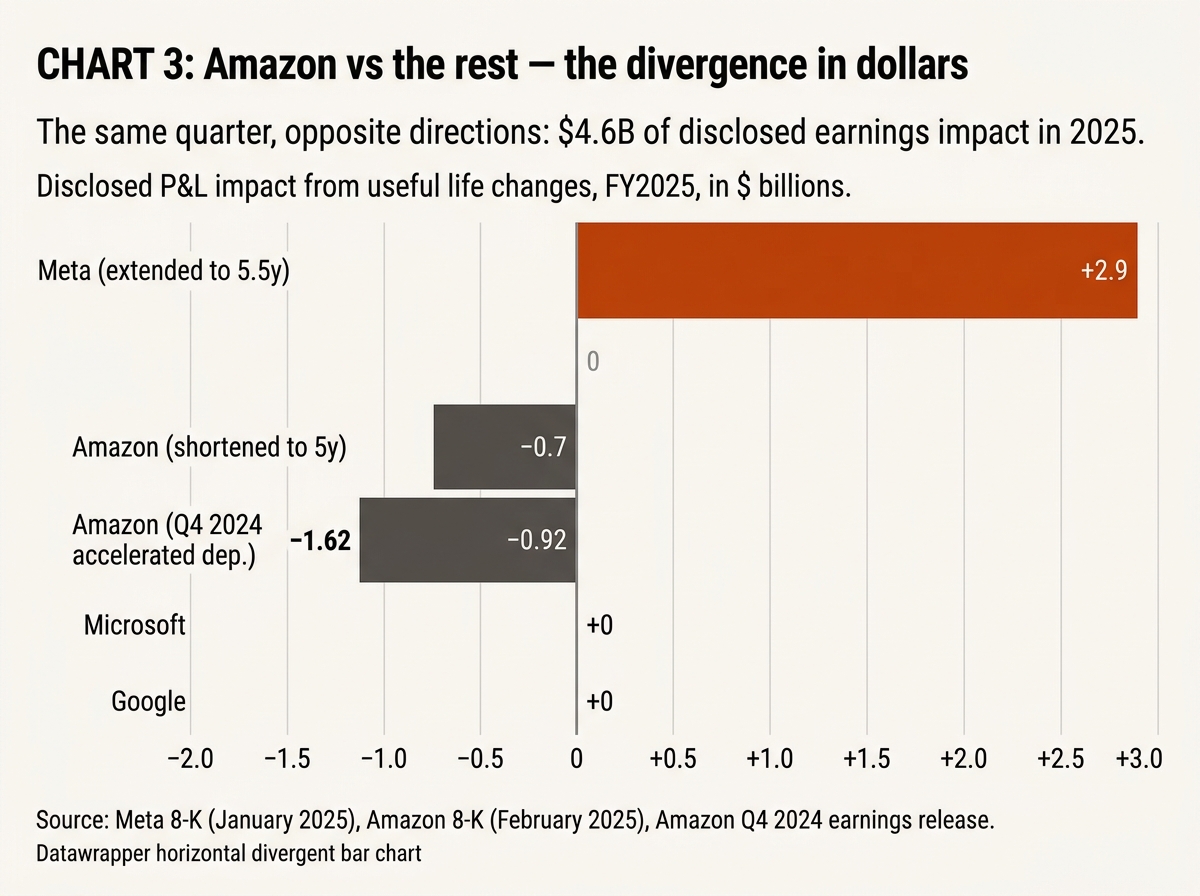

Meta. Meta’s path is the most layered. The company moved from a roughly three-year assumption in 2020 to four years, then 4.5, then five, and most recently — effective January 29, 2025 — to five and a half years. The 2025 disclosed reduction in depreciation expense is $2.9 billion, equivalent to nearly 4% of estimated pre-tax profit for the year.

Oracle. Oracle moved its server and networking useful life from four to five years in 2023 per filings, and is now operating on a six-year schedule for both servers and networking, per the most recent disclosures.

Across the four, the disclosed first-year benefits are well over $10 billion. The compounding effect across the affected fleet, as new capex layers in at the longer schedule, scales the impact considerably from there. The justifications across filings are consistent: software efficiency, advances in technology, planned utilization, fleet rearchitecture. The disclosures meet GAAP. The auditors signed off.

The justifications are also identical to what makes the policy aggressive. AI infrastructure is the part of the fleet experiencing the most rapid technological turnover in the industry’s history — Hopper to Blackwell to Vera Rubin generational jumps in 18 to 24 months. The argument that software efficiency is extending economic life applies more easily to general-purpose servers than to frontier-AI training systems whose marginal economic value collapses the moment the next generation ships.

Amazon broke ranks — and the divergence is the hook

On February 7, 2025, Amazon disclosed that following its Q4 2024 useful life study, it would change the assumed useful life of a subset of its servers and networking equipment from six years back to five, effective January 1, 2025. The expected reduction in 2025 operating income was approximately $0.7 billion. Separately, Amazon took a $920 million accelerated depreciation charge in Q4 2024 for early-retired equipment.

The disclosed reason — pulled directly from the filing — cites the “increased pace of technology development, particularly in the area of artificial intelligence and machine learning.”

Amazon was the third hyperscaler to extend useful life (3→4 in 2020, 4→5 in 2022, 5→6 in 2024). It is the first hyperscaler to walk one back. It did so in the same quarter Meta extended in the opposite direction.

The divergence matters because it cannot be reconciled by underlying technology. Microsoft, Google, Meta, Oracle, and Amazon are all operating broadly the same chips in broadly the same data centers serving broadly the same workload mix. If the technology supports a 5.5-year life, Amazon does not need to retire $920 million worth of equipment early. If it doesn’t, the others’ schedules are wrong.

The asymmetry is significant: Amazon’s reversal cost the company $700 million of reported 2025 operating income. There is no tax benefit to over-depreciating, no rating agency reward, no narrative gain. Companies do not voluntarily eat that hit unless the operational data leaves them no choice.

Reconstructing the math: a 4-year counterfactual

The methodology behind the ~$200 billion figure is straightforward and replicable from the filings. The structure:

- Affected base entering 2026: approximately $467 billion in net property, plant, and equipment across the four extending hyperscalers (Microsoft, Google, Meta, Oracle), in the categories where useful life was extended — primarily servers, networking, and some structured cabling.

- Projected 2026–2028 capex: approximately $1.34 trillion in additional spending across the same categories, based on each company’s most recent guidance and analyst consensus.

- Affected capex share: roughly 60%. This excludes buildings, land, leasehold improvements, and general data center fitouts (which retain their original lives, typically 15–40 years), and includes server hardware, networking equipment, and the GPU and CPU components subject to the extension.

- Annual delta: approximately 6.82% of the affected base. This is the difference between the disclosed schedules (5–6 years) and the 4-year counterfactual matching pre-2022 policy.

- Three-year cumulative: roughly $228 billion. Rounded conservatively to ~$200 billion to absorb estimation error.

The annual progression is what tells the story:

| Year | Suppressed depreciation (≈) |

|---|---|

| 2026 | $46 billion |

| 2027 | $75 billion |

| 2028 | $107 billion |

| Cumulative | ~$228 billion |

The reason 2028 is so much larger than 2026 is mechanical: capex booked at the longer life is still ramping. The full effect compounds as the fleet turns over.

A note on precision. The 6.82% delta is not a round number, and that is on purpose — it is the calculated weighted-average difference across the four issuers’ specific old-vs-new schedules. The 60% affected-capex share is the most defensible single number for cross-company aggregate work, but the actual figure differs by company (Oracle’s mix is more server-heavy than Microsoft’s; Meta’s data center buildouts include more shell construction than Google’s). Anyone running the numbers at a single-issuer level should adjust.

The Burry version, and where my number sits

On November 11, 2025, Michael Burry — manager of Scion Capital, known for predicting the 2008 housing collapse — posted on X that hyperscalers were artificially boosting earnings by extending useful life assumptions beyond what 2-3 year product cycles justify. His estimate of the total understatement of depreciation across 2026–2028 was $176 billion. He singled out Oracle and Meta, projecting their earnings could be overstated by roughly 27% and 21% respectively by 2028. He simultaneously disclosed short positions on Nvidia and Palantir.

Burry’s $176 billion uses a slightly more conservative counterfactual than mine — he benchmarks closer to a 3-year life for AI-specific hardware in some scenarios, but applies it across a narrower asset base. My ~$228 billion (rounded to ~$200 billion) uses a 4-year counterfactual matching pre-extension policy across a broader base, including non-frontier servers and networking. Different inputs, similar conclusion.

Importantly, both numbers are calibrated to a counterfactual Amazon’s own filings now suggest is roughly correct. The “5-year for AI servers” position Amazon took in February 2025 sits between the 4-year pre-extension policy (more aggressive write-down) and the 6-year current schedule at the others (less). A 4-year counterfactual is, if anything, the more defensible reference once Amazon’s data is in.

The small loop: Microsoft → CoreWeave → Nvidia

The depreciation question is the accounting half of the picture. The other half is how the demand that justifies the spending in the first place is being financed. The cleanest illustration is the smaller of two circuits running through the AI infrastructure stack.

Microsoft is CoreWeave’s anchor customer — 62% of CoreWeave’s $1.92 billion 2024 revenue, 67% of its 2025 revenue. CoreWeave does not own that infrastructure outright. It finances its GPU buildout through GPU-collateralized debt — analysts estimate roughly $10.45 billion outstanding, layered across at least five delayed-draw term loan facilities, including an $8.5 billion investment-grade-rated facility closed in March 2026 secured by $19.2 billion of Meta contract backlog.

Nvidia, the supplier of the GPUs that collateralize this debt, holds approximately a 13% equity stake in CoreWeave — up from 1.21% three years ago and 7% at the IPO. The most recent investment was a $2 billion private placement at $87.20 per share in January 2026. The total stake value, depending on the day’s share price, sits in the $4–5 billion range. Nvidia separately wrote CoreWeave a $6.3 billion take-or-pay capacity backstop in September 2025, effectively committing to lease unsold compute as a safety valve.

Trace the dollars: Microsoft pays CoreWeave for compute. CoreWeave borrows against the multi-year Microsoft contract. The borrowed money flows to Nvidia in exchange for GPUs. Nvidia owns a slice of CoreWeave’s equity and contractually guarantees a chunk of its capacity. The dollars are real. The path is a closed circle.

This is not, by itself, fraudulent or even unusual — vendor financing structures exist in many capex-heavy industries. The signal is in the concentration. CoreWeave’s primary hardware supplier and primary strategic backer are the same company. Its primary revenue source is one customer. Its primary collateral is hardware whose secondary market values are already declining (H100 hourly rental rates have fallen roughly 70% from peak).

The big loop: Nvidia → OpenAI → Oracle → Nvidia

The larger circuit operates at roughly 30x the dollar scale and involves three of the most-watched companies in the AI infrastructure stack.

The September 22, 2025 announcement was striking. Nvidia and OpenAI signed a letter of intent for Nvidia to “invest up to $100 billion in OpenAI as the new NVIDIA systems are deployed,” targeting at least 10 gigawatts of Nvidia systems. CEO Jensen Huang at the time called it “the biggest AI infrastructure project in history.”

Two important caveats followed.

In December 2025, at the UBS Global Technology and AI Conference, Nvidia CFO Colette Kress told investors: “We still haven’t completed a definitive agreement.” The company’s then-current sales outlook of approximately $500 billion in Blackwell and Vera Rubin demand explicitly excluded any work tied to the new OpenAI agreement.

In February 2026, in Taipei, Huang told reporters: “It was never a commitment. They invited us to invest up to $100 billion and of course, we were, we were very happy and honored that they invited us, but we will invest one step at a time.”

Whatever the eventual size, OpenAI’s compute commitments are being made today. The company has signed a $300 billion deal with Oracle for compute over five years starting in 2027 — $60 billion a year, delivering 4.5 gigawatts of capacity, part of the Stargate program. By Q3 FY2026, Oracle’s remaining performance obligations had grown to $523 billion, up 438% year-over-year, reflecting the scale of these commitments.

Delivering $300 billion of compute requires building data centers and filling them with chips. KeyBanc analysts estimate Oracle will need to borrow approximately $100 billion over four years — about $25 billion annually — on top of $82 billion in existing long-term debt. Oracle’s announced 2026 plan: $45–50 billion in funding, half debt and half equity. By March 2026, Oracle’s non-current debt sits at $124.7 billion and trailing free cash flow is approximately negative $24.7 billion. Moody’s has flagged that Oracle’s debt is growing faster than its earnings; the company’s bonds, despite an investment-grade rating, have at points traded at credit default swap spreads above 125 basis points — the kind of level last seen during the 2009 financial crisis.

Of the ~$100 billion Oracle is raising over four years, a meaningful share — call it $40 billion at sticker prices and reasonable utilization assumptions — flows back to Nvidia in the form of GPU purchases.

The compressed circuit: Nvidia commits to invest in OpenAI. OpenAI commits to buy from Oracle. Oracle borrows to buy from Nvidia. Nvidia books the revenue. Nvidia’s market cap rises. The market cap underwrites the next leg.

OpenAI’s CFO Sarah Friar told Tomasz Tunguz at Theory Ventures that “we’re making some very tough trades at the moment on things we’re not pursuing because we don’t have enough compute.” The compute scarcity is real. The harder question is what fraction of the demand is end-customer pull-through, and what fraction is the upstream chipmaker financing its own buyers.

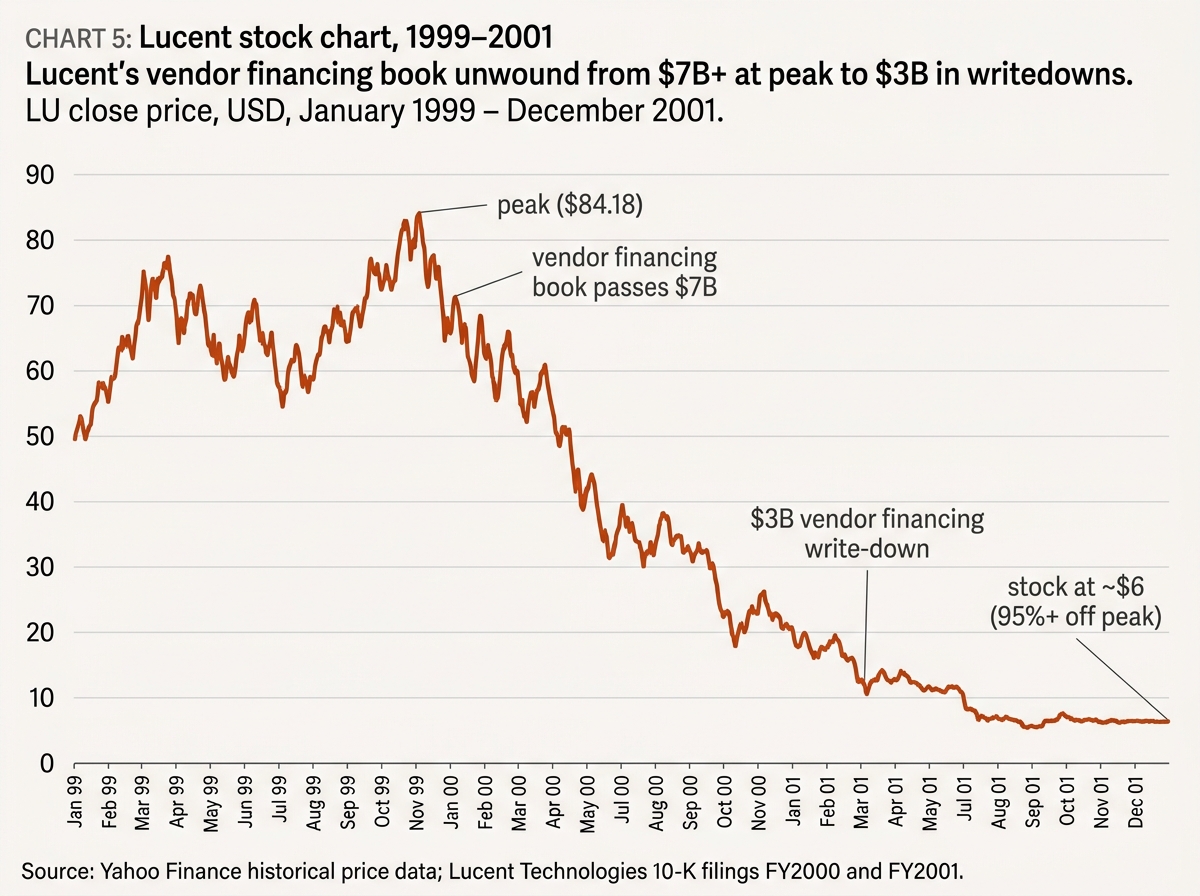

Lucent and Nortel: the 1999 analog

Vendor financing arrangements where the seller funds the buyer have a history. The most relevant one in dollar scale and structural similarity is the telecom buildout of 1998–2001.

Lucent Technologies, spun out of AT&T in 1996, was the dominant U.S. supplier of telecom equipment. In the late 1990s, a wave of newly formed competitive local exchange carriers (CLECs), internet service providers, and emerging mobile operators became Lucent’s most important growth customer base. These companies were, with few exceptions, unprofitable. They were also signing equipment commitments multiples larger than their then-current revenue.

Lucent’s response was vendor financing. The company extended credit to its customers — sometimes structured as receivables, sometimes as direct loans — to fund the equipment purchases. By 2000, Lucent’s vendor financing book had grown past $7 billion. Nortel Networks, Lucent’s Canadian counterpart, ran a similar book. Both companies booked the equipment sales as revenue in real time. Both companies’ market caps exploded. Lucent peaked at $84 per share in late 1999, with a market cap above $250 billion.

The unwind started in 2001. The CLECs and ISPs ran out of equity capital. They couldn’t service the financing. Lucent and Nortel had to take large write-downs against their financing books — Lucent took a $3 billion provision in March 2001 — and at the same time the equipment those customers had bought went into the secondary market at deep discounts, dropping the value of similar equipment on Lucent’s own balance sheet. Lucent’s stock fell more than 95% from peak. Nortel went bankrupt in 2009.

The 2026 AI version is differently structured but rhymes:

- The buyer (OpenAI) is unprofitable and signing commitments multiples larger than its current revenue.

- The capacity layer (Oracle, CoreWeave) is funding the buildout with debt collateralized by hardware whose useful life — by Amazon’s own filings — is shorter than the seller is willing to admit on its own books.

- The chipmaker (Nvidia) sits on both sides: selling the hardware and equity-financing the customer who buys it.

The break point in 1999–2001 was when the equity backing the buyers ran out. The buyers couldn’t pay. The receivables wrote down. The collateral wrote down. Both happened in the same window.

The 2026 break-point candidates: an OpenAI funding round that prices materially below the most recent $852 billion valuation; any hyperscaler matching Amazon and shortening its useful life; Oracle’s inability to refinance 2027 maturities at investment-grade pricing; Nvidia’s $500 billion Blackwell-Vera Rubin pipeline failing to convert without OpenAI legs being formalized.

Sensitivity: stress-testing the $200B

The headline number assumes a 4-year counterfactual against the affected base. Different assumptions produce different outcomes.

| Scenario | Useful life assumption | 2026–2028 cumulative impact (≈) |

|---|---|---|

| Bear (Burry’s harsher version) | 3 years for AI hardware | $280–320 billion |

| Base case (this analysis) | 4 years matching pre-extension policy | ~$200 billion |

| Burry published number | Mixed 3–4 years | $176 billion |

| Amazon-aligned | 5 years across the board | $80–100 billion |

| Status quo | 5–6 years (current disclosed) | $0 — already in earnings |

The point of the sensitivity table is not to produce a single right number. It is to show that under any assumption other than the current disclosed schedule, reported AI-era earnings are systematically overstated. The conservative version of the bear case — Amazon’s own 5-year position — still implies $80–100 billion of suppressed depreciation across the three years.

For single-issuer analysis, the most exposed names by suppressed-depreciation-as-percent-of-pre-tax-profit are Oracle and Meta (per Burry’s 27% and 21% estimates), with Microsoft and Google materially less exposed because their absolute pre-tax profits are larger.

Why the auditors haven’t pushed back

The natural question: if four hyperscalers are running aggressive useful life assumptions, why aren’t their auditors objecting?

The answer is that GAAP gives substantial flexibility. ASC 360 (Property, Plant, and Equipment) requires companies to depreciate assets over their “expected useful life,” which is the company’s own determination based on planned utilization, technological factors, and operational data. There is no fixed schedule. Auditors test whether management’s estimate is supported by internal documentation and whether disclosures are consistent with that documentation.

The hyperscalers have submitted documentation. Microsoft cited “investments in our software that increased efficiencies in how we operate our server and network equipment.” Google cited a January 2023 lifecycle assessment. Meta’s filings reference “regularly evaluat[ing] for factors such as technological obsolescence and our planned use and utilization.” Oracle’s disclosures reference similar studies.

The auditors’ job is not to second-guess the documentation but to test whether it is internally consistent and whether the resulting estimate falls within a defensible range. Six years for general-purpose enterprise servers running mixed workloads is defensible. Six years for frontier-AI training hardware that will be displaced by the next Nvidia generation in 18–24 months is less defensible — but the cascading-use argument (frontier training → inference → cloud rendering → archival) has been used to bridge the gap.

The argument is also, partly, self-fulfilling. As long as Microsoft, Google, Meta, and Oracle all use 5-6 year assumptions, the auditors can point to industry practice as a benchmark. Amazon’s reversal complicates that defense — but doesn’t yet break it, because the others can argue Amazon’s mix is different.

A meaningful inflection would be the SEC commenting on the policy directly, or a second hyperscaler matching Amazon’s reversal. Neither has happened as of the most recent filings.

The risks to the $200B thesis

A thesis worth holding has to survive its honest counterarguments. Three are particularly worth taking seriously.

The cascading-use argument has empirical support. Hyperscalers run a multi-tier infrastructure — top-tier GPUs serve frontier training for 12–18 months, then cascade to fine-tuning, then to inference, then to non-AI compute or as backup capacity. If the cascade actually extends total economic life to 5–6 years, the longer schedules are correct. The bull side cites internal utilization data showing meaningful inference workloads still running on Volta-generation hardware deployed in 2017.

The counter to the counter: the cascade was true for the pre-AI fleet. It is not yet proven for the AI fleet, where each new generation is materially more capable per dollar than the prior, and where customers are willing to pay materially more for the new generation. The economics may not support the cascade in the same way.

Burry has been early before, and wrong before. The “Big Short” track record is one famously correct call. Burry has subsequently been bearish on Tesla, the broader market, China, and several other positions where he was either wrong or early. Pattern-matching to Burry’s calls is not a substitute for the underlying analysis.

The counter: the depreciation argument is replicable from publicly available filings. It does not require trusting Burry’s judgment. The math is the math.

Amazon’s reversal may not be the signal it appears to be. Amazon’s 5-year position applies to “a subset” of servers and networking equipment, not the entire fleet. The company has not extended the reversal to all assets. It is possible Amazon is simply being conservative on a specific cohort — perhaps Trainium-related hardware — and the broader 6-year assumption holds for the rest of the fleet.

The counter: the reversal still happened. The disclosed reason still cites AI-driven technology pace. A subset reversal still implies the 6-year schedule was wrong for that cohort. The question is how big the cohort is, and whether other hyperscalers will need to do similar subset reversals as their fleets age.

What to watch in the next 12-18 months

Four signals would meaningfully strengthen or weaken the thesis.

A second hyperscaler matching Amazon’s reversal. Microsoft’s, Google’s, Meta’s, or Oracle’s next 10-K will disclose any change in useful life assumptions. A second hyperscaler shortening would effectively confirm the policy is moving back toward 4–5 years across the industry. Watch for the FY2026 filings landing March–April 2026.

H100 and Blackwell secondary market pricing. GPU rental rates are a real-time signal of effective useful life. H100 hourly rentals have fallen from a peak of roughly $8–10 per hour to $2.85–3.50 today. A drop below $2.00 would suggest cascade saturation and would put real pressure on the longer depreciation schedules.

Oracle’s refinancing capacity. Oracle’s existing $82 billion long-term debt has scheduled maturities throughout 2027–2030. If the company can refinance at investment-grade pricing, the circular financing model has room to run. If credit markets reprice Oracle as a high-yield credit, the OpenAI buildout becomes structurally more expensive and may need to be slowed or restructured.

Definitive Nvidia–OpenAI agreement. As of February 2026, Huang has explicitly described the $100 billion as “never a commitment.” A definitive agreement at materially smaller scale — $25 billion, say — would be informative. A definitive agreement at $100 billion would be the bull case crystallized. The stretch and ambiguity in between is the relevant signal.

The same Nvidia chip is generating two reported profits today — once when Nvidia sells it, and again when the hyperscaler buyer refuses to admit how fast it’s aging. Only one of those profits will turn out to be real. The size of the gap, by 2028, is somewhere between $176 billion and $230 billion — and the chip you’re depreciating over six years is the same chip Amazon is now depreciating over five.

This analysis is based on Microsoft, Google (Alphabet), Meta, Oracle, Amazon, Nvidia, OpenAI, and CoreWeave SEC filings (10-K, 10-Q, 8-K, S-1, FWP), Q4 2024 and Q1–Q3 2025 earnings releases, KeyBanc Capital Markets analyst notes, and reporting from CNBC, Reuters, Bloomberg, the Wall Street Journal, The Register, Data Center Dynamics, and Tomasz Tunguz at Theory Ventures.

— Hamza, Footnote Brief

Frequently asked questions

Is hyperscaler depreciation policy fraud?

No. Useful life is a management estimate that GAAP explicitly leaves to the company, subject to auditor review and disclosure consistency. The hyperscalers’ disclosed schedules are within a defensible range and are documented in the filings. The argument here is that the policy is aggressive given the technology cycle, not that it is fraudulent.

How much would Microsoft, Google, Meta, and Oracle’s earnings fall if they all matched Amazon?

A back-of-envelope estimate, using the 5-year reference, would put the cumulative 2026–2028 impact at roughly $80–100 billion across the four — versus ~$200 billion under a 4-year counterfactual. Per-company impact varies meaningfully with the AI-share of the fleet; Oracle and Meta are the most exposed.

Why is Nvidia investing in its own customers?

Two reasons. First, capacity. AI infrastructure is supply-constrained, and equity stakes in operators like CoreWeave, Nebius, and Lambda give Nvidia priority allocation and operational visibility. Second, demand support. Equity financing the buyers helps clear Nvidia’s inventory at posted prices in periods when those buyers couldn’t otherwise close their funding gaps.

The 1999 telecom analog is the cautionary version: vendor financing works until the buyers run out of equity. Nvidia’s stakes are smaller as a percentage of revenue than Lucent’s were at peak, but the structural pattern is similar.

Is Oracle going to default?

Probably not in the near term. Oracle’s investment-grade rating is intact, the OpenAI revenue is contracted, and the company has demonstrated access to both debt and equity markets. The risk is reputational and strategic — credit spreads widening, equity multiple compressing — rather than acute default. Barclays has flagged a cash runway concern by November 2026 if current trajectory continues, which gives a marker.

What’s the bull case for the longer schedules?

The cascade. Frontier training hardware moves to inference, then to lower-tier inference, then to non-AI compute. If the cascade is real and the total economic life is 6+ years, the schedules are correct. The empirical question is whether the cascade economics will actually hold in the AI generation. The next 4–6 quarters of utilization disclosures should clarify this.

How does this affect Nvidia’s stock?

Indirectly. If hyperscalers are forced to shorten their schedules, reported AI-era earnings fall, multiples compress, and capex enthusiasm cools. Cooler capex enthusiasm flows back to Nvidia as smaller orders, particularly in the customer cohorts financed through circular structures. The chain runs from hyperscaler depreciation policy → reported earnings → equity multiple → capex commitment → Nvidia revenue. None of these links are mechanical, but the directional pressure is there.